Darren415

| Here’s one I first wrote about in 2015 with updated numbers and regulatory developments. |

S&P 500 (SPY)

I want exposure that 1) correlates closely with the S&P 500 (NYSEARCA:SPY) and 2) compounds generationally, with as little tax leakage as possible. Here’s something you can do this week that could combine those virtues.

#1 Passive Fund in the World

Vanguard

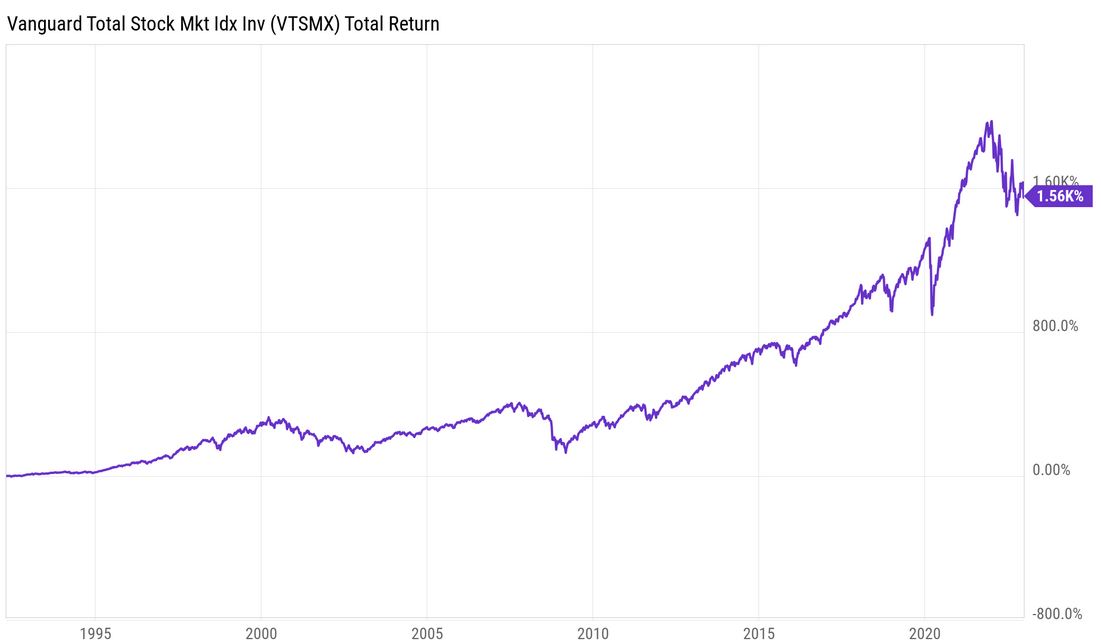

I have always mixed active investing ideas with some amount of passive market exposure. Passive exposure is cheap, simple, and tax efficient. It also provides me with a little insurance against the results of my active ideas. My No. 1 favorite place to get market exposure with these benefits is Vanguard’s Total Stock Market Portfolio (VTSMX) within Vanguard’s 529. It has done well since inception:

YCharts

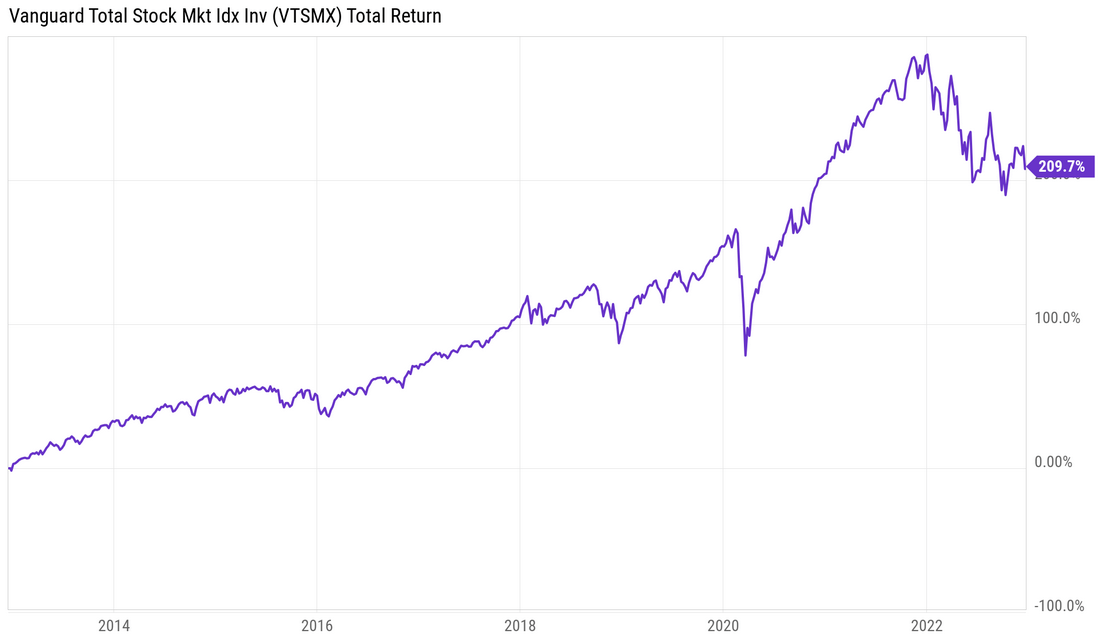

It’s up over 200% since I discussed it as a long idea:

YCharts

Management

Vanguard claims that:

We hire top investment professionals with the experience and expertise you’d expect from Vanguard.

But this is an unmanaged fund, so as long as they can keep the books straight, they could also:

hire psychotic crack fiends with the experience and expertise I’d expect from San Quentin.

…for all that I would care.

Service

Their service is fine. It improves on the margin if you put in over $1 million and improves again over $10 million. They give you the name and phone number of a competent representative who typically can solve problems associated with such accounts, so I’ve never been put on hold or gotten an automated answer.

529s

A 529 savings plan is an investment account intended for college and other higher-education costs. They are sponsored by individual states and offer various tax benefits. Earnings are deferred from federal taxes. Withdrawals for qualified higher-education expenses are also tax-free. You can make up to five years’ worth of contributions at one time without triggering gift tax. The uses are pretty generous – you can use the money for tuition, room and board, books, and other expenses.

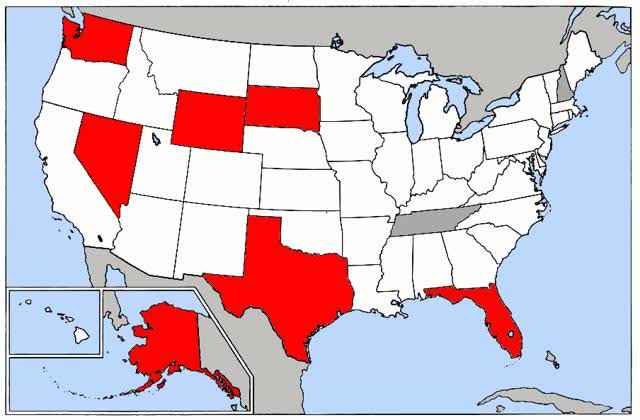

Why Nevada?

Nevada is one of the few remaining states without any income tax.

NV

If you have flexibility as to where you live, these are probably states worth considering. Of the bunch, Wyoming is my favorite. If one lives in Wyoming close enough to Montana to shop there, you can pay Wyoming’s zero percent income tax and Montana’s zero percent sales tax.

As for Nevada, since they lack a state income tax, they cannot lure Nevadans to their 529 with promises of avoiding state income tax. Instead, they have offered every other type of inducement. Their $500,000 limit for beneficiary account balances that can get additional contributions is high. Funds are removed from your estate and are exempt from creditors’ claims. They are lenient about any requirement to withdraw funds.

Why Vanguard?

Compared to the alternative in Nevada, Vanguard’s 529 allows you to invest in Vanguard funds. Alternative funds cost more while the expense ratio on my favorite Vanguard fund is 0.12%. Vanguard’s minimum initial contribution is $3,000 (or $1,000 for Nevada residents) instead of $250, but the whole idea with this investment is to make a large investment and to hold it for a very long time. There are no enrollment fees for Nevada 529s.

Why the Total Stock Market Portfolio?

While this fund is highly correlated with the S&P 500, it’s somewhat more diversified. It includes smaller capitalization companies. In doing so, it avoids some of the turnover associated with companies entering and exiting the S&P 500. That reconstitution generates trading fees and taxes. Companies included in the S&P 500 trade at a premium, which one has to pay every time one buys an S&P 500 index fund or ETF. Owning a broader-based fund avoids such expenses. But whether or not you agree with my rationale, the difference is trivial.

Scale

This is a tax-advantaged fund with a much bigger scale than your IRA contribution limit. For 2022, the IRA contribution limit is $6,000 ($7,000 for people 50 or older). One might as well fund it, but the scale is small. The 529 limit is $500,000 per beneficiary. If you are married, you can each invest $500,000 with oneself as the owner and beneficiary. This is an ideal vehicle for long-term tax-free compounding.

Withdrawals

This investment idea works well regardless of your intention for the proceeds. It works best when invested for at least a generation or longer. However, regardless of your time horizon, it’s more flexible than it first appears. There are at least five great ways to use the proceeds.

1) College for your kids and grandkids

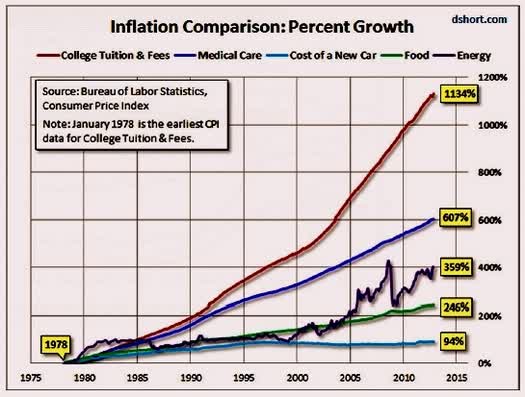

First, one can use it for its intended purpose: College, presumably for your kids or grandkids. It’s easy to transfer money from one beneficiary to another. This year, you can transfer assets in increments of $80,000 once every five years without any gift tax (bumped to $85k in 2023). Higher education is expensive and getting more expensive. It should be no surprise that we suffer under the highest inflation where there are the most third-party payers. The government enters the bid side of a market with no price-sensitivity, and it… increases prices:

dshort.com

Is the expense more worrisome or is the fact that politicians fail to see the connection between their behavior and prices? In any event, it’s likely that you will have higher education bills in your future.

2) College for yourself

Secondly, you can spend the money on yourself. Whether or not you have kids or grandkids (or have any inclination to subsidize said kids/grandkids), you can still save the money in a 529 and spend it on… your own bad self. Courses in wine tasting and golf in an idyllic college town would not be terrible.

3) College as philanthropy

Thirdly, you can give the money away. Even if you do not want to spend it on either your progeny or yourself, this would make a perfect foundation for your philanthropic educational efforts. Whether or not you will have college bills to pay, someone certainly will. You will be able to help them.

4) Future expanded usage

Fourth, it’s reasonably likely that the hodgepodge of tax-advantaged accounts will be simplified and consolidated in the future. If this one is consolidated with others intended for retirement or healthcare, then the limitations on usage will have effectively disappeared. Over the next 50 years, this is highly likely.

5) Just pay the penalty… you will still come out ahead

Fifth and finally, you can simply pay the penalty. But here’s where this idea gets really interesting, in fact, dominant as a strategy: The penalty is too small. Federal law imposes a 10% penalty on earnings for non-qualified distributions. While I never plan to pay this penalty, the cost of 10% of the earnings on the back end will probably be far less than the benefit of compounding tax-free in the interim decades. Even if you intend to spend the money on wine, women, and song (and fail to find an anthropology course “Wine, Women & Song 101”), then you can compound tax-free, pay the penalty, and still end up ahead.

Scholarship Encouragement

If your kids fully expect that you will pay for college, it can be harder to encourage them to find scholarships. There are piles of scholarship dollars everywhere for almost every type of kid. The key is for them to be motivated to find it and get it. If they receive a scholarship, then the penalty for withdrawing money from a 529 is waived. My hope is that my kids attend military academies (also that my daughter elopes). If the plan succeeds, then there are decades ahead of tax-free compounding without any restriction on some withdrawals. In order to interest them, I’m offering each kid half of whatever they earn in scholarship money.

Conclusion

If you max out your 529 contribution and then wait for a long time, you will benefit from tax-free compounding at a significant scale. At the same time, the cost of the limitations on withdrawals is manageable. With that base of passive market exposure, one can turn to active ideas. My best ones are here.

TL; DR

Max out all of the tax-advantaged account types, including 529s.

Be the first to comment