photographer3431

I just finished reading a book titled “Unconventional Success” by David Swensen that I would highly recommend to anyone. The author makes a solid case for owning REITs in what he refers to as a “core asset class” as he explains,

“Sustained levels of high cash flow lead to stability in valuation, as a substantial portion of asset value stems from relatively predictable cash flows.”

He added,

“In contrast, as leases approach expiration, owners face releasing risk, causing investors to face near-term variability in residual value.”

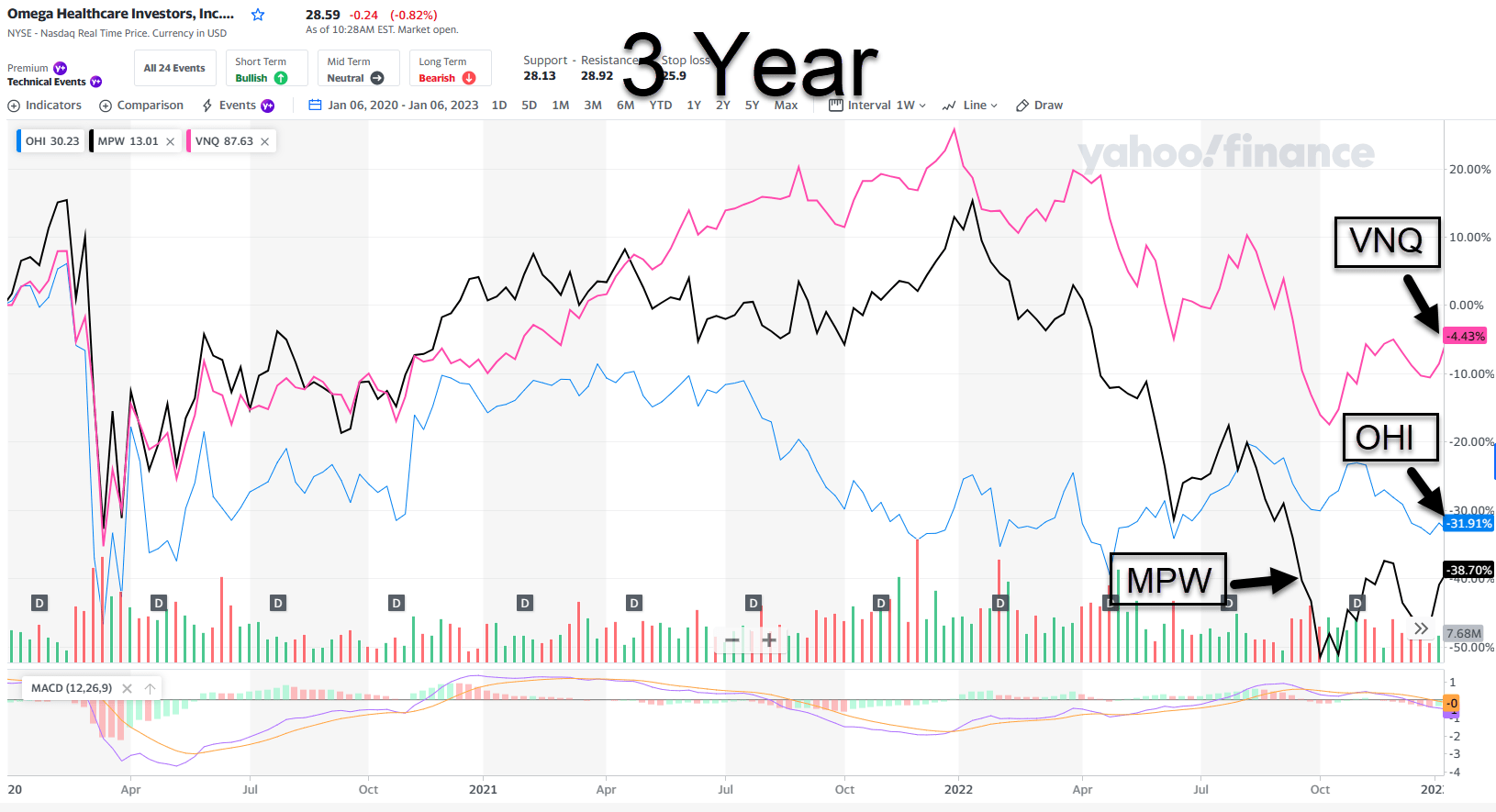

This seems logical – that real estate should be valued based on its underlying cash flows – yet two healthcare REITs are being valued by Mr. Market based on high lease-up risk.

Yahoo Finance

There’s no argument from me that these two REITs are riskier than many of the blue chips that we recommend; however, there’s a compelling argument that the business models will continue to generate predictable income that could result in very attractive total returns.

iREIT on Alpha

Medical Properties Trust (NYSE:MPW)

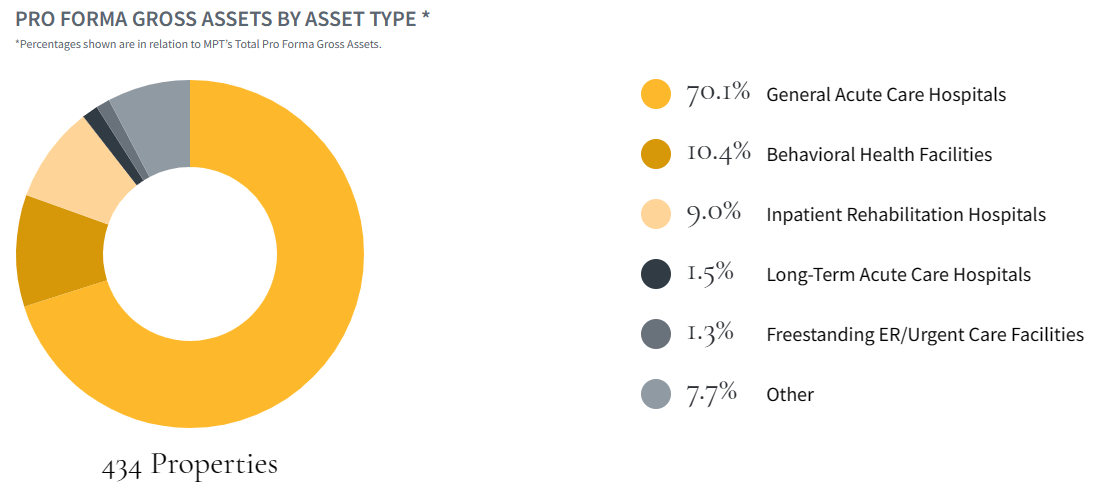

Medical Properties is an internally managed real estate investment trust (REIT) founded in 2003 that primarily invests in hospital properties and is the only pure play hospital REIT.

They own 434 properties in 10 countries that contain approximately 44,000 licensed beds and their leases are typically structured on a net-lease basis. MPW’s asset mix contains 80.6% hospitals (general acute care, inpatient rehabilitation, long-term acute care hospitals), 10.4% behavioral health facilities, 1.3% urgent care facilities, and 7.7% described as other.

MPW Portfolio

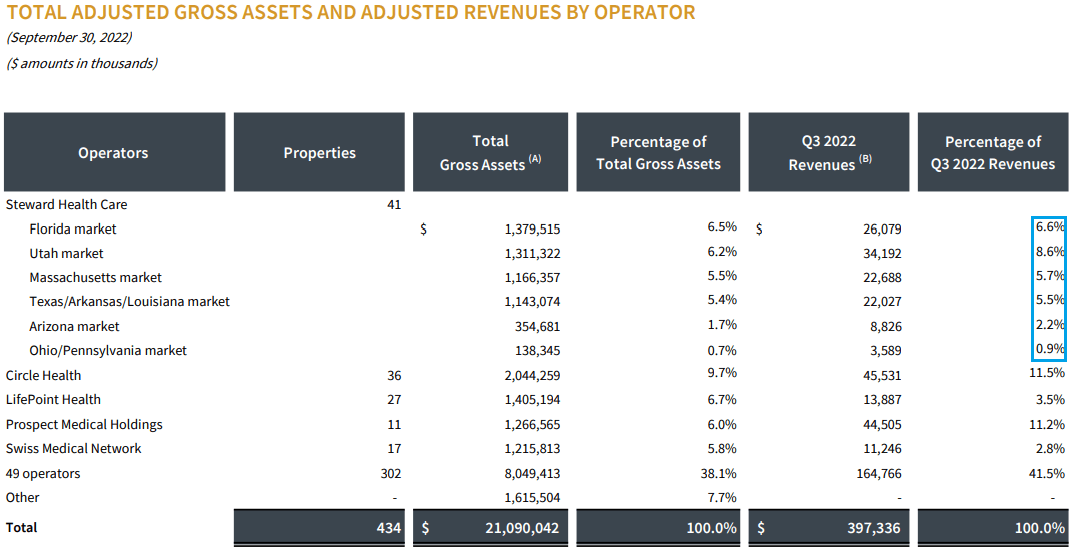

As a percentage of revenue, Steward Health is MPW’s largest tenant making up 29.5% of MPW’s revenue as of the 3rd quarter in 2022.

After Steward, Circle Health and Prospect Medical Holdings are MPW’s 2nd and 3rd largest tenants with 11.5% and 11.2% of total revenue respectively.

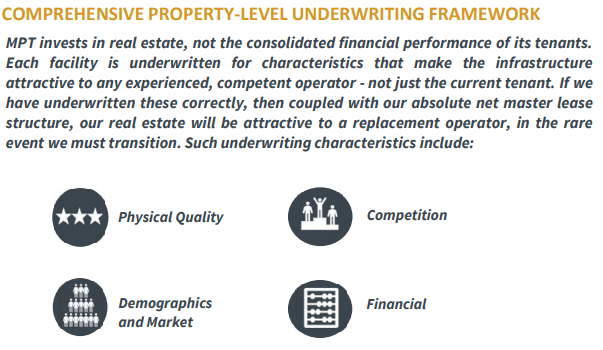

There is no argument that MPW has a high tenant concentration, but they stress the fact that they underwrite the real estate, not the operator’s financial performance.

MPW Investor Presentation

Hospitals are critical infrastructure and MPW underwrites properties that have attractive characteristics (population density, proximity to major highways, proximity to competing hospitals, etc.) that would attract any operator, not just the current tenant. If the real estate is valuable, then they should be able to replace any tenant in the event of a default.

MPW Q3 Supplemental

Omega Healthcare Investors (NYSE:OHI)

Omega Healthcare Investors is a triple-net REIT that specializes in Skilled Nursing and Assisted Living Facilities with properties in the US and UK.

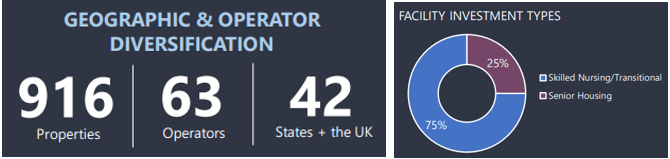

They have a portfolio of investments that includes 916 properties managed by 63 different operators. 75% of their investments are in Skilled Nursing while 25% are in Senior Housing and in all they have a total of 91,643 certified beds.

OHI Investor Presentation

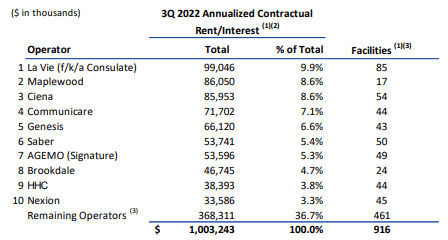

Although not as high as MPW, Omega also has a high tenant concentration. Omega’s top 3 tenants make up 27.1% of their annual rent, while their top 10 tenants make up 63.3% of their annual rent.

OHI Investor Presentation

Skilled Nursing and Assisted Living Facilities have both headwinds and tailwinds that they are facing. As most of us know, the pandemic put a real strain on the healthcare system as a whole.

Nursing and Assisted Living Facilities were hit particularly hard with the spread of covid and the impact it had on the elderly residents. The tough working conditions resulted in staffing shortages which led to increased wage demand and expenses for healthcare operators. This is a current headwind for the healthcare sector in general.

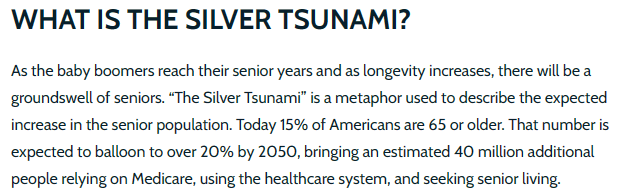

On the other hand, the “silver tsunami” currently underway is a real tailwind for Nursing and Assisted Living. As baby boomers reach their senior years there will be an increased need for senior living. Estimates are that an additional 40 million people will be relying on Medicare and seeking senior living facilities by 2050.

www.leisure.com

Compare and Contrast

One of the first things I look at when analyzing a REIT is its credit, debt metrics, and payout ratios. I want to see Funds from Operations (FFO) and dividend growth, a well-covered and high dividend yield, and attractive properties that are well diversified by tenants and location, but before all else I consider how leveraged the company is, and the safety of its dividend.

Omega has a BBB- investment grade credit rating which gives them the edge on this front. Medical Properties is just under investment grade with a credit rating of BB+.

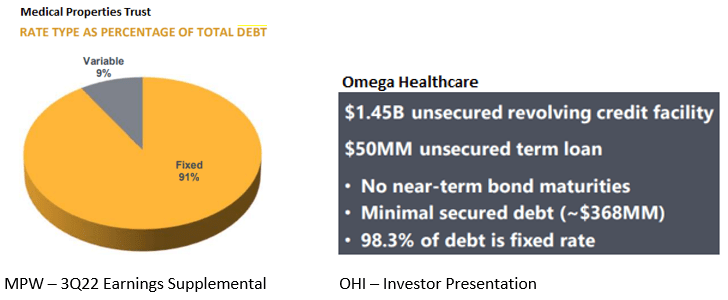

In isolation, this should give Omega a cost advantage with the rates charged on the issuance of new debt. While the debt composition for both REITs is largely fixed rate, Omega has a slight advantage with 98.3% fixed rate debt vs. 91% for Medical Properties Trust.

iREIT

Omega has good debt metrics with a Debt to adjusted pro forma EBITDA of 5.31x and an adjusted Fixed Charge Ratio of 4.1x. They also have significant liquidity with $1.38 billion available to them under their revolving credit facility.

Medical Properties has very similar debt metrics with an adjusted net debt to annualized EBITDAre of 5.8x and by our calculations an interest coverage ratio of 4.02x for the 3rd quarter (3Q EBITDAre / 3Q Interest). Medical Properties has approximately 1.2 billion in liquidity as of November 2022.

Both Omega and Medial Properties have solid debt metrics and a large amount of liquidity available to them.

OHI Presentation MPW 10-Q

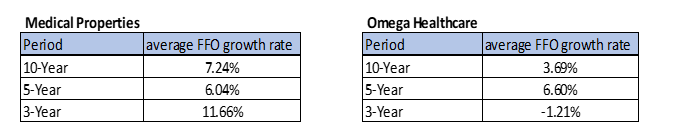

When it comes to growth in Funds from Operations (FFO), Medical Properties has the advantage here.

Over the last 5 years, Omega had a slightly higher average FFO growth rate of 6.60% vs 6.04% for Medical Properties, but over the last 10 years and especially over the last 3 years, Medical Properties has delivered superior FFO growth.

iREIT on Alpha

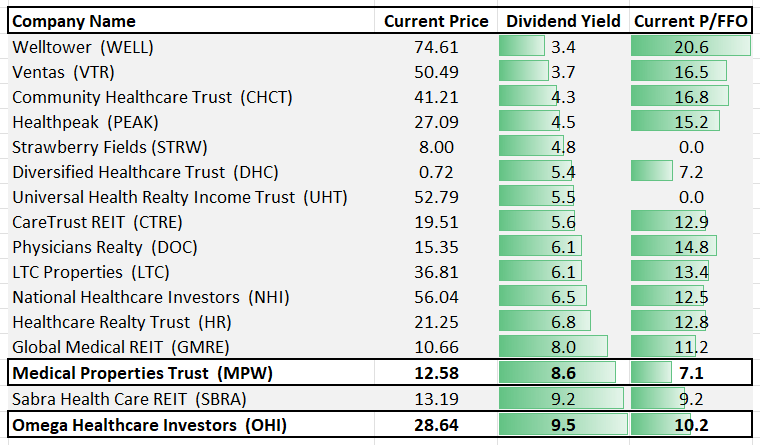

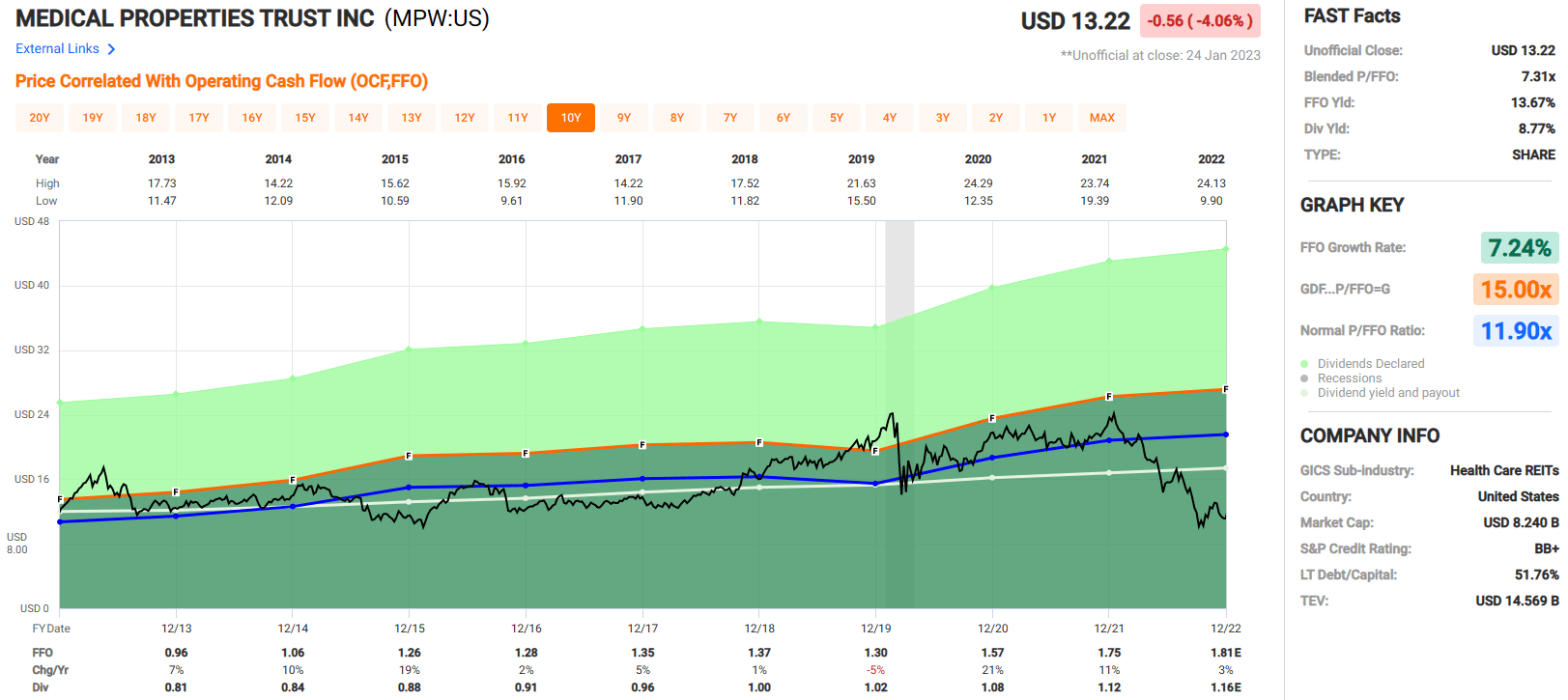

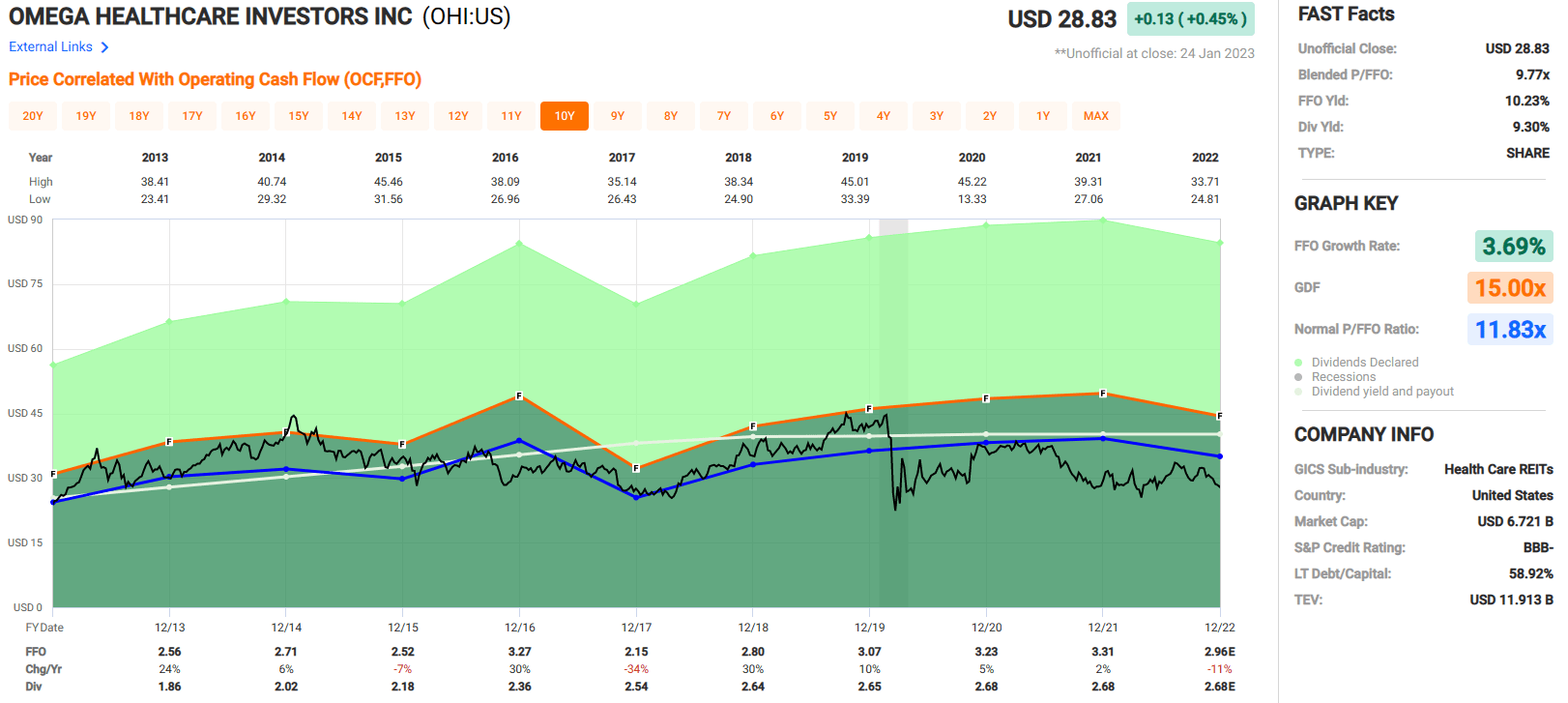

Both Medical Properties Trust and Omega have a high dividend yield of 8.77% and 9.30%, respectively, but Medical Properties has a better track record of dividend increases over the last five years with an average growth rate of 3.86% vs 1.09% for Omega.

Medical Properties Trust also has a more secure dividend with a 2022 expected AFFO payout ratio of 82.27% while Omega has a 2022 expected AFFO payout ratio of 96.75%.

FAST Graphs

Medical Properties Trust is trading at a significant discount to the multiple it historically trades at with a current blended P/FFO of 7.31x vs. its normal P/FFO ratio of 11.90x.

While not as significant of a discount, Omega is also priced at an FFO multiple below where it historically trades with a current blended P/FFO of 9.77x vs its normal P/FFO ratio of 11.83x.

Both REITs are trading at a discount to their normal valuation and appear attractively priced at these levels. We rate both Medical Properties and Omega Healthcare a STRONG BUY.

iREIT on Alpha

FAST Graphs iREIT

FAST Graphs

In Closing…

While both MPW and OHI are seeing continued operator pressures, a slowing economy and rising unemployment will help bring relief to wage pressures. As it stands right now, we believe the dividends are safe and we see good value with OHI (under $30) and MPW (under $17).

We’re continuing to accumulate shares while also maintaining responsible portfolio diversification.

Good luck and thanks for reading!

NOTE: Last week OHI declared a $0.67/share quarterly dividend, in line with previous.

Be the first to comment