bunhill

T. Rowe Price Group, Inc. (NASDAQ:TROW) delivered its FQ4’22 and FY22 results last week. It was considered a mixed bag as the leading asset manager outperformed consensus estimates on adjusted EPS for Q4 but underperformed Q3’s metrics.

As such, investors will need to parse whether global equity and fixed-income markets could continue to improve in 2023 following a remarkable January recovery.

While TROW posted a 5% QoQ drop in Investment Advisory revenue in Q4 (which accounted for 90% of net revenues), it posted an improvement in AUM metrics. Accordingly, TROW delivered a 3.3% QoQ increase in ending AUM in Q4, lifted significantly by “market appreciation,” despite experiencing net cash outflows of $17.1B. As a result, TROW delivered a net cash outflow of nearly $62B in FY22 as the equity bear market hammered investors.

However, management is sanguine about its 2023 outlook, bolstered by the strength in “core and value-oriented equity and some fixed-income products. In addition, while management highlighted the underperformance in growth-oriented strategies, we believe the market’s risk-on sentiments have lifted headwinds against growth and tech stocks.

Still, market sentiments remain pessimistic despite the recent recovery, as investors fear a worse fallout from a potential recession has not been reflected. Moreover, the Fed could stun the bond and equity bulls at its upcoming FOMC meeting, even as investors bet on an earlier-than-expected Fed pivot.

As such, Fed Chair Jerome Powell & team are likely still TROW’s most formidable challenge, which could impact investors’ sentiments further if the Fed doesn’t intend to loosen financial conditions further in 2023.

As such, paying close attention to the tech-focused NASDAQ (NDX) (QQQ) could proffer vital clues on whether the risk-on sentiments could continue.

Why? The 10Y average P/E of the Tech sector is 25.2x, well above the S&P 500’s (SPX) (SPY) 17.7x. Also, the NASDAQ has outperformed the SPX over the past ten years. As such, if risk-on is indeed returning in earnest, we believe the well-battered tech and growth-focused NASDAQ will likely be a critical beneficiary.

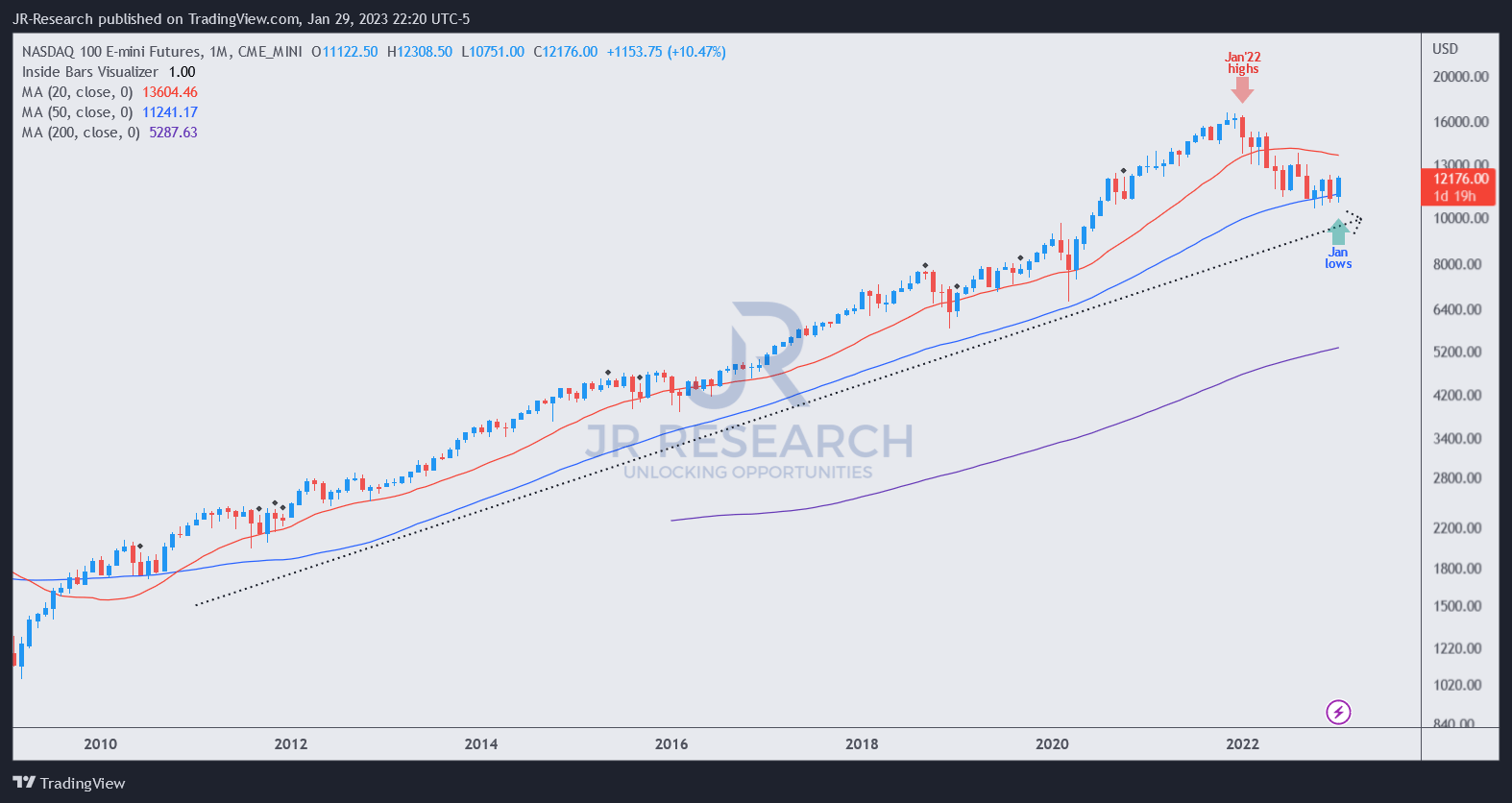

NASDAQ futures price chart (monthly) (TradingView)

As seen in the NASDAQ’s long-term price chart, it’s still in a long-term uptrend, with last year’s “collapse” a mere pullback observed above.

We also noted uptrend continuation price action at its October lows, suggesting investors have primed for a return to growth and tech stocks over the past three months.

As such, it augurs well for TROW moving ahead, as Wall Street analysts (Neutral rating) don’t expect the asset manager to post robust performance in 2023.

Accordingly, TROW is projected to post a net revenue decline of 3.9% in 2023. It’s also estimated to deliver an adjusted EPS decrease of 16.5% after FY22’s 37.1% decline.

Therefore, we assessed that analysts don’t expect TROW’s operating performance to recover in 2023, likely anticipating further downside risks related to the economy and the Fed.

As such, we believe investors must consider whether they are in the mild recession camp or the steep recession camp before adding further exposure to TROW.

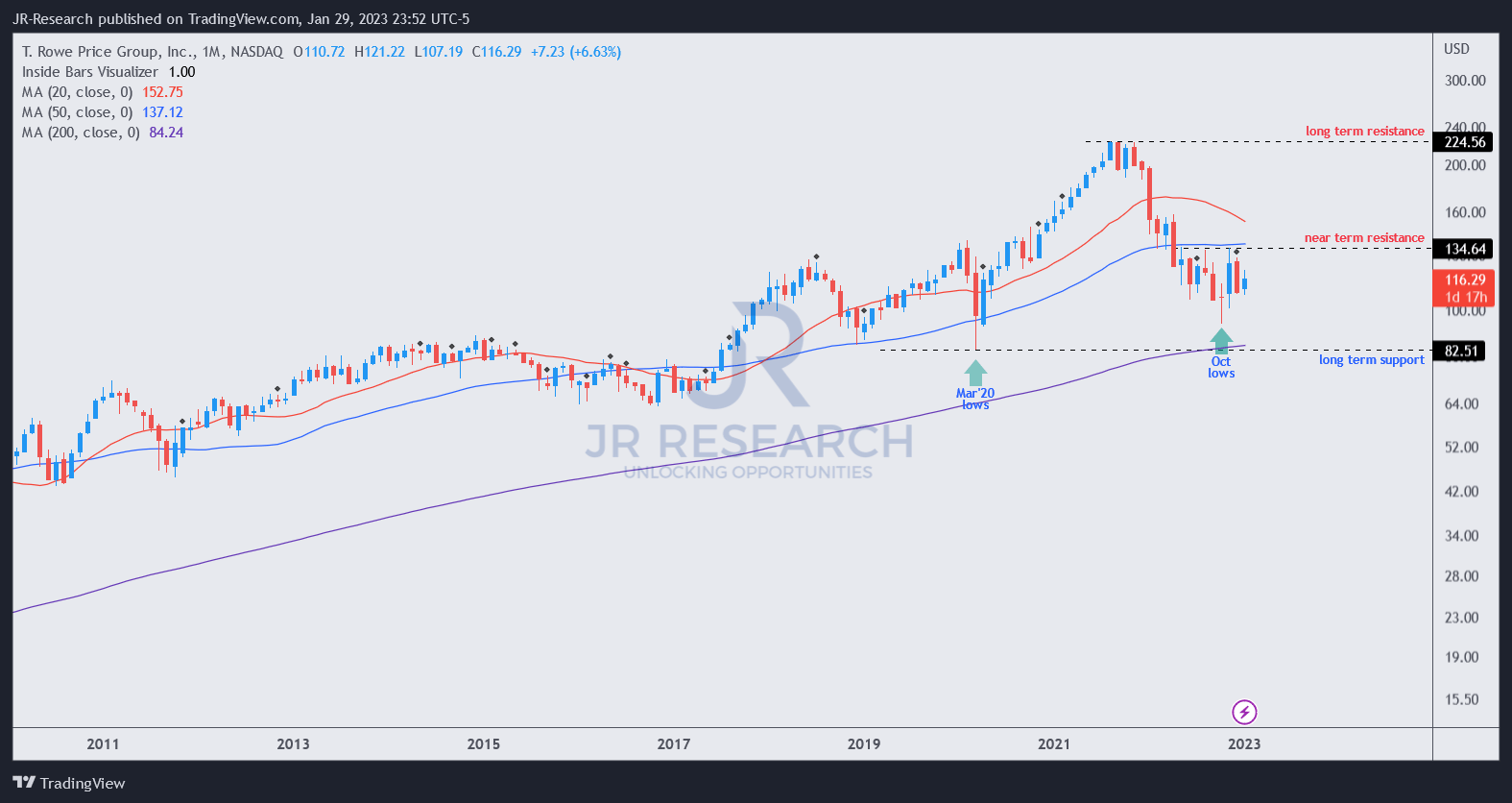

TROW price chart (monthly) (TradingView)

Despite the doom and gloom, TROW is still in a long-term uptrend, as seen above.

TROW’s October lows are still holding up constructively, vital for the recovery above its 50-month moving average or MA (blue line).

Hence, investors picking TROW’s current levels need to be convinced that the asset manager can continue outperforming in the long term.

TROW updated its investment performance for FY22, showing that 73% of its US equity mutual funds outperformed Morningstar’s median over the past ten years. In addition, its multi-asset strategy saw a 90% outperformance against its median over the same period.

However, its 1Y performance has been somewhat disappointing, as only 53% of its US equity mutual funds outperformed its median.

Therefore, if investors are convinced that its near-term and long-term performance could normalize, picking the pessimism in TROW could be worth the reward/risk.

Rating: Buy (Reiterated).

Be the first to comment