Avatar_023

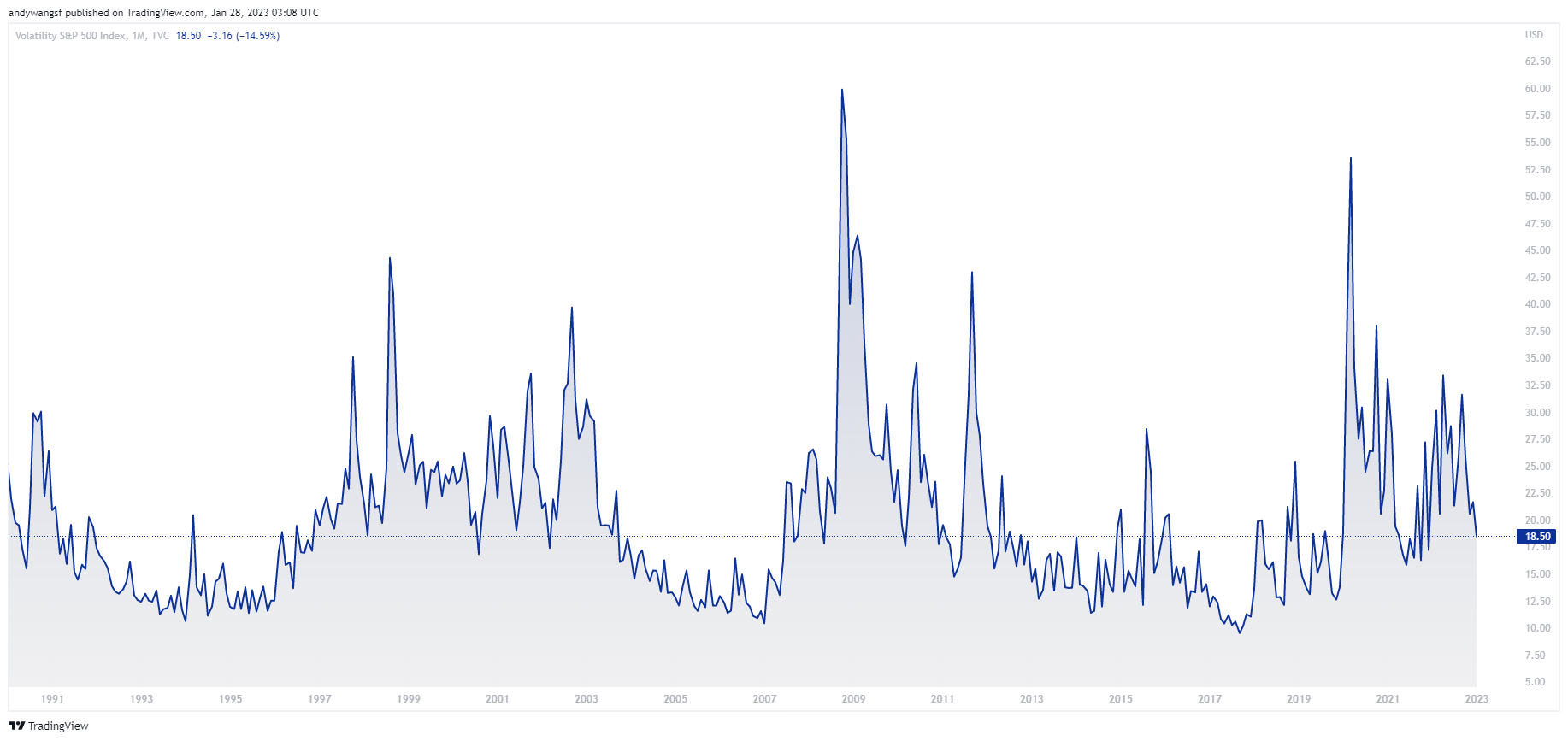

The Cboe Volatility Index (VIX) is once again approaching levels that are attracting the attention of traders who are hoping to bet on some kind of major risk-off event in the equity markets. On the other hand, traders who have been betting on calmer markets over the past several weeks would be sitting on impressive gains, with the VIX having fallen from its 12 October peak of 33.5 points to 18.5 points at the time of writing.

In this article, we will first begin by assessing the risk-reward for both the long and short sides of trading the VIX. We shall then discuss why we think the short side could be headed for trouble.

TradingView.com

For traders with a long bias, trading the VIX is pretty straightforward. The VIX has a well-established history of experiencing recurring spikes that have delivered abnormally large returns at magnitudes that far exceed even some of the most volatile commodities. One popular strategy to trade the VIX involves building long positions on the VIX right before earnings season, FOMC meetings, or key economic data releases.

Summarising definitions by the Cboe, the VIX Index is a benchmark designed to provide an up-to-the-minute market estimate of the implied volatility of the S&P 500 Index. The VIX is calculated by using the midpoint of real-time S&P 500 Index (SPX) option bid/ask quotes. More specifically, the VIX Index is intended to provide an instantaneous measure of how much the market thinks the S&P 500 Index will fluctuate in the 30 days from the time of each tick of the VIX Index.

Because equity market meltdowns tend to result in sudden spikes in implied volatility on SPX options as hedge funds and institutional fund managers scramble to hedge their portfolios by buying put options, the VIX is more likely to spike than to collapse following a relatively stable market. This is mainly a result of human nature, where traders tend to be more aggressive at selling risky assets than when buying them. In other words, investors can afford to wait when buying a stock, but when it is time to dump one, they all rush for the exit.

Having said that, trying to guess when the next piece of bad news will hit the markets is as difficult as trying to guess when a particular number will eventually come up on the roulette wheel. Indeed, there have been extended periods of time when the VIX just drifted lower for months without a spike.

But even if traders with a long bias on the VIX don’t get the timing exactly right, the downside risks can be managed by going long only when the VIX is at an extreme low.

Shorting The VIX Is Becoming A Dangerous Game

Now, we turn our discussion towards strategies that are aimed at shorting the VIX.

The ProShares Short VIX Short-Term Futures ETF (BATS:SVXY) is a popular tool for expressing a short view on the VIX. The SVXY provides traders with one-half the inverse exposure to the S&P 500 VIX Short-Term Futures Index, which measures the returns of a portfolio of monthly VIX futures contracts with a weighted average of one month to expiration.

Short VIX strategies typically involve shorting the VIX following a large spike in anticipation that implied volatility has overshot and should quickly reverse once markets settle down. But such strategies are also subjected to the risk of the VIX spiking even higher before it eventually reverses. Because of the sheer magnitude of VIX spikes, most traders are unable to stomach the massive losses associated with underestimating the VIX’s upside.

The alternative is to take a more passive approach, by trying to catch the VIX’s natural downward drift over time. This usually means trying to avoid shorting the VIX right at its peak but aiming for the middle part of the downward trend back to more normal levels of implied volatility.

For traders who prefer to take the short side of the trade, however, the risk-reward is a lot more trickier. The act of shorting the VIX resembles that of “picking up pennies in front of a steamroller”, a metaphor coined by Nassim Taleb to describe making small gains repeatedly at the risk of suffering an irreparable loss.

Not A Good Time For SVXY

Back in November 2022, we published an article titled “VIXY And SVXY: Exploring Strategies To Profit From Fear” where we provided a historical study of the VIX’s behaviour and explored a systematic strategy to trade the index. We also set specific target levels to go long or short the VIX, at 15 points and 40 points respectively.

With the VIX currently trading at 18.5 points at the time of writing, the risk-reward of holding onto the SVXY has become increasingly unfavourable. Not only are potential returns on SVXY limited to just 9 points on the VIX based on the historical all-time low of 9.14 points (1990 – present), but potential losses could be as large as 38 points based on the average of the 5 highest peaks of 57 points.

Recall that major events such as earning seasons, FOMC meetings, and key economic data releases, are potential windows for volatility spikes. With the FOMC concluding its meeting on February 1, January CPI data due on February 14, and the SPX having enjoyed a forceful rally since the beginning of the year, we think the odds are heavily stacked against SVXY in the immediate term.

Watch Out For Our Entry Level On VIXY

To be absolutely clear, although we dislike the odds of shorting the VIX at this moment, it does not mean that we are recommending traders take a long position on the VIX either.

As we have discussed in much greater detail in our previous article, we are targeting an optimal entry level of 15 points for the VIX to take a long position through the ProShares VIX Short-Term Futures ETF (VIXY).

With the VIX hovering at just 3.5 points above our entry level of 15 points, do stay tuned for our next article on the VIXY.

Be the first to comment