Alexey Bakharev

The shipping industry has been one of the best-performing sectors in recent years, benefiting from the general shortage of large vessels after years of low industry investment. The oil tanker industry has had a solid performance, gaining from both the shortage of shipping vessels and the increased need for global oil transportation amid the geopolitical and economic breakdown of certain trade relationships, notably, oil exports from Russia to Europe and the ongoing disruptions in the Red Sea.

With improved profitability, key oil shipping stocks such as Teekay Tankers Ltd. (NYSE:TNK) have dramatically lowered their liabilities, giving way to immense free cash flow. Currently, TNK offers an outstanding FCF yield of 30%. Of course, we must consider that its income is not expected to remain stable over the coming years at current levels, as it is benefiting from a confluence of events that significantly improve tanker shipping rates. That said, if the various economic and geopolitical trends that have created this situation continue, Teekay may maintain its current high profit position.

I was very bullish on TNK in 2020 but downgraded TNK to a “hold” last year due to ongoing concerns regarding the Petrodollar system. To me, investors should continue to weigh how the efforts of BRICS countries to distance themselves from the US system may hamper global trade, particularly in oil. With the increased Middle Eastern geopolitical strife, the risk seems to be significantly reduced as key exporters like Saudi Arabia and Qatar work to keep their oil-based economies afloat.

TNK’s valuation is notably higher than last April, with a particularly strong surge since October, as the company is likely seen as a hedge against the Middle East. Fundamentally, as Red Sea trade breaks down, the demand for long-haul shipping that Teekay provides will likely rise. Further, we continue to see increased US-Europe oil trade across the Atlantic, opening the door to a potentially prolonged supply and demand imbalance in the tanker market. With this in mind, it seems an opportune time to reanalyze Teekay’s economic position and valuation.

Expect Strong Margins for Years

As with most shipping stocks, Teekay is exposed to substantial cyclical risks as demand for shipping changes more dramatically with the global economic cycle. A small supply and demand imbalance in the market can cause massive swings in shipping rates as both the supply and demand curves are somewhat inelastic. In other words, recessions lower import demand for oil, but only by so much, with less change than most in a downturn. Further, increased shipping rates do increase shipping vessel supplies, but only after several years, as it takes time and resources to construct new tankers. Thus, if the market is in a shortage, that shortage can last, mainly if external issues such as geopolitics influence the market.

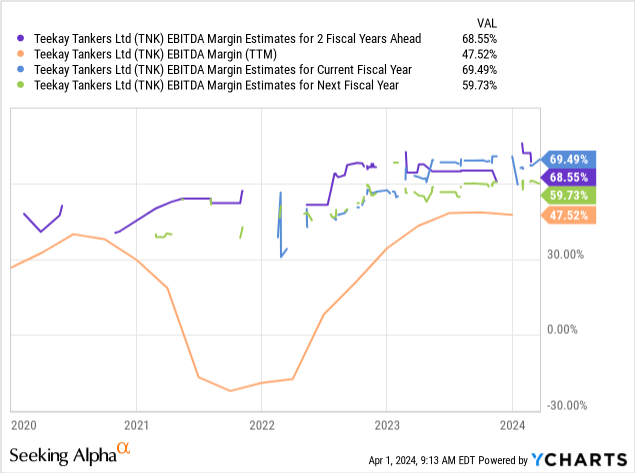

The company’s 2024 consensus EPS is $13.75, giving it a forward “P/E” of 4.25X. Based on analysts’ consensus, its EPS is expected to remain nearly that high until at least 2026, implying that other analysts expect the tanker shortage to last. Its EBITDA margins are expected to climb from a 47% TTM level to 60-70% over the next two fiscal years. See below:

The consensus points to TNK earning a total EPS of about $40 over the next three years. Assuming its EPS will be sustained to a degree beyond 2026, then TNK will likely earn back all of its current market capitalization by 2028-2029, indicating it has a very low valuation today. Still, TNK also often operates at a loss and may again if the supply and demand imbalance is fixed.

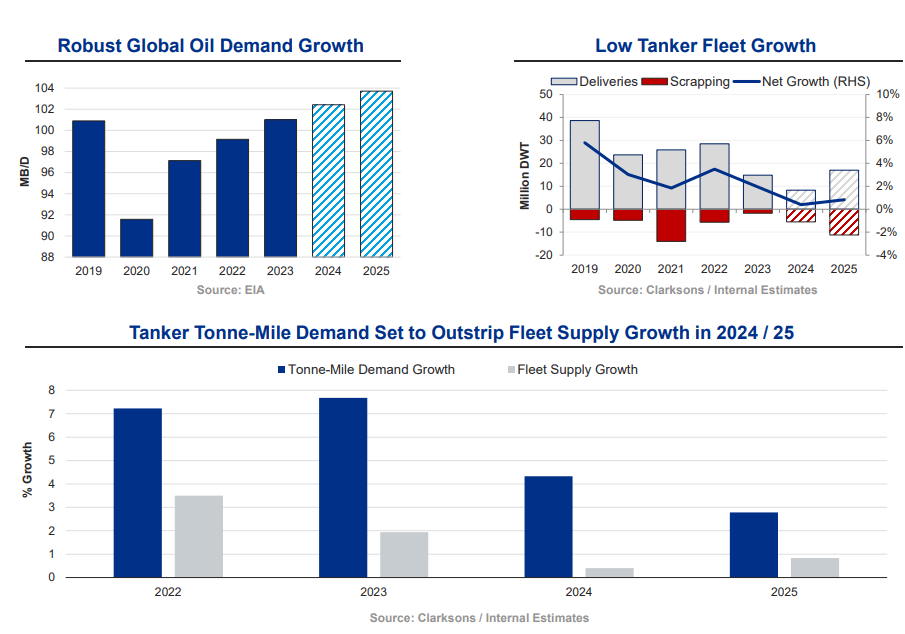

That said, there is likely more evidence of an increased net shortage than a return to the 2010s glut. For one, the global oil tanker fleet growth will continue to fall this year and next. Demand growth will also likely slow, but the overall demand-supply gap will likely grow by then. See below:

Teekay Tankers – Tanker Supply Demand Outlook (Teekay Tankers Q2 Presentation)

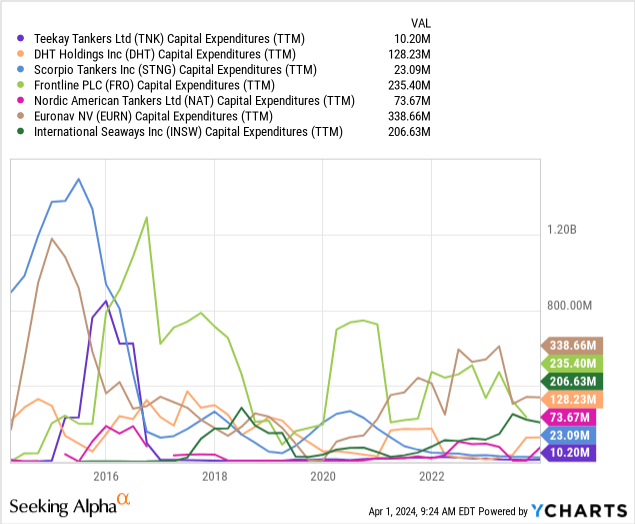

At the least, this data points toward a continued, albeit slower, trend toward a net tanker shortage through 2026. Given their very high-profit margin levels, we would typically expect oil tanker companies to increase spending on new vessels. That said, amid the precarious trade environment, many appear reluctant to do so, even more so because most are repaying debt that was taken on during the glut from 2015-2020. Therefore, CapEx levels for most tanker companies remain generally low, only rising slightly since before 2020. See below:

As long as these companies are not dramatically raising their CapEx spending, we should not see a large boom in oil tanker supplies. Even then, due to the time lag in production, it would still take well over a year for that to impact the market.

A decline in high-demand growth offsets this low-supply growth. The demand side of the equation is difficult to predict because it is so exposed to the various events in critical countries and between them. If all were stable, I would expect little demand growth as countries focus on using cheaper oil pipelines to trade oil, with total oil demand hardly growing worldwide.

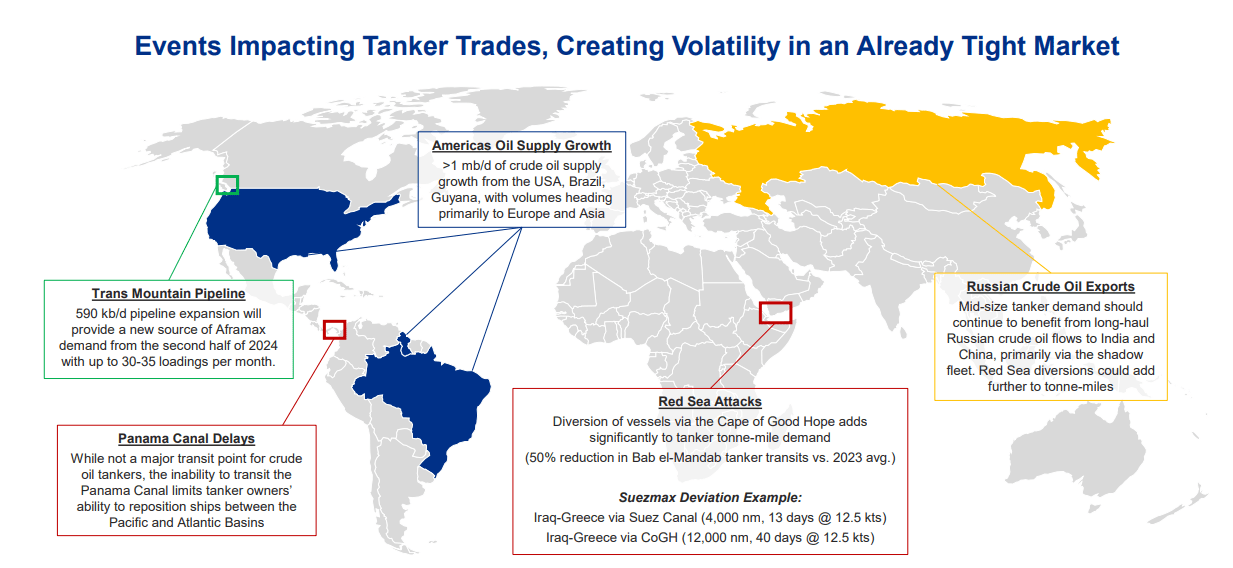

Still, the geopolitical environment has created a goldilocks market for Teekay. The oil embargo disrupts Russia’s flows. See below:

Global oil tanker geopolitical demand drivers (Teekay Investor Presentation Q2)

Realistically, the oil embargo has done little to stop Russia from exporting oil or from the Kremlin earning a profit. Instead, Russia sells oil to countries that resell it, artificially increasing the trade route length. With the Red Sea attacks and the Panama Canal drought, global trade is beginning to look more like it did centuries ago, with vessels traveling around the southern capes dramatically increasing distance, lowering free vessels.

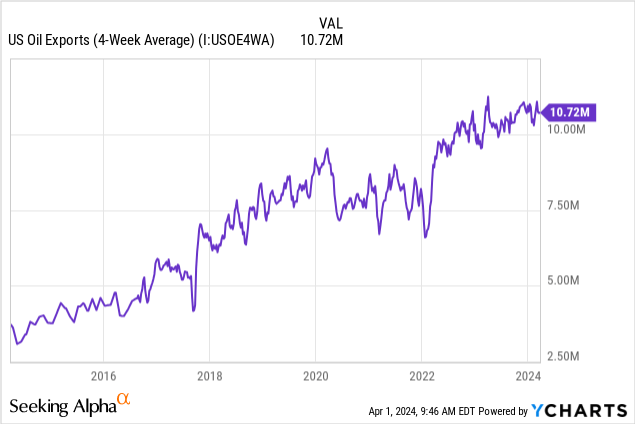

Further, US exports of oil have markedly increased in recent years, primarily driven by increased demand from Europe to offset lower Russian imports. See below:

In my view, the critical question is whether these demand drivers will continue to push the market or if they will last. When I covered Teekay last, most analysts and I viewed it as unlikely that shipping demand would remain high for too long, considering the situation with Russia and Ukraine would eventually normalize. That was a year ago, and much has changed since then. It seems unlikely that the situation will normalize, particularly now that the Middle East and Africa also face internal and external conflict.

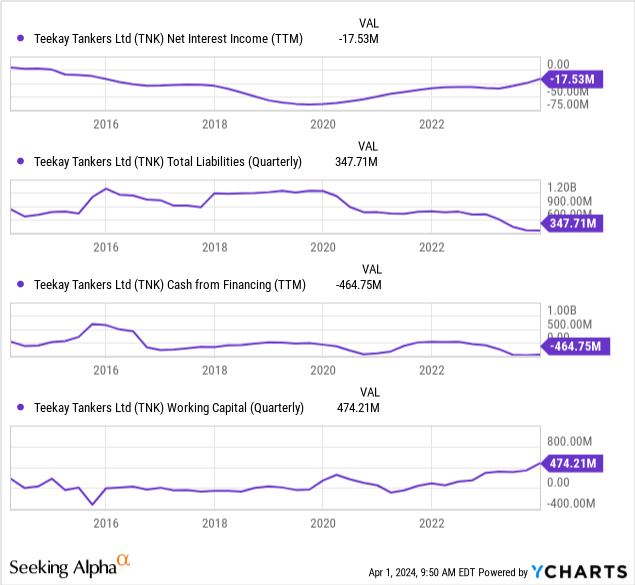

Until then, Teekay’s balance sheet quality is significantly bolstered by its effort to reduce debt, increasing its value even if the macroeconomic backdrop sours. In 2020, Teekay was at bankruptcy risk as its interest costs soared amid high debt and negative working capital, resulting from years of negative cash flows. Today, its liabilities are around 70% lower as its interest costs are nearly negligible, stemming from an immense focus on repaying debt (see cash from financing). Even more, its working capital has turned to a positive $474M, with $365M in cash. See below:

Teekay’s balance sheet is solid today. Since it has focused on using its profits to reduce its burdens instead of dividends or increased vessels, it is no longer at risk of bankruptcy. It can likely survive a period of negative earnings since its total liabilities are lower while its liquidity position is stellar. Indeed, its growing hoard of cash is also of great value to investors as they may eventually be paid out as a dividend or used to make income-improving investments.

The Bottom Line

Overall, I am cautiously bullish on TNK today. Its price to forward EPS based on two-year expectations is 4X, which is typical for the company in recent years. That said, its liabilities are much lower, and it continues to trade at a “high bankruptcy risk” valuation when that risk is now shallow, even if the economic fundamentals manage to change dramatically. Realistically, I believe the macroeconomic fundamentals will remain nearly where they are, with the shortage of tankers not growing but not fading at TNK’s low valuation points.

At its current price, the overall upside in TNK is much lower than it was when I first became bullish in 2020. That said, TNK’s outlook is far more stable today than it was then or even in 2023, as the geopolitical environment has become entrenched in a manner that should improve oil trade volumes, and its balance sheet continues to improve. With such a low “P/E” and high working capital compared to its market capitalization, I believe TNK is undervalued and represents a solid long-term investment.

Still, TNK investors face risk due to potential changes in the geopolitical environment, particularly if key Middle Eastern countries distance themself from the US, as I continue to believe is more likely than many would like to admit. Further, a global recession may lower oil trade and harm TNK’s profitability, potentially being one of the more significant risks facing TNK today.

Be the first to comment