Mario Tama

We’ve been following Take-Two Interactive (NASDAQ:TTWO) and have both bought and sold shares over the past 12-months. We generally hold a bullish view on the company, as we expect future game titles and longevity of game franchise translates to investment returns. Recent headline estimates missed consensus expectations, but we anticipate the stock to trend higher as we move further into the year. We provide conservative estimates to FY ’23 – FY ’25 results, and still have margin of safety when discussing upside in our investment thesis on TTWO stock.

Take-Two Interactive earnings call had some major pain points, which we try to talk about constructively in our reactionary research report. Some key points at a high level: 1) Costs tied to the Zynga transaction ($12.7 billion) are likely to take longer to work through and will impact profitability metrics. 2) The amount of cost tied to mobile game development hinges on being able to develop native video game titles. 3) Expect some near-term charge offs tied to the Zynga transaction. 4) Cost reductions of about $50 million annually on operating expenses, mainly in the form of selling general and administrative expenses, as opposed to laying off in-house game developers.

We anticipate that given the launch of additional mobile game titles, and the announcement of next-generation game franchises the narrative improves, but not immediately. This is why TTWO was down -4% in the after-hours on Monday session trade on February, 6th 2023. The stock then rallied to $111 over the course of the same week (ending February 10th, 2023), recapturing much of the selling following the announcement of earnings. The stock ultimately trades at the same level as it did prior to the earnings announcement signaling some confusion among traders and investors in the stock.

Management a bit more limited on discussion tied to next-generation console platforms like PlayStation 5 or Xbox Series X until summer with discussion stemming heavily on monetization from pre-existing game titles that have been released. We do like the fact that they can continue to monetize GTA V, but it’s worth noting that the franchise has aged over the years thus diminishing the amount of revenue contribution from core Rock Star game franchises. The inclusion of Take-Two’s NBA2K23 being the only product with an annual refresh cadence (hence the revenue contribution skewing towards the sports title). Further dependence on monetization of mobile devices makes us a little concerned about the growth headwinds given the overall weakness this far into the game console cycle.

Management noted that the company would have another update on game release and game slate in May 2023. Hopefully expectations are diminished with the launch of Grand Theft Auto 6. Absent the inclusion of hype tied to the next-generational release of Grand Theft Auto 6 the earnings call tried to make best of GTA V and GTA Online related sales and shipments. The game was originally released in 2013 and continues to have its life extended with the addition of DLCs and online content.

We rate TTWO at Buy with a $130 price target, and anticipate +17% upside from the time of writing, as we value the stock at 22.5x FY ‘25 earnings. The stock looks undervalued given the prospects for improving game console cycle, weakness in holiday sales, and low expectations on game release slate. We anticipate that the company will generate quicker growth rates as we exit the transitional year. We value the stock conservatively. We anticipate less revenue and diluted EPS when compared to other analysts in our FY ’25 estimates to arrive at our price estimate embedding more conservatism in our model.

Take-Two game console cycle lows shock shareholders

We’re not surprised management missed its own financial guidance as results were fairly weak for hardware, and hardware related shipments for game consoles. This was mostly owed to the fact that chip shortages, scalpers buying consoles on the primary and secondary markets, and the pandemic all played a role in keeping the PlayStation 5 and Xbox Series X out of the hands of consumers.

We think these trends start to subside as we enter into 2023 as the chip shortage is turning into a chip glut, as we see a surplus of memory in the channel, which is indicative that with the exception of some categories like next-gen smartphones like iPhone 15, 15 Pro which use next-gen processes the aging tech inside of the current 7nm console generation should be able to take advantage of added capacity once the smartphone cycle transitions towards 5nm and 3nm manufacturing.

Hence, we expect all the accompanying components like memory, storage, processors and graphics inclusive of wireless modem will be in abundant capacity as console’s primary competitor for parts, high-end desktop GPUs and smartphones start to transition towards 5nm and even 3nm orders over at TSMC. Upcoming AMD Zen Core 4 architecture shifts more MPUs (microprocessor units) to TSMC’s (TSM) 5nm+ second-gen process (AMD Socket AM5). The utilization for 7nm manufacturing has come down considerably signaling the beginning of a massive volume ramp-up for current gen consoles. We anticipate both the initial and second-gen 5nm processes to shift meaningful amounts of production away from older gen 7nm manufacturing. Hence, game consoles will start taking the remaining capacity leading to supply/demand balance and retail pricing of $499 for PlayStation 5 and Xbox Series X.

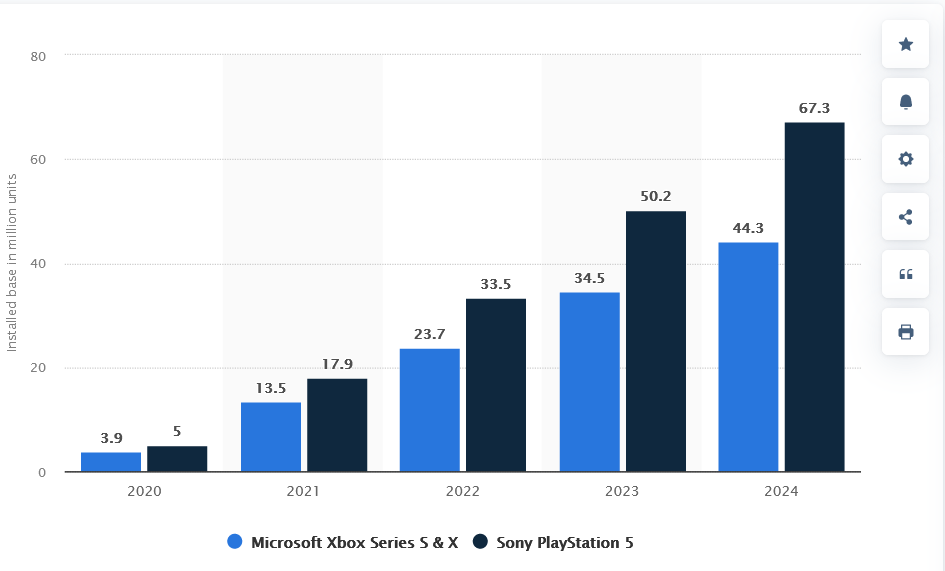

Figure 1. Game Console Installed Base

Game Console Shipment Estimate (Statista)

We’re at a point where Xbox Series S & X shipments, and PlayStation 5 shipments total 57.2 million units, which is quite low at this point in the cycle (3rd holiday launch year). Typically games get more exciting at this point in the console hardware cycle (at least that’s the hoped for outcome). We think the number of available next-gen installed base plays a huge factor in the timing of release for key game titles.

Furthermore, we expect the company’s launch of certain titles to sustain financial results like NBA 2K24 to play a major role in reducing some uncertainty tied to financial results given the annual release cadence of sports titles. Without the accompanying addition of a core game title in the line-up for the upcoming year, investors might have to hit the panic button.

That being said, we’re early in the game console cycle, and we anticipate that as the gamer base builds up, and AAA titles launch from TTWO we can get a bit more optimistic on financial results. We’re probably off by 3-months or so before we can build any real excitement in the stock.

TTWO earnings summary headline numbers and guidance

Take-Two Interactive reported Q3 GAAP EPS of -$0.91 and missed consensus expectation by $.07, as consensus estimates implies GAAP EPS of -$0.84 for Q3 ‘23 results. The company also reported revenue of $1.41 billion (which grew by 56.1% year-over-year) but mostly driven by acquisition related impact tied to Zynga. TTWO missed consensus expectations by $40 million, as analysts were expecting the company to report $1.37 billion sales.

We could imagine TTWO improving on financial results, but given the cost of launching various mobile and game console titles we’re not exactly certain when the company will transition back towards profitability given the addition of acquisition related impact, and the skew towards AAA game title launches having substantial revenue impact on holiday quarter sales.

We hope there’s more hiding for the upcoming Winter launch of 2023, but we’re not exactly certain what’s in store for the game developer by end of 2023. This limits most of our optimism towards what management guidance suggests for the full-year, which seems limited to another quarter or Q4 results, which are reported sometime in May of 2023 (approximate). We anticipate that TTWO will have some time to build-up some momentum in shareholder narrative for the beginning of its next fiscal year following the E3 gaming conference (June 2023) where game industry analysts, experts, and video gamers convene together to play games and discuss the launch of future game titles.

In Q3’ 23, TTWO reported that digital sales mix for consoles increased from 63% to 69% y/y and that the bookings mix for game segments were as follows: 46% Zynga, 36% 2K, 17% Rockstar Games, 1% Private Division labeled games. We anticipate that the increased mix towards mobile might be a bit difficult to stomach, but with the launch of other Rockstar titles at some point in the future and also 2K titles we anticipate that the mix contribution will vary, but commentary on release seems to suggest that much of the momentum near-term is in mobile gaming unless game console releases and game console shipment starts to reach parity with consumer demand.

Furthermore, the company reported outlook for the full fiscal year 2023, whereby revenue outlook was $5.24 billion – $5.29 billion and total opex range was $3.4 billion to $3.41 billion (which ends in March but gets reported in May or June depending on when TTWO announces its earnings date). The management team communicated that operating expense reductions could exceed $50 million per year, but expectations of a mass layoff should be limited given the differences in the game publishing industry versus big tech. Furthermore, the company will report a GAAP net loss range of -$704 million to -721 million, or -$4.40 to -$4.50 dil. earnings per share.

David Karnovsky, an analyst at JPMorgan, mentioned that holiday spending trends were particularly weak for video game publishers in-line with other game publisher commentary:

Messaging from TTWO was similar to EA and UBI, with management commenting that consumers – especially over the holiday period – were more discerning with their spending, shifting allocations to the largest franchises and discounted catalog, and away from smaller and in some cases critically acclaimed new releases (e.g. Marvel’s Midnight Suns, which launched in the post Black Friday discount window). Incrementally, some of this softness extended to RCS for core PC/console games, even amid continued strong engagement.

The weakness in holiday game title shipments mirrored much of the negativity echoed by big tech companies last week. We anticipate that the added pessimism coming from this quarter further echoes the sentiment that Hollywood has been doomed lately, especially on the creative output side of things. However, we hope to paint a bit of a better picture by discussing our financial model and how we arrive at our recommendation and price target on Take-Two Interactive.

Take-Two Financial Model Discussion and Overview

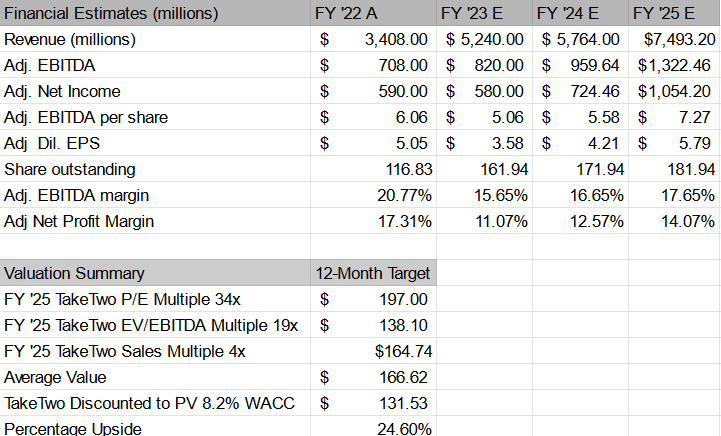

Figure 2. Take-Two Financial Model

Take-Two Interactive Financial Model (Trade Theory)

We anticipate that the company will mostly report in-line with the commentary indicated in the earnings call, perhaps at the low-end of the guidance range.

We forecast revenue of $5.24 billion and non-GAAP diluted EPS of $3.58 for FY ‘23, which compares to consensus estimates of $5.22 billion and non-GAAP diluted EPS of $3.56. Given the commentary tied to expense reduction probably not a whole lot of surprises there, and if anything, the addition of some operating expense reduction mostly presumes cost synergies tied to an acquisition, which rarely ever happens. We anticipate a ramping narrative tied to new game releases, and the eventual release of AAA title games for the present game console cycle to take our estimates higher.

Given the somewhat limited visibility of revenue, and non-GAAP diluted EPS earnings, we estimate +10% revenue growth for FY ‘24, and +30% revenue growth for FY ‘25. We anticipate the release of new game titles for consoles, and the mass release of a number of mobile games in the pipeline to drive a combination of sales and earnings growth. Analysts expect a massive sales increase of +40% to +60% by FY ’25 tied to a major game release, but we keep our estimates a bit more conservative given the absence of timing for a major game release.

Furthermore, we value the stock using a combination of 34x P/E, 19x EV/EBITDA, 4x Sales to arrive at an average FY ‘25 value of $166 and then discounted to PV using the firm’s WACC of 8.2% to arrive at our $130 price target for the next 12-months. We anticipate the stock to have +17% upside from present levels following the weak earnings results as expectations have reset to a point where any announcement made about future game releases would actually move the needle.

Take-Two Interactive a quick recap on investment thesis

Weakness in near-term results paints somewhat of a difficult cloud over the next couple quarters. We anticipate announcements at the upcoming E3 gaming conference to help with the transition of core game franchises and thus reassert a more positive shareholder narrative to keep bulls onboard. Also expect limited successes with transitioning console games to mobile titles. The most successful mobile games tend to be designed for mobile, and are mobile only franchises.

We think TTWO appeals to more value oriented investors who prefer to buy stocks on poor reactionary outcomes tied to quarterly earnings results. The weakness tied to financial outlook seems a bit blown out of proportion, but absent any meaningful dialogue around game title release we think some prefer to be on the sidelines.

We anticipate that the broader economy sort of adjusts to the new reality of higher inflation, and that sentiment will start to improve as we move into summer of 2023. Furthermore, TTWO likely recovers by June as the stock is expected to announce a number of new games at E3 2023, and we think it’s a make or break year for game publishers as the release of new games is the only pressure reliever for what has been a rough Q4’22 for game sales.

We recommend TTWO at Buy, to our readers because it’s heavily undervalued and because we anticipate +17% upside to the stock given the conservative inputs of our model when compared to other estimates from other analysts that cover the stock. We think the stock could reach $130, which is conservative and far below its peak at $200 from February of 2021, so the transitional narrative might appeal to value investors who can keep up with the stock.

Be the first to comment