Margarita-Young/iStock Editorial via Getty Images

Shares of Tesla (NASDAQ:TSLA) have been pummeled amidst a multitude of headwinds arising over the past few weeks, falling over 45% since last warning of major headwinds from October. With shares having shed $800 billion in value from April’s $1.19T valuation to reach the lowest level in over two years — at a $390 billion market cap — shares could be an attractive Christmas gift to some investors. Let’s dig into the details to find out if shares really are attractive at these two-year lows.

Fundamentals Intact & ‘Relatively’ Cheap

The 37% December decline has brought shares back to more reasonable valuations not seen in more than two years — and at levels that can be attractive to investors with a longer time horizon.

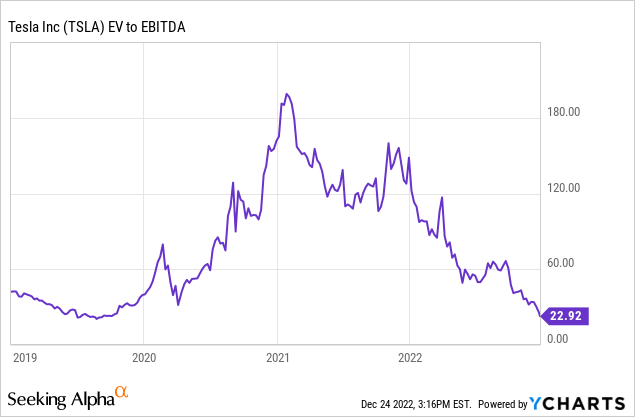

EV/EBITDA is at its lowest level since September 2019, with Tesla trading at 23.4x TTM EBITDA of $16.01 billion. FY23 EV/EBITDA is expected to further improve with Tesla trading at ~15.1x projected EBITDA of ~$24.9 billion.

EBITDA margin has shown consistently strong growth, reaching 21.4% in Q3 2022 from 8.9% in Q4 2019 as volumes scale; further volume growth in FY23 as Berlin and Austin could provide ample room for margin expansion. A 22% EBITDA margin for FY23 equates to ~$24.9 billion in EBITDA on $113 billion in revenues (approx. +40% growth from $81 billion in revenues for FY22).

Profitability has also been quite strong, boosted by software and higher-trim models — TTM net profit margin is approaching luxury segment manufacturers Porsche AG (OTCPK:POAHY) and Ferrari (RACE) at 14.95%. Expanding net margin as revenues crest past $1 billion opens the door for further earnings growth over the next six to eight quarters.

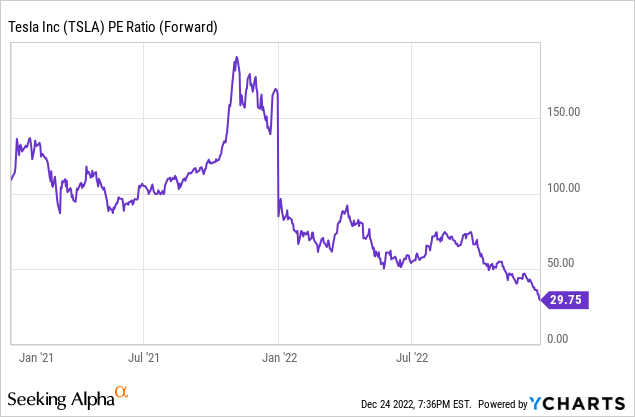

Tesla’s PEG has dropped to rather attractive levels to value-seeking investors, with a relatively conservative ~30% y/y growth rate in EPS modeled to account for impacts from a challenging auto market, discounts offered and possibly lower ASPs, and forex. At such growth, FY23 EPS would be modeled to ~$5.10, for a forward P/E of ~23.9x and a PEG of just under 0.8.

Tesla

Although legacy OEMs such as GM (GM), Ford (F), and others trade at much lower valuations — 5x to 8x forward EV/EBITDA, 5x to 7x forward P/E, etc. — Tesla offers market-leading access (albeit with multiple headwinds) to a growing EV industry, with much higher revenue, EBITDA, and EPS growth rates. For example, Tesla is over 40% forward revenue growth potential and over 30% EPS growth, compared to single-digit growth rates for GM.

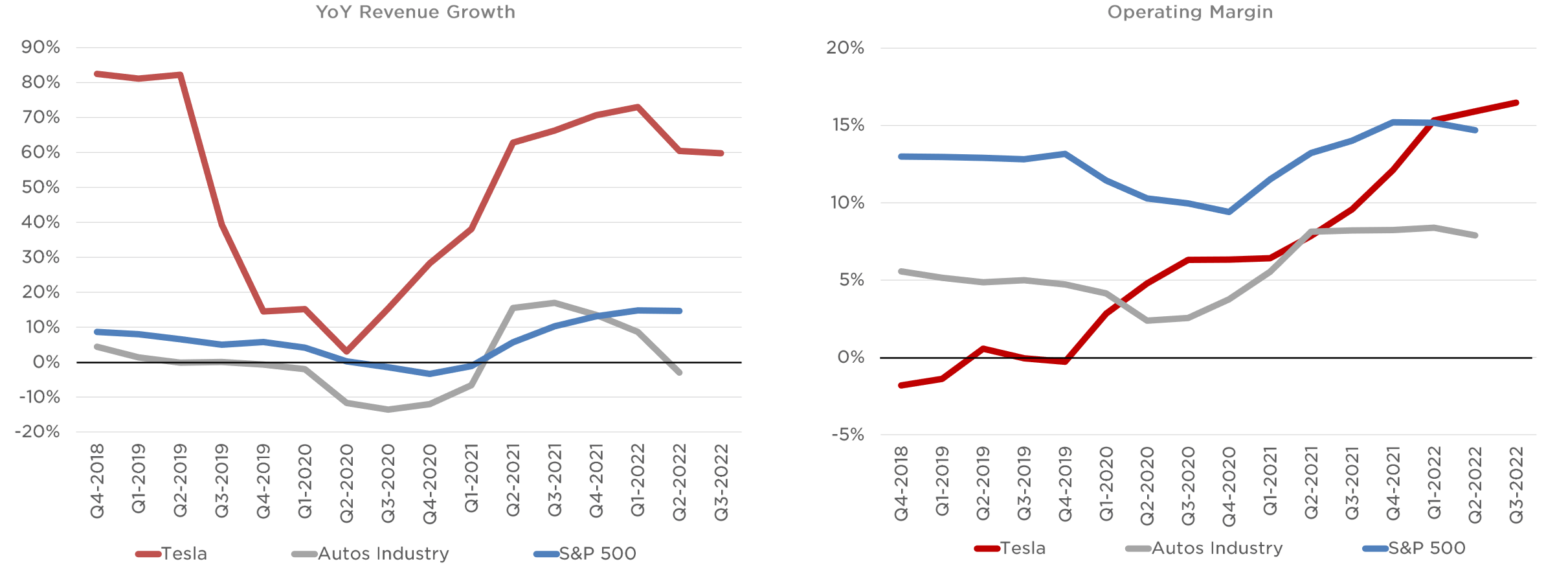

A look at the chart above demonstrates Tesla’s exceptional fundamental performance relative to both the auto sector and S&P 500 (SPY). Tesla is consistently recording stronger y/y revenue growth rates, most recently recording about 60% y/y revenue growth compared to a decline for the auto sector and about 15% for the index. Operating margins have now exceeded both the auto industry and index average.

From a fundamental standpoint, Tesla’s recent nosedive has brought the stock to metrics not seen in over two years, with shares relatively attractive with PEG and EV/EBITDA in a fair range for the growth at hand.

Weaknesses Ahead

Aside from a possible challenging pathway for strong earnings growth in 2023 due to a distressed auto market and adverse impacts from forex, Tesla could be facing multiple other headwinds in the year ahead. Let’s be honest — Tesla trades more on sentiment than fundamentals, and the narratives surrounding Musk’s stock sales and role in Twitter have had a significant negative impact on share price.

Moving forward, regulatory pressures and issues with FSD/Autopilot may play more of a role, and increasing competition and market share issues also are coming into the limelight as more ICE manufacturers kick off EV deployment.

FSD & Regulatory Issues

FSD is facing a rough stretch — California passed Senate Bill 1398, which would “require a dealer or manufacturer that sells any new passenger vehicle that is equipped with a partial driving automation feature” to accurately describe the feature’s capabilities and limitations. SB 1398 also would “prohibit a manufacturer or dealer from deceptively naming or marketing” such a system, a direct aim at Tesla’s ‘Full-Self Driving’ system, which is also facing a handful of lawsuits and national investigations.

A class action lawsuit alleges Tesla has failed to reach long-term goals regarding FSD’s development and has misled consumers about the technology becoming fully self-driving with software updates. NHTSA has been investigating FSD and Autopilot over a string of more than 41 crashes, following two recent crashes — one of which the driver claimed FSD malfunctioned, braking to 20 mph on I-80 and causing an eight-vehicle pileup with injuries.

Competition & Market Share

Competition in the EV industry is expected to ramp up later in FY23 through FY25 as ICE majors roll out EV strategies and begin producing and delivering EV models at scale. Increasing competition will increase the need for Tesla to maintain double-digit market share by continuing to scale production volumes to beyond 2.5 million by FY24.

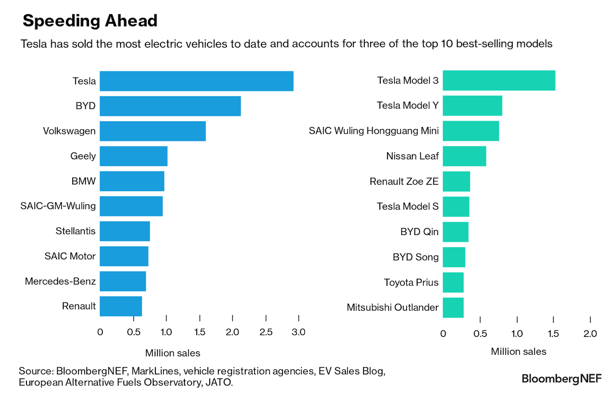

For FY21, Tesla held about 14% market share globally for EVs, and is projected to hold about 13% market share in 2022 based on projections for about 10.5 million EV sales. Data from Counterpoint Research shows Tesla’s Q3 EV market share at 12.6%, reaffirming the trajectory for approximately 13% market share. Estimates for ~14 million global EV sales in 2023 would correlate to approximately 13.5% market share for Tesla, assuming 45% delivery growth to 1.9 million vehicles.

BloombergNEF

As of August 2022, Tesla held the top spot in both cumulative EV deliveries and the two top selling models. Although the gap has narrowed to less than half a million vehicles between Tesla and BYD (OTCPK:BYDDY), the challenge lies not within one manufacturer overtaking Tesla’s crown, but rather a handful of manufacturers all pushing EV volumes higher, and the group squeezing Tesla’s share. However, a market share squeeze is not expected until FY24 or FY25 when major ICE OEMs begin pushing EV volumes at scale.

Outlook

Shares slumped more than 20% in the lead-up to Christmas as Tesla faces fallout from CEO Musk’s purchase of Twitter, offering a $7,500 discount, a slump in the broader markets, and more.

Discounts and increased reliance on China, which contributes a hefty 35% of deliveries, are a dark cloud moving forward for ASPs, although the scaling of higher-priced Model Y production in Austin and Berlin should offset such impacts. Regulatory impacts and any fallout relating to the sale of FSD could prove to be influential, should such an event occur; the high-profile investigations and legal challenges surrounding the software are tarnishing reputation and R&D success. Competition and market share threats are on watch, though not expected to have a massive impact in FY23.

Fundamentally, shares have dropped to more attractive levels, shaping up to be a Christmas gift for a patient investor — forward EV/EBITDA has dropped to levels not seen since September 2019, with forward P/E dropping below 24x with EPS growth potential at 30% or higher. PEG has fallen to about 0.8 based on ~30% EPS growth, offering an attractive entry for keen investors after a rapid slump into oversold territory with a bounce likely on a technical basis.

Although Tesla tends to trade heavily on sentiment rather than fundamentals, the fundamental picture is clear, after shedding $800 billion in value. Significantly stronger revenue growth than the auto sector, strong EPS growth, and expanding EBITDA and net margins paint a positive picture for shares in the long run. However, issues arising from Musk’s complicated purchase of Twitter, legal challenges and adverse impacts from FSD’s capabilities and marketing, concerns about market share, and more are still likely to weigh heavily on shares.

Be the first to comment