jetcityimage

Getting right to business, I am far from a Tesla, Inc. (NASDAQ:TSLA) bear as you can see in my articles history. But I cannot stop wondering if Tesla longs are getting into the herd mentality as 2022 draws to a close. Investing is as much about Psychology as it is about fundamental and technical indicators. “We see what we want to see” is one of my favorite Psychology quotes, and I believe this is the case with us Tesla longs here. However, I offer five reasons why I believe the worst may not be over yet for Tesla’s investors. Let us get into the details.

#1 Too many bullish calls

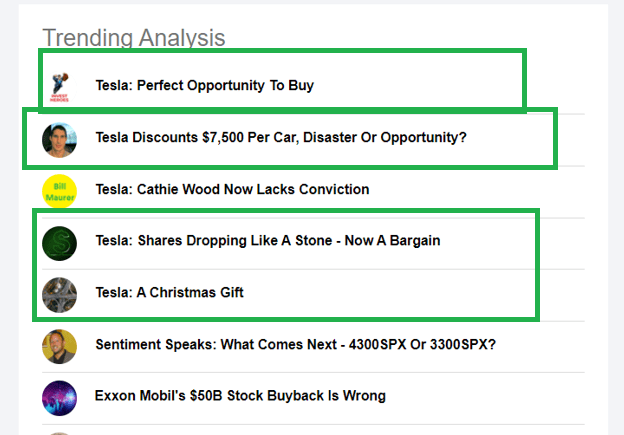

Tesla longs are hurt. Who can stomach a 70% fall on any stock and especially a darling stock with cult status? I get it because I am long, too, though not from the absolute highs, thankfully. But I am hurting. But the sentiment is still too positive for me to actually believe a turnaround is here for Tesla. As an example, as of this writing, the top 5 trending articles on Seeking Alpha are about Tesla. 4 of the 5 are generally touting this as an opportunity to buy.

Who predicted Elon Musk’s rise to the top? Who predicted this rapid fall (relatively speaking)? No one. It is not just Seeking Alpha contributors like myself who were/are still too optimistic. Tesla is still making it to the top ideas list.

To summarize this section, things turn around when you least expect it. Not when everyone is cheering from their rooftops.

Tesla Articles (seekingalpha.com)

#2 Cathie Wood – The Contrarian Indicator

Retail investors love picking on Wall Street analysts and fund managers. Just say the name “Jim Cramer” and you will notice the passion it triggers from Seeking Alpha commenters, with many retail investors arguing that doing the opposite of Mr. Cramer has helped them. It may not be an overstatement to say fund manager Cathie Wood may have taken over that baton from Mr. Cramer as being the best contrarian indicator.

If her recent history is any indication, Ms. Wood has little credibility in picking the bottom. As an example, her Robinhood Markets, Inc. (HOOD) buy reported at the end of October has not turned out well, to put it mildly. In hindsight, it appears like she picked the absolute short-term top to buy the stock as shown below, with the stock losing about 33%. In the same time frame, S&P 500 has lost about 2%.

To summarize this section, the latest news that she has once again loaded up on Tesla is not all that encouraging to Tesla longs.

Hood Chart (Google Finance)

#3 Valuation

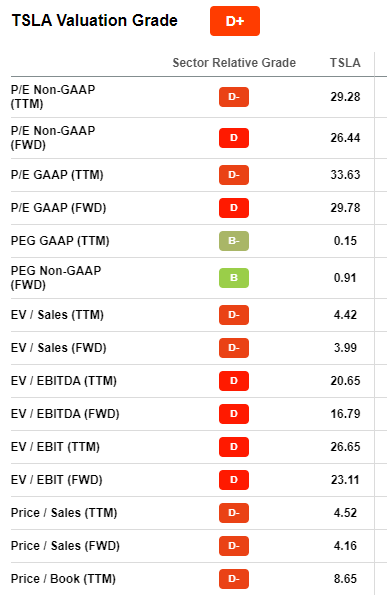

Despite the horrendous 70% fall, Tesla stock is still trading at a forward multiple of 28.50 as of this writing. Seeking Alpha’s quant ratings, while still evolving, offers a nice breakdown of various metrics for each stock and compares it to peers.

As shown below, Tesla’s Valuation Grade is still nothing to shout about. The only solace is the fact that the Valuation Grade used to “F” just three months ago. But once again, a D+ is nothing to brag about, especially in a market where plenty of stocks can be found at bargain prices, like Ford Motor Company (F). I do acknowledge that I recently wrote about Ford’s dividend being risky, but please note I am strictly talking about valuation metrics here and Ford is fundamentally much more attractive than Tesla. Granted, I may be doing an Apples to Oranges comparison here, but if you move outside Tesla’s industry, you can find many more profitable companies like Altria Group (MO) and AT&T (T) that trade at attractive relative valuations and offer relative dividend safety in this turbulent market.

TSLA Valuation (seekingalpha.com)

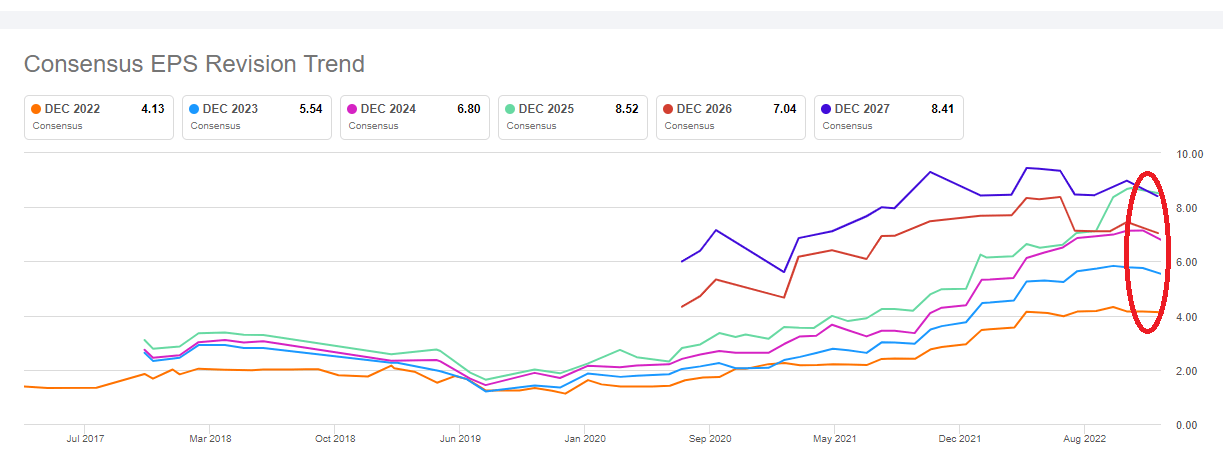

Even Tesla’s forward multiple of 28.50 is contingent upon the earnings estimates not falling below where they are. But as you can see below, even as recently as 3 months ago, Tesla’s estimates were trending higher and have just started to fall. We may have some further downside revisions to go here.

TSLA Estimates (seekingalpha.com)

To summarize this section, even if Tesla meets earnings estimates, the market may not be willing to assign the multiple of yesteryears, also known as multiple compression.

#4 Technicals

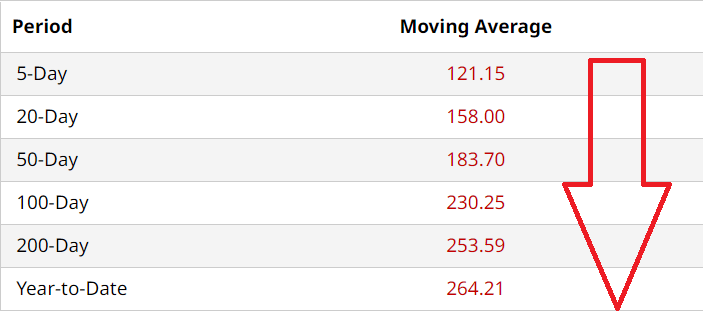

Whether you believe technical analysis is the best thing since sliced bread or are akin to reading tea leaves, they offer valuable insight on the short- to medium-term prospects. Tesla’s stock is just in an endless death spiral technically, with the stock trading well below its 5-, 20-, 50-, 100- and 200-Day moving averages. The 200-Day moving average is considered the most important indicator among these, and Tesla’s current price is more than a double bagger away from.

To summarize this section, please remember it also may be darkest before pitch black.

TSLA Moving Avg (barchart.com)

#5 Discounting – Good or Bad?

The words “Discounting” and “Premier” rarely go together. But that is precisely what is happening with Tesla now with the reported $7,500 discount per car. Is this a sign of desperation or a smart way to clear inventory? Will this impact the profit margin or will the volume make up for the reduction in margin? I enjoyed this Seeking Alpha article on this subject, and I am pondering those questions. In short, no one knows yet.

To summarize this section, expect a terrible whiplash if Tesla’s Q4 deliveries disappoint despite the discounting.

Bonus and Conclusion

Despite all the factors mentioned above, in my opinion, the elephant in the room for Tesla remains Elon Musk. While some Seeking Alpha readers believe he may have alienated the Tesla base with his recent political stance, I believe he still has the clout and charm to win investors’ trust back if they are convinced his mind is firmly back on Tesla. After all, money knows no party. I firmly believe Musk meaningfully disconnecting himself from Twitter will be the spark that ignites Tesla’s turnaround. I remain long here as the long-term (at least 3 years) risk-reward appears to favor the longs, but my expectations are grounded.

So, that’s my contrarian take on the recent surge in Tesla bullishness. What is yours?

Be the first to comment