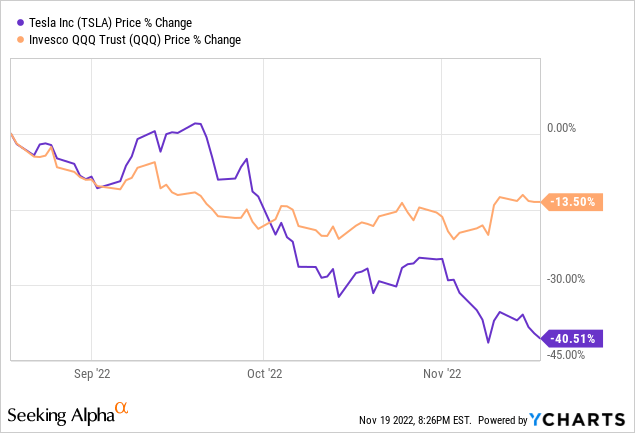

Tesla (NASDAQ:TSLA) is a high-beta stock; however, its recent underperformance relative to the market is raising eyebrows across the investing world. Despite Tesla’s exceptionally strong performance in Q3, its stock has continued to go lower in an astounding fashion. And Tesla’s stock completely sat out the recent rally in equity markets.

In my view, a multitude of factors are driving Tesla’s stock lower, and some of these factors are:

Elon Musk’s acquisition of Twitter: Elon completed a $44B buyout for Twitter at the end of October, and he sold a lot of Tesla shares to complete this deal. Since going through with this acquisition, Musk has been spending a lot of time at Twitter, and hence, Tesla has a distracted CEO. Twitter’s advertisers are fleeing the platform, and so are its employees. And Musk may need to sell more Tesla shares to finance Twitter’s business. The Twitter overhang is clearly hurting Tesla.

Macroeconomic concerns: In Tesla’s Q3 report, China sales were weaker-than-expected, and demand concerns have been growing ever since. The Chinese economy is hurting right now, and a global recession seems inevitable. If a global recession were to materialize, Tesla could suffer demand issues, and these macro fears are probably keeping a lot of investors away from Tesla’s stock (despite an aggressive valuation moderation in the stock).

Poor Technicals: The technical chart structure for Tesla remains ominous, with the stock set to break down from the right shoulder of a bearish H&S pattern formed over the last two years! This breakdown could attract tons of short-sellers, and a reverse gamma squeeze could be on. Technically, the bears are in control of Tesla’s stock, and we could see a lot more downside from here over the coming months.

In this note, we will discuss some of these factors in greater detail and try to determine if Tesla’s relatively underperforming stock is offering long-term investors a good buying opportunity.

Tesla’s Technicals Trouble

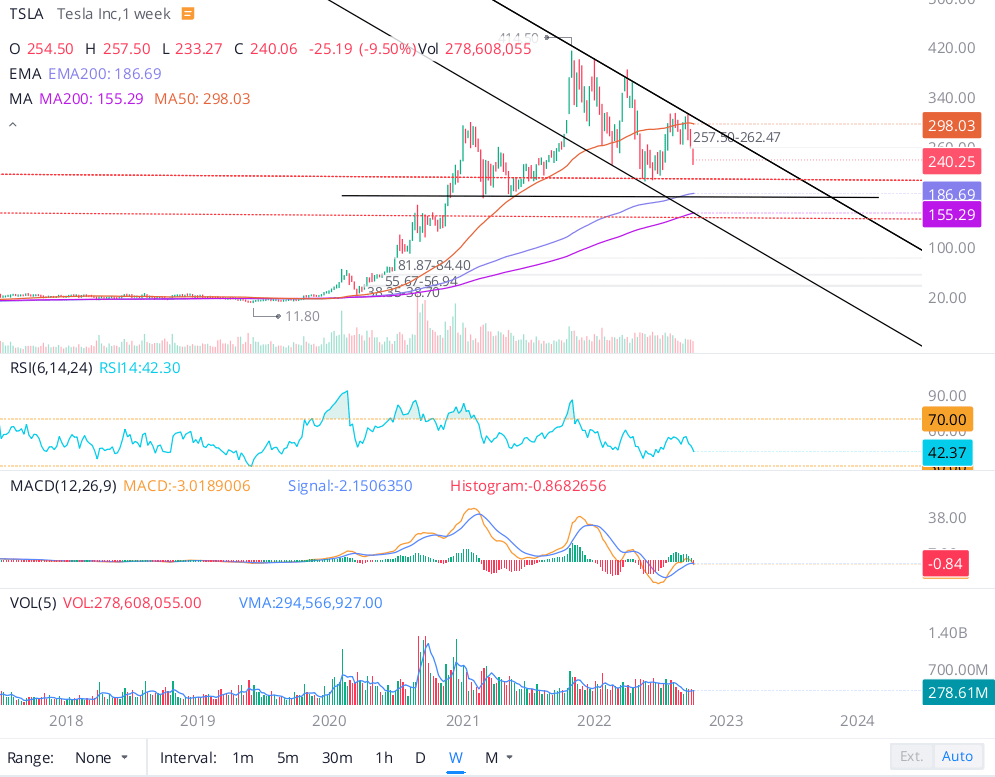

In my Q3 earnings analysis note for Tesla, I shared my thoughts on its precarious technical setup, and here’s a quick recap of the same:

As of writing, Tesla is trading at ~$240 and trying to form a base at this level after a rapid decline; however, the stock remains stuck in a falling wedge pattern. From a technical perspective, Tesla is looking nailed on to retest its 2022 lows of ~$209 (a level last seen in May), which is very close to my fair value estimate for the company.

WeBull Desktop

If Tesla fails to hold onto the psychological support level of $200, we could see a swift ride down to the $175 to $150 range. In the past, I have discussed the idea of a reverse gamma squeeze in Tesla, and such a move could come to fruition in the event of a deep economic recession hurting consumer demand for Tesla’s products amid rising competition in the EV market (yes, competition is coming in the form of traditional automakers and other EV startups).

On the flip side, if Tesla can break out of the falling wedge pattern, we could see a run up to new all-time highs ($400+) in 2023. While it is hard to see such a move in the foreseeable future due to the rising probability of a recession, the market is unpredictable, and Tesla is one of the strongest earnings growth stories in the market.

If I were to make a directional bet, it would be to the downside”

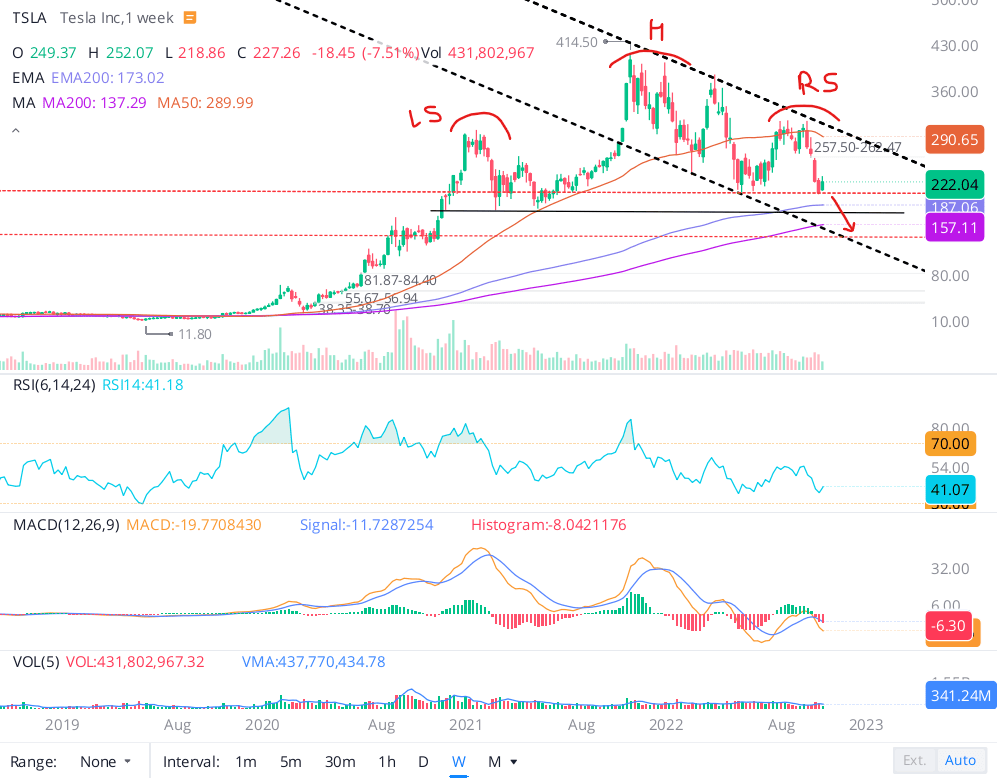

While it’s only been a couple of weeks since this research work was published, Tesla has already tested the $209 level twice and is currently trading below this level. With Elon Musk likely to sell more shares on Friday or early next week (to raise remaining funds for his $44B Twitter buyout), I could see a big test of the $200 psychological support in the coming days.

WeBull Desktop

On Tesla’s chart, we are now looking at the potential breakdown of a bearish “Head and Shoulders” pattern, which could mean a quick ride down to the mid-100s (even low-100s is possible). The prospect of a reverse gamma squeeze in Tesla is real, and despite my switch to a bullish stance for Tesla’s stock after considerable valuation moderation, I urge investors to proceed with caution. For anyone looking to buy Tesla for the long term, I see slow accumulation as the right strategy. However, if you are looking for a short-term buy, just skip Tesla for good.

Now, let us see how Tesla’s chart has evolved in the past month and try to figure out where the stock may be headed in the near to medium term:

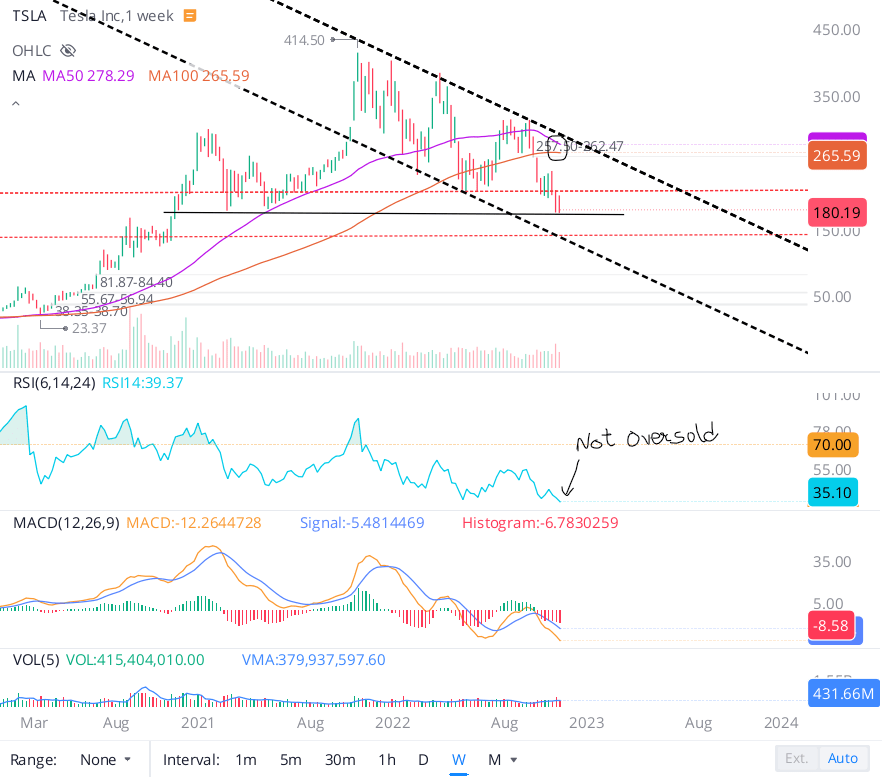

As seen in the chart below, a breakdown of the $209 level (May low) and the $200 psychological support level sent Tesla’s stock into a tailspin to hit a new low at ~$177 in mid-October. Since then, we have seen a sharp bounce in equity markets; however, Tesla’s stock didn’t participate as much in the rally and has come back down to these recent lows during a (small) broad market pullback last week. Tesla’s stock is looking quite weak, and this relative underperformance doesn’t bode well for the stock.

WeBull Desktop

Tesla has one of the worst technical charts in the equity market right now, with a confirmed breakdown of the bearish head and shoulders (H&S) pattern pointing to even more downside from here. The next big support is located on the lower trendline of the falling wedge pattern Tesla has been trading in for months, and that level is ~$140. If a reverse gamma squeeze were to materialize, I think even the low $100s are on the table for Tesla. With this precarious technical setup, buying Tesla as a near-term trade (<12 months) is simply out of the question. And any long-term investor buying here should be prepared for high volatility in this counter. After nearly two years of rating Tesla “Neutral”, I am finally a buyer here due to improving fundamentals and attractive valuation.

Tesla’s Fundamental Story Is Getting Stronger

While Musk’s acquisition of Twitter and the time he is spending there have become a big distraction for Tesla’s stock, I believe that great businesses can be run by monkeys, and Tesla is a great business. Now, I am not saying that a monkey would run Tesla better than Elon; all I am saying is that Tesla’s executive leadership has ample talent to run day-to-day operations in the absence of Elon Musk. Even before the Twitter CEO gig came along, Musk had been running the show at SpaceX, Neuralink, and The Boring Company – and while I don’t know what amount of time he previously spent and spends now at Tesla, I think it is fair to assume that Tesla can operate without Musk’s presence. In a recent court hearing, Elon Musk said that he doesn’t want to be a CEO and that he has identified someone to be Tesla’s CEO in the future. More importantly, Elon mentioned that he would be hiring a CEO for Twitter once the platform has been stabilized. In my opinion, Twitter has been a disaster for Musk, and he will refocus himself on Tesla in the near future.

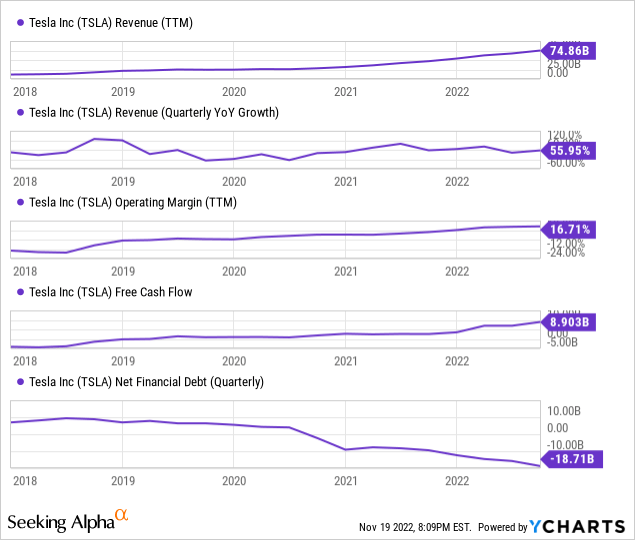

Over the last few years, Tesla has been scaling up rapidly whilst improving operational efficiency, and it is now a free cash flow generating machine. With a net cash position of ~$20B, Tesla finds itself in a very strong financial position, which is getting stronger with each passing quarter.

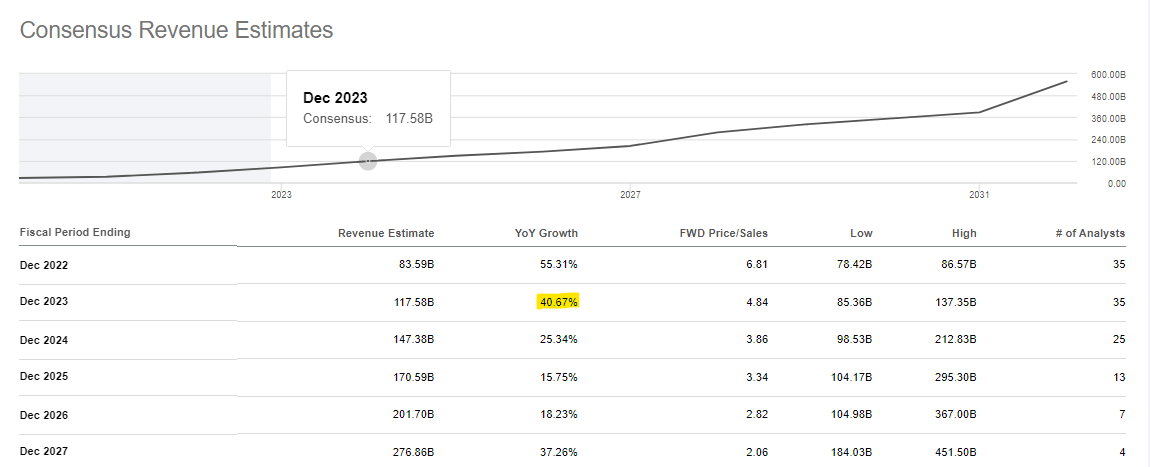

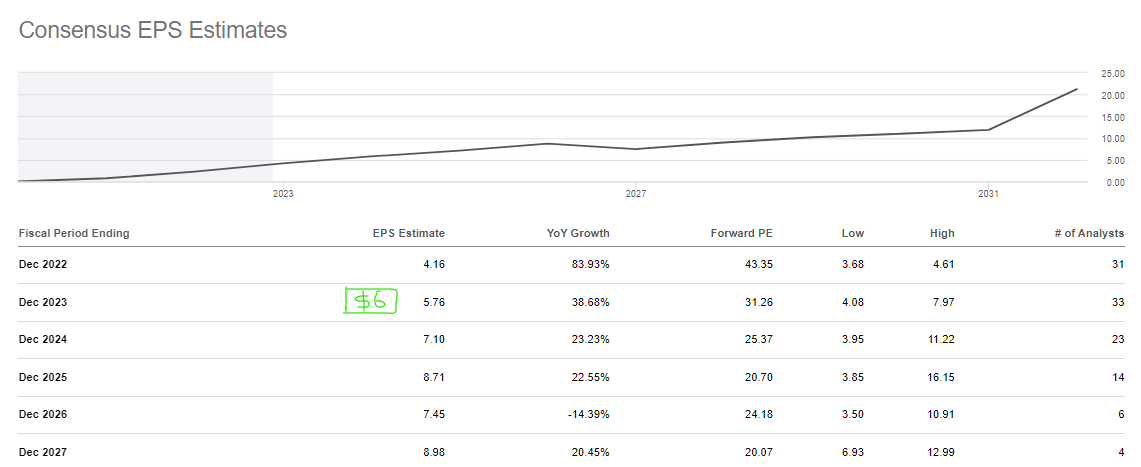

Tesla’s future looks even brighter. According to consensus analyst estimates, Tesla is set to grow revenues at a CAGR of 28% over the next five years. And earnings growth is projected to outpace revenues, as can be seen below.

Seeking Alpha

Seeking Alpha

On 1st Dec 2022, Tesla will deliver the first “Tesla Semi” truck to PepsiCo (PEP), and the company now expects to produce 100 Tesla Semi trucks in 2022. The planned scale-up for Tesla Semi trucks aims for 50K units per year by 2024. Another big product set to roll out for Tesla is the Cybertruck, which is expected to go into production at Gigafactory Texas by mid-2023. However, Tesla is looking to deliver 30 (manually-made) Cybertrucks next month. In my view, consensus analyst expectations are not fully pricing in these rollouts and ongoing scale-up in operations at Shanghai, Berlin, and Texas. I wouldn’t be surprised if Tesla were to deliver ~$7-8 in EPS next year; however, to be conservative, I have pegged my EPS estimate for 2023 at $6.

The Valuation Is Enticing

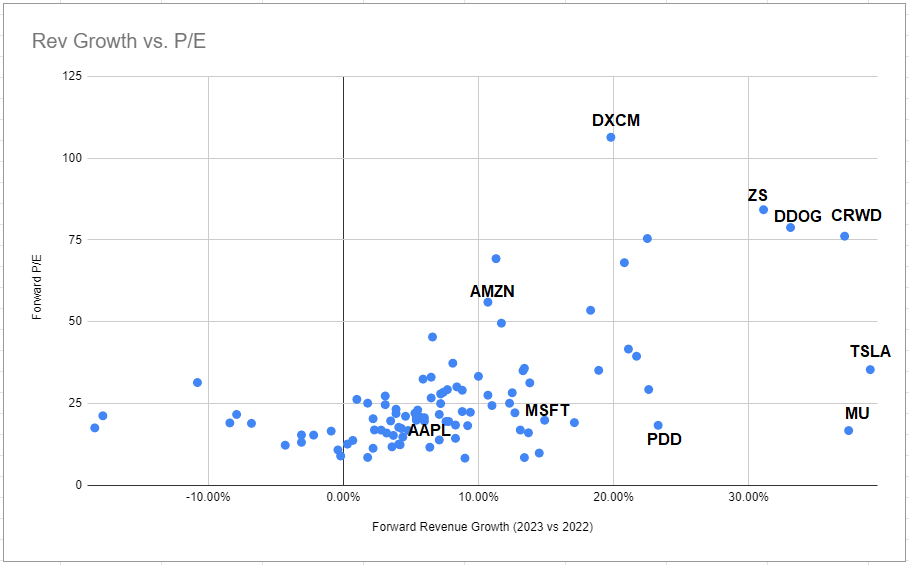

With significant improvement in financial performance (robust revenue and earnings growth), Tesla is looking very attractive at ~30x forward P/E. While Tesla trades at a premium compared to traditional auto companies, the transformational shift to EVs is still in its early innings, and Tesla is set to lead this space for years to come. Despite being one of the fastest-growing businesses in the Nasdaq-100 (as measured by next year’s revenue growth), Tesla is trading at a far lower earnings multiple than other companies with similar growth profiles.

Twitter

From a historical perspective, Tesla was only cheaper (on a forward P/E basis) during the COVID-19 pandemic crash in 2020. The macroeconomic environment remains challenging, and Tesla’s business may come under pressure next year; however, I think the secular trends powering Tesla will be in place for the next decade or two. Hence, I think any dip in financial performance from Tesla (in the event of a recession) will be temporary.

Here’s what Tesla’s fair value is looking like after its Q3 report:

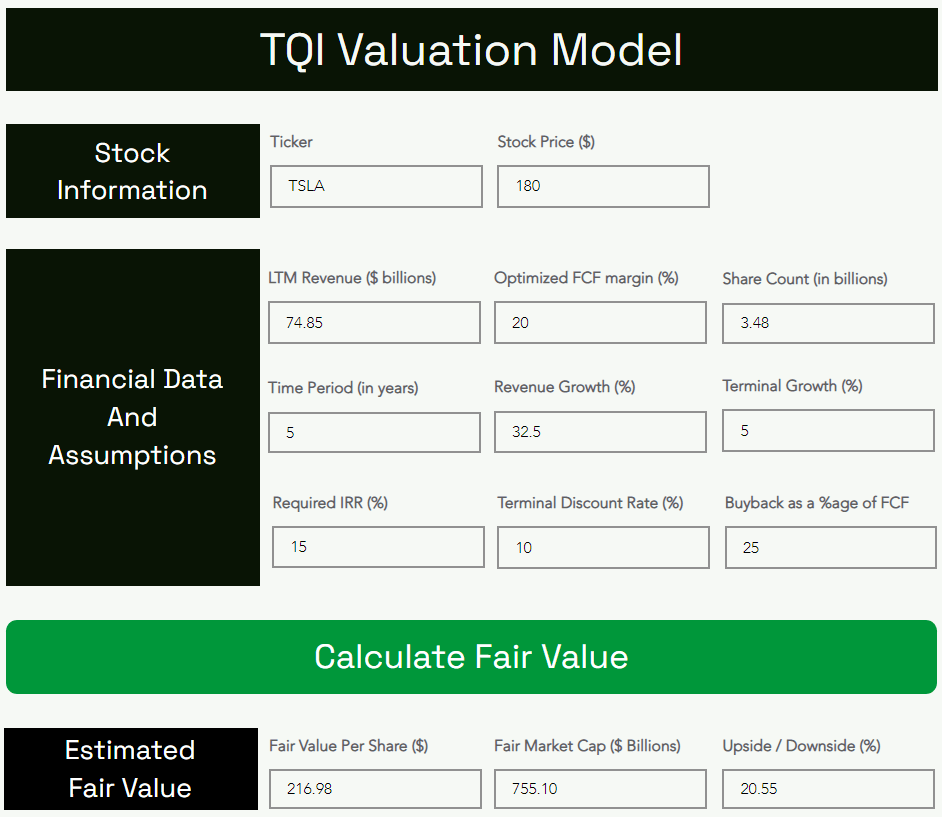

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

According to my analysis, Tesla’s intrinsic value is ~$217 per share. This means Tesla is now undervalued by ~17%. As we discussed in the past, Tesla is overshooting to the downside (and there could be more room to fall)!

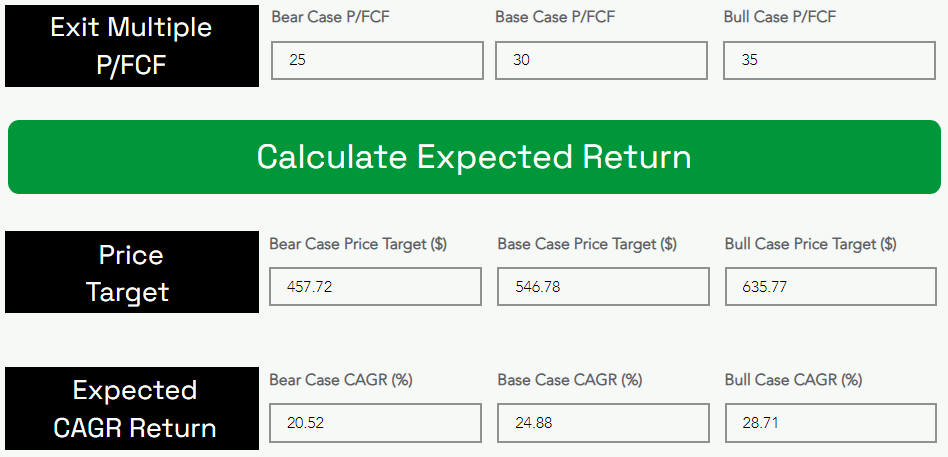

Now let’s look at expected CAGR returns for the next five years. Assuming a base case exit P/FCF multiple of 30x for Tesla, I see the stock hitting $546.78 per share by 2027.

As can be seen above, Tesla is projected to deliver CAGR returns of 24.88% for the next five years, which beats my required IRR of 20% for high-growth stocks. Hence, Tesla is a solid long-term buy at current levels.

Concluding Thoughts

Up until the last year or so, a simple “buy-and-hold” strategy worked wonders for long-term equity investors since the Great Financial Crisis. However, 2022 has been a difficult year as equity valuations have normalized (from lofty levels) due to monetary policy tightening by central banks across the globe. In the fight against inflation, I firmly believe that the FED will emerge victorious sooner or later. However, the amount of demand destruction the FED will need to cause in order to bring inflation back to the 2% target level is likely to be immense. The probability of a recession in 2023 is rising, and I don’t think we can dismiss the idea that we may already be in an economic downturn.

In Q3, Tesla’s delivery volumes fell short of expectations, and similar disappointments could continue to haunt the EV giant next year. The Chinese economy is in doldrums, and we have seen price cuts from Tesla in this market. While some fanboys have attributed these price cuts to greater scale in Gigafactory Shanghai, Tesla may very well be facing a demand issue in China. Considering the geopolitical and macroeconomic realities, I think Europe is going to experience a painful recession, and the US may not avoid one either. If we do end up going into a global recession, the demand for auto vehicles is likely to dip, i.e., Tesla could be facing a demand problem across all of its markets. From a fundamental perspective, Tesla is looking like a fantastic buy right now; however, the numbers may be about to shift negatively over the coming quarters due to macro factors.

Tesla’s stock is behaving poorly (relative to the market), which could be a sign of things to come. A breakdown of the right shoulder of the H&S pattern formed in Tesla is underway, and the stock could realistically fall down to the low to mid-100s level in the near term. For long-term investors looking to build a position in Tesla, I think slow accumulation via a 6-12 month dollar-cost averaging plan is the way to go. At TQI, we manage our risk proactively, and we are doing the same with Tesla. To guard against the ~45% downside risk (from $180 to $100), we have implemented an options-based hedging strategy (zero cost, upside limited to +25% in 7 months) to buy Tesla shares stress-free at current levels.

Key Takeaway: I rate Tesla a long-term buy at $180 per share (strong preference for slow accumulation and/or proactive risk management).

As always, thank you for reading, and happy investing. Please feel free to share any questions, concerns, or thoughts in the comments section below.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment