wwing

Note: This article originally appeared in the Daily Drilling Report on Saturday, the 21st of January.

Introduction

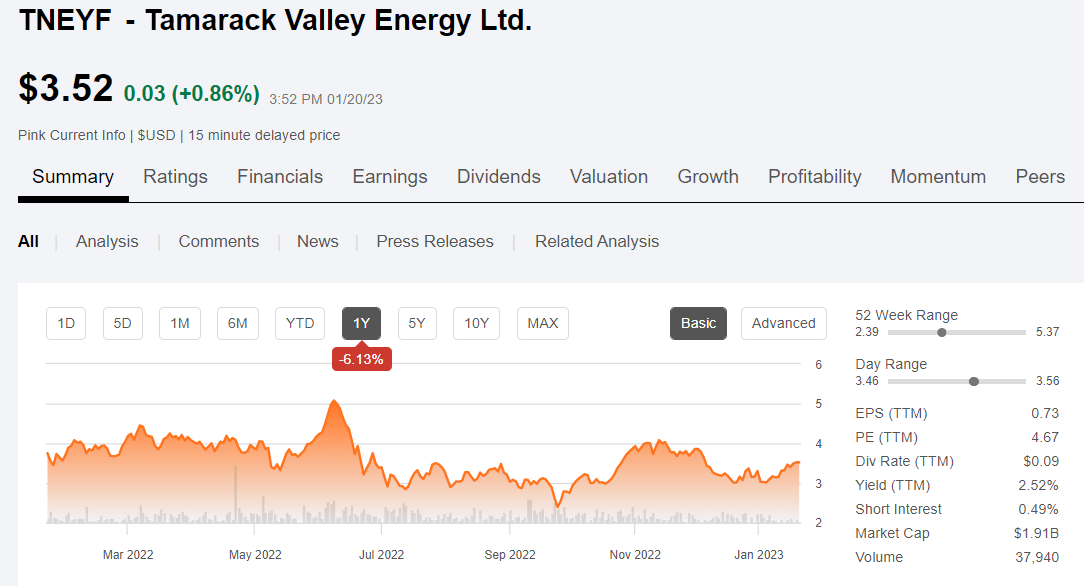

Tamarack Valley Energy (OTCPK:TNEYF) (TVE) is a leading player in the Charlie Lake and Marten Hills sections of the Alberta, Clearwater play. TVE has sold off 30% from mid-year 2022 highs, trading in a range of mostly between $3 and $4.00 since then. Currently at $3.52, it is selling on the mid-point of that range, at attractive multiples – EV/EBITDA, 4.8X and P/FB-$39K.

TVE price chart (Seeking Alpha)

We have discussed this company before, but not since the middle of last year. You might give that one a read as well if TVE interests you. We have also discussed the Clearwater many times, notably with Headwater Exploration, (OTCPK:CDDRF), a 2020 startup formed to develop the Clearwater exclusively. The Clearwater has been proclaimed the most economic play in North America, and that sort of chat-up always makes my ears perk up. Low costs bode well for long term survival as we have discussed on many occasions.

I think there is strong case to be made for TVE at current levels as a long term core position for growth and increasing shareholder returns. We will discuss as we close out this article.

The Thesis for Tamarack Valley Energy

The company has positioned itself as leading producer in two key Alberta plays, Charlie Lake and the Marten Hills area where the Clearwater is at its best. As a reminder, the key feature of the Clearwater is its high porosity – room for oil, and permeability – ability to flow. When you combine this with the viscosity of the oil obtained, it means the wells will produce without a frac or the steam injection that’s so common to many heavy oil producers. This saves literally millions of dollars per well, and drives down breakeven costs to where a substantial profit is realized even when WTI sells off and the WCS differential is out whack-as it is currently. TVE estimates these wells will return their cost 6-7X over the life of the well.

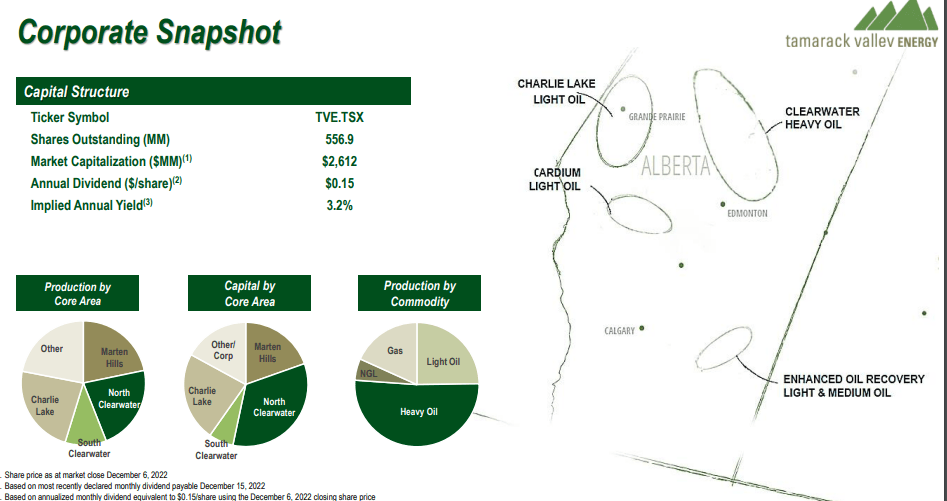

Corporate Snapshot (TVE)

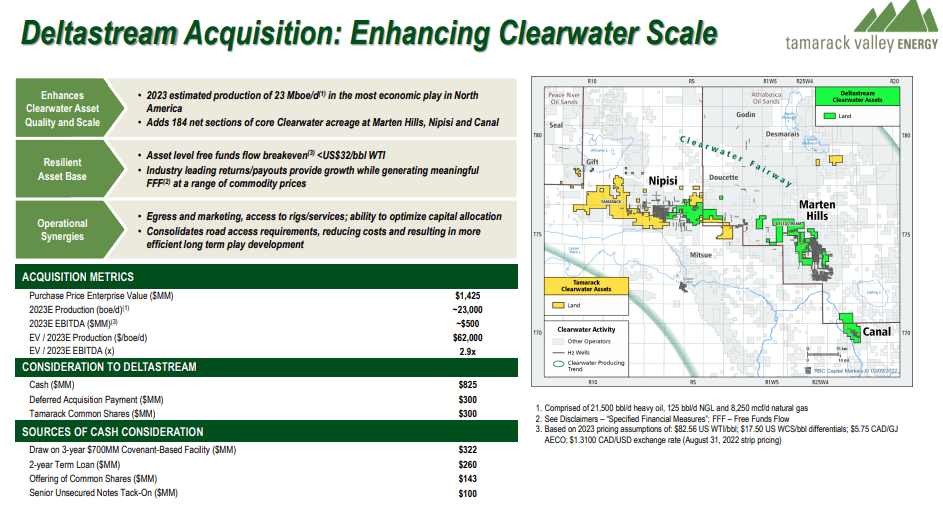

The just completed Deltastream deal was transformative for TVE. Linking together several discontinuous blocks TVE held prior, it enables cost savings-estimated at over $300K per well. Roads and a marketing terminal were cited in the linked call as being a benefit of Deltastream. The deal was also structured in a cash, stock and deferred payment that kept the $1.425 bn price of Deltastream from blowing up TVE’s balance sheet. In addition to blocking up TVE’s acreage position, Deltastream brought 23K BOEPD of production, making it immediately accretive to cash flow and EBITDA.

Deltastream deal (TVE)

What the Clearwater means to investors is a quick recovery of capital and multiple payouts during the initial recovery phase-first 5-years of production, with waterflooding in the secondary recovery phase. Lower capex and longer economic life means superior capital efficiencies as compared with a top tier Permian Wolfcamp-A well in the example shown in the slide below. (Although it should be noted some of the data in that slide is a little spongey, as I know of no one drilling 3,200′ laterals in the Wolfcamp). None the less, the larger point remains valid: Clearwater wells deliver longer life production at lower costs per foot.

The Clearwater advantage (TVE)

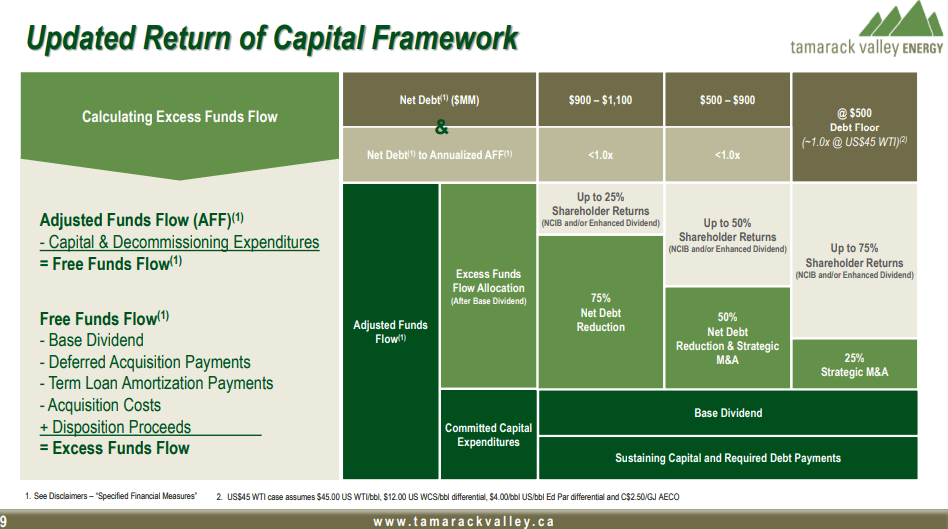

TVE has increased their dividend twice in the past year by significant percentages. The company is focused on debt reduction in the near term with plans to allocate 75% of AFF to shareholder returns once floor debt of $500 mm is achieved. That could be quite significant a few years hence.

Return of Capital framework (TVE)

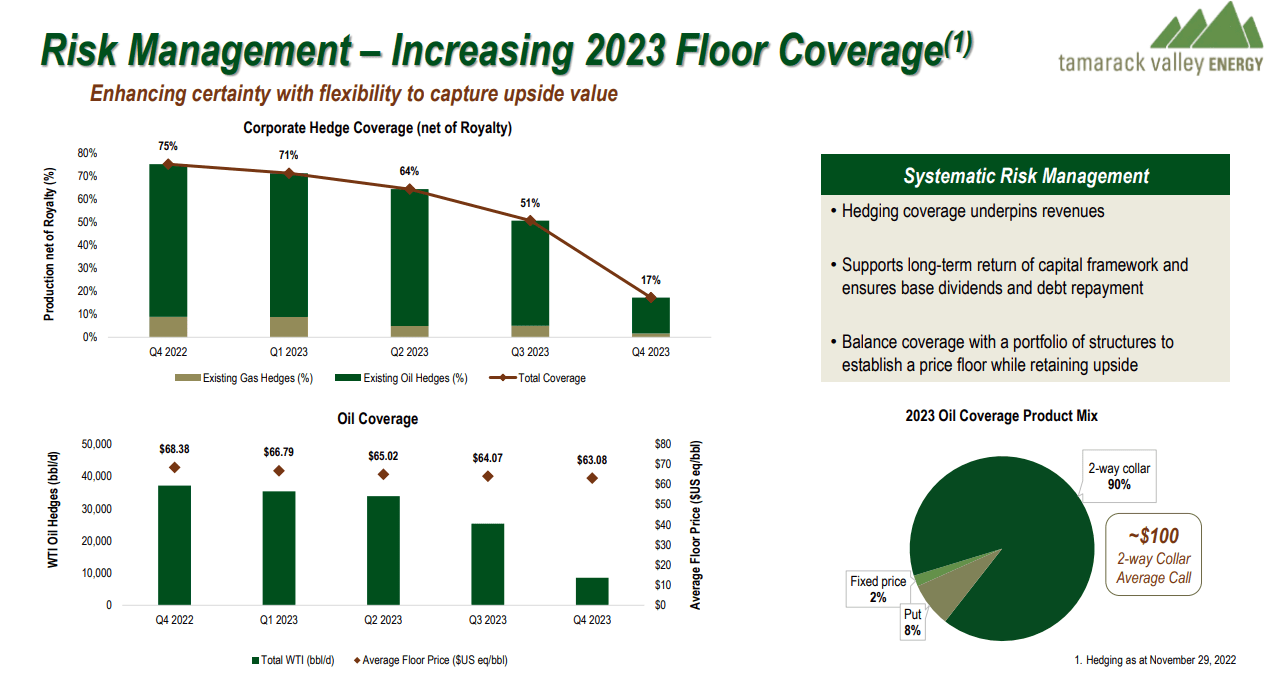

Hedging

About 60% of TVE’s liquids production is hedged on a 2-way collar at $100 oil for 2023. This puts in a floor price in mid-$60’s to protect downside risk. The percentage slides during the course of the year as debt is paid down, to expose more crude to market pricing. The company notes it may add additional hedging during the course of the year.

TVE hedges (TVE)

The Catalyst for TVE

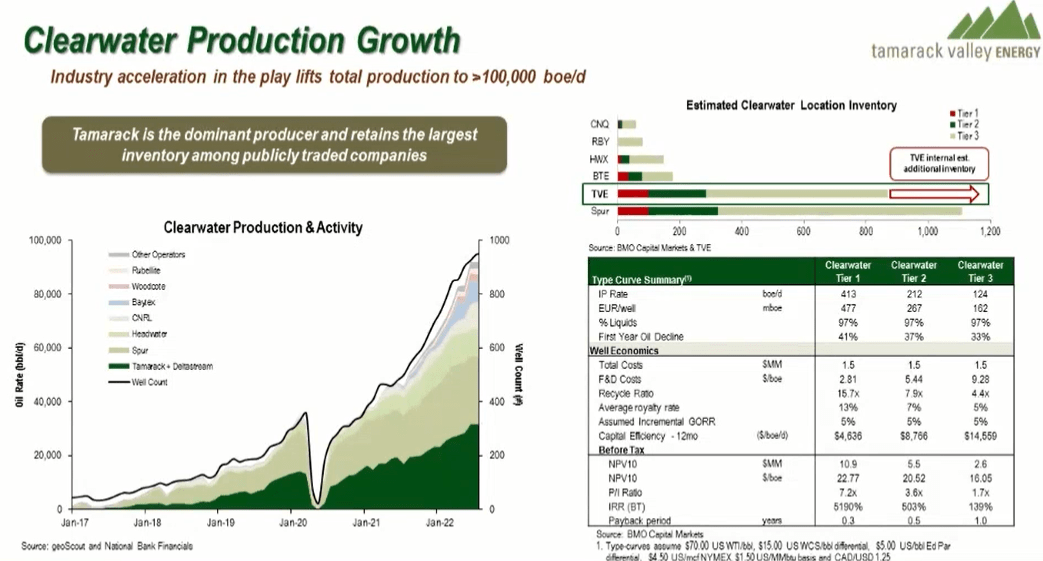

The growth potential in the Clearwater is the top catalyst for TVE. The company has derisked about 280 drill sites so far, and with its acreage footprint will add to those substantially.

Clearwater production growth (TVE)

The company has grown production to 43,476 organically, and the Deltastream added 23K to that figure. That rate of growth could take toward 80K BOEPD of production by 2023 exit.

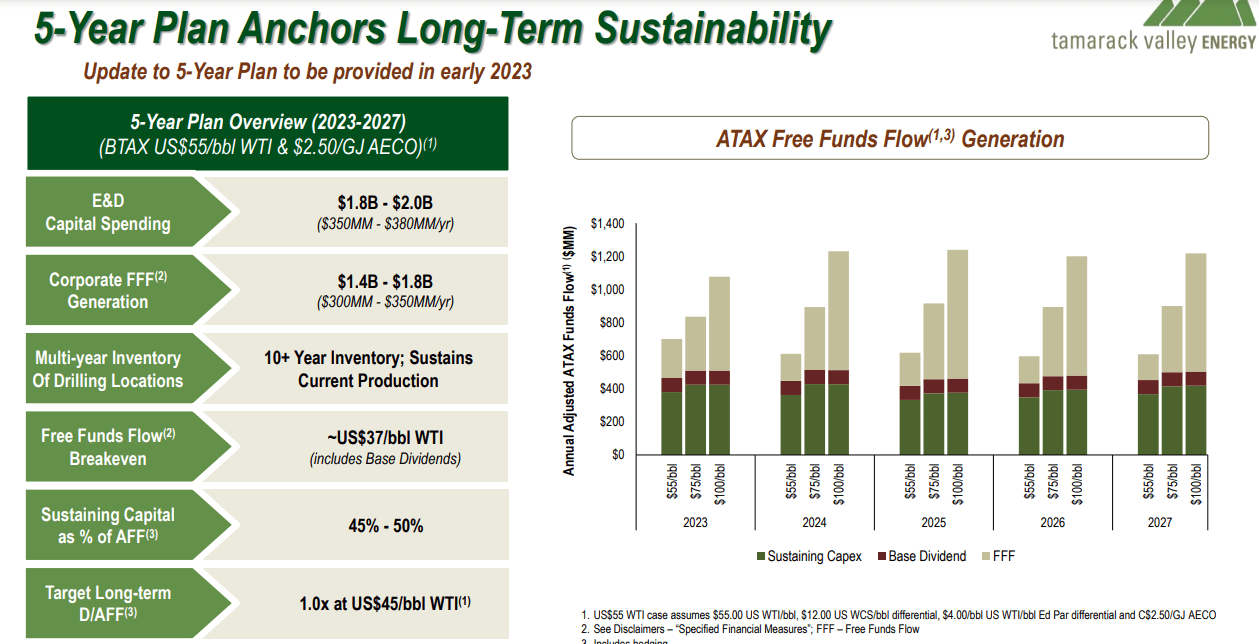

Long Term sustainability (TVE)

At $75 bbl WTI the slide above forecasts AFF of over $800 mm CAD this year. This provides ample room for additional dividends and share buybacks, while holding capex in the $400 mm range annually.

Q-3, 2022 and Guidance

TVE generated Q3/22 adjusted funds flow of $177.8 million. They achieved quarterly average production volumes of 43,476 boe/d in Q3/22. Free funds flow of $79.4 million. Net income ran to $124.8 million. This funded a dividend of $13.6 million and, in conjunction with the Deltastream acquisition, they announced an increase to the base dividend of 25% to $0.15 per common share annually ($0.0125 per month).

In Q-3, TVE repurchased 3.1 million common shares under the NCIB for $12.8 million during the quarter for a total of 4.4 million shares and $18.6 million in consideration year to date.

Capex ran to $93.5 million in exploration and development (E&D) capital expenditures and $4.7 million on undeveloped land in the Clearwater and Charlie Lake areas during Q3/22, which contributed to the drilling of twenty-three (23.0 net) Clearwater oil wells and six (5.4 net) Charlie Lake oil wells.

TVE exited the quarter with $286.8 million of net debt, and successfully closed the disposition of certain assets in the Viking CGU for gross consideration of $70 million ($59.5 million net).

Announced the acquisition of Deltastream during the quarter for total consideration of $1.425 billion CAD, consisting of 80.0 million shares of Tamarack, $300.0 million of deferred acquisition notes and $825.0 million in cash. The cash consideration was financed, in part, through a $100.0 million addon offering to the Company’s existing 7.25% senior unsecured sustainability linked Notes due May 2027 and a $137.3 million net equity financing – both of which closed in September 2022.

Guidance

Capex for Q-4, is forecast to run $125-$135 mm. Q4 Production will come to 62,000-64,000. Expenses: Royalty Rate 20-22% Operating $9.50-$10.00 Transportation $2.50-$3.00 General and Administrative $1.25-$1.35.

Risks to our Thesis

I view these as mostly political and takeaway. On the political side, both Canada and the U.S. are throwing up roadblocks to petroleum development. It could get worse and is just part of our calculus investing in this space.

The Trans Mountain Expansion is desperately needed not too far in the future for access to the BC market. Completion date on their site is late 2023, but full permitting is pending. Refer to comment above for further guidance.

Your Takeaway

TVE is aggressively developing key focus areas for 2023 with its capital budget. 39 new wells and 4 injector conversions are planned for Marten hills, with IP-30’s of 250 BOPD. At Nipisi 13 new producers and 29 injectors to kick off a waterflood will be drilled. West Marten Hills will get 28 new wells, with half to accommodate the water flood. Southern Clearwater will receive 11 net wells. Charlie Lake will get 19 new producers with an average IP-30 of about 600 BOPD. At $75 WTI, these wells repay their $5 mm cost to drill in about 4 months and forecast to deliver another 2 payouts over the next five years.

Loose math suggests if we take the ~85 new wells TVE will bring on this year at 300 BOPD-fairly conservative, and apply a 20% decline to existing production, they should exit 2023 at about 75K BOPD. That’s a rate that resembles what they have done YoY, so it’s not too far-fetched.

With netbacks in the $40 range, that’s an additional $125 mm per year and takes them easily past that $800 mm CAD figure forecast for 2023. To keep the multiple at 4.9X, the stock price needs to adjust to $5.50ish per share-USD, implying a 63% upside from present levels. Not too shabby. As long as we are having fun with numbers, let’s say they do this again in 2024. That gets you to a share price in the mid-$7s to $8.00 USD in a couple of years.

A couple of outliers that could impact positively are. Higher WTI prices and higher production than what I’ve estimated from new wells. When I am playing with numbers, I like to keep it on the conservative side!

Bottomline on this one. I wouldn’t sit on the fence too long.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment