KanawatTH

Recommendation

I believe Telos Corporation (NASDAQ:TLS) is fairly valued. The positive part about the business is that cybersecurity is becoming increasingly important, especially as businesses undergo digital transformation and rely more on technology. TLS portfolio of product offerings is well-positioned to ride on this wave. The negative is the near-term weakness that TLS is expected to go through. As the current investment environment is unforgiving to bad narratives, I believe it now is not the right time to invest in TLS.

Business

TLS provides software-based security solutions that protect businesses from threats. Its security offerings help businesses and governments protect their assets, expand into new markets, and satisfy their constituents.

Cyber security is getting more important now than ever

I think a lot of companies are currently undergoing what I call “digital transformation.” As a result, the vital information technology systems upon which their prosperity and safety depend are experiencing strain, threat, and attack on a scale never seen before. Even more so, customers have a hard time planning for future growth in the face of disruptive technologies and economic uncertainty. Today, there are a wide variety of changing security threats that modern businesses, public and private, must contend with.

Many types of institutions, including businesses, are becoming increasingly dependent on technological tools. Also, increasingly both data and applications can be hosted locally, in the cloud, or in a hybrid setting. While increasing management over operational systems is a benefit, bringing IT and operational technology [OT] together increases the enterprise’s overall attack surface. When thinking about today’s technological landscape, the cloud is inescapable. Businesses and government agencies alike are moving quickly to adopt hosted and cloud infrastructures. The cloud’s rapid application development and increased flexibility are enticing an increasing number of businesses and even highly secure government agencies to migrate their operations there.

In addition, enterprise technologies are inherently risky due to their interconnected nature and their ability to extend beyond the confines of the organization. The cloud, in particular, raises the difficulty level because of the interdependence of various elements in cloud management.

TLS flagship product: Xacta

For automating security compliance and managing cyber risks across an organization, Xacta is the go-to platform. The United States Federal Government uses Xacta as their standard commercial cyber risk and compliance management solution.

Twenty years ago, Xacta was introduced as an alternative to the time-consuming and inefficient methods of doing business used by conventional consultants and government contractors. Xacta has matured over time to streamline workflow-based automation of security risk and compliance activities. Xacta automates a large portion of cyber risk and compliance management’s manual processes, cutting down on the need for costly time-and-materials consulting. Further, Xacta provides the advantage of continuous monitoring, which is extremely difficult to accomplish manually.

I believe Xacta has reached a tipping point in the market where resellers and the channel can no longer ignore it because it is the de facto solution across the United States Federal Government. The way TLS can win over more channel partners and boost sales is by reassuring them that they are not in competition with them. TLS is merely a tech firm that is constantly working to enhance their security compliance automation software platform.

FedRAMP drives adoption of Xacta

Xacta is a quick way for individuals to become compliant for working with the government, and the government is increasingly requiring Federal Risk and Authorization Management Program (FedRAMP) compliance.

TLS’s cloud-first strategy has led to extensive partnerships with other cloud providers like Rackspace Technology, Inc., which aids SaaS providers in achieving federally mandated cloud compliance standards like the FedRAMP. The truth is that the government requires many distinct SaaS applications. As a result of Xacta’s ability to ease security compliance requirements, these companies have seen increased cloud adoption, usage, and revenue. As a result, I believe businesses that focus on the cloud regard Xacta’s features as a competitive advantage.

Proven product that works

To convince myself that a security product is worth adopting, I would want to see that it has been widely accepted and is effective, but that may just be me. It has been proven that TLS’s product is effective in this regard. It has proven its ability to secure and maintain enterprise-level contracts, and it also offers crystal-clear insight into expected revenue and profit.

I believe that the combination of the existing contracts, acquisition vehicles, and customers will serve as a sturdy stepping stone to further expansion. TLS has also proven time and again that it can implement enterprise-level security solutions for both government and private sector organizations. The most important benefit is the stable income and high profit margins that come from these long-term contract relationships.

TSA issuance of Authority to Operate is good news

TLS has been granted an authority to operate [ATO] by the TSA for a limited public trial. Due to the importance of validating systems and processes before full authorization, a limited number of applicants have been given the opportunity to enroll in the PreCheck program. Fortunately, the opportunity for TSA in CY23 is expected to grow throughout the year and is currently estimated by management to generate revenue of $30 million on a net run rate basis. In the long run, I think the increased accessibility of non-airport locations will help to increase the number of customers significantly above the current level.

Operational hiccups dampen near-term outlook

Despite Telos’ plans to expand its TSA PreCheck enrollment service in fiscal year 23 (FY23), TLS expects its revenue to drop by 15% due to weaker-than-expected growth in Secure Solutions and fewer contract wins in Secure Networks. In addition, Xacta’s success has been slower than anticipated due to TLS’s lack of significant sales through Microsoft and AWS. To make things worse, TLS’ Sales team size, which peaked at more than 60 after increasing from 8, has been cut to around 30 in recent months.

While Telos remains bullish on resale thanks to its IBM partnership, Xacta’s adoption outside of the Government vertical appears to be on the decline. Even for the TSA, this portrayal of the future is much gloomier than previous expectations.

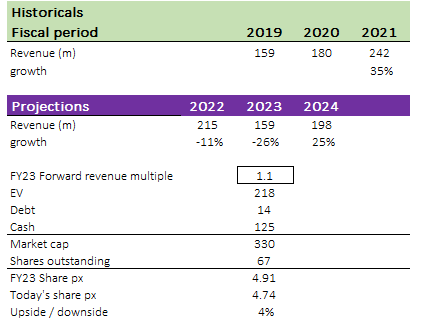

Valuation & model

Using consensus estimates, I believe TLS is fairly valued at the current share price. The premise of my model is that TLS will face serve near-term headwinds in FY23, which is guided by management. And it seems that this guidance is already baked into the valuation and share price (stock chart is horribly ugly). While I believe the long-term secular uptrend in cybersecurity, this is not a stock that I like to participate in at this time.

That said, we could possibly see an inflection in multiples maybe during 2H23 when management starts commenting about FY24. Hopefully, the outlook given by then would be a lot better than what was given in the last earnings. That would certainly drive a better narrative and the stock valuation up. As of now, I assume no change in valuation.

Author’s own calculations

Risks

Competition

Competing products and services can cloud the market’s view and obscure the benefits of TLS product, since it is not easy to differentiate to competing cybersecurity product. There is a risk that this will slow Telos’ expansion.

Pricing pressure

Despite what I believe to be less competition in TLS’s pricing power compared to other companies, it is still a risk. Nevertheless, TLS should be less vulnerable to competition thanks to the company’s well-established position within the U.S. Government and the absence of significant rivals in the market.

Summary

Overall, TLS is a strong company with a well-positioned portfolio of products in a growing market. However, they are currently facing near-term challenges, and the current investment environment is not favorable for companies with negative narratives. Therefore, it may not be the best time to invest in TLS.

Be the first to comment