gorodenkoff

I initiated Stryker (NYSE:SYK) in August 2023, and pointed out that Mako would continue to be a growth driver for the company. They reported a strong Q3 FY23 result and provided an initial FY24 guidance with 10%+ organic revenue growth. The Mako shoulder and spine applications are on track, and I think they are going to become a major catalyst for their stock price in 2024. I maintain my ‘Buy’ rating with a fair value of $320 per share.

Quarterly Review and FY24 Outlook

They delivered 9.2% organic revenue growth and 16% adjusted EPS growth year over year during Q3 FY23. The growth is evident across their business segments, with 10.1% organic revenue growth in MedSurg and Neurotechnology and 8% in the Orthopedics and Spine segment.

SYK quarterly earnings

They ended the third quarter with $1.9 billion in cash and equivalents and $12.7 billion in debts. They paid down $100 million of debts in Q3 FY23 and are on the right track to deleverage their balance sheet.

In terms of cash flow, they generated $2.2 billion in cash from operations year-to-date, reflecting a 34.7% growth compared to YTD FY22. This robust cash growth is driven by earnings growth and accounts receivable improvements.

For FY23, they guided for 10%-10.5% organic revenue growth and adjusted EPS in the range of $10.35 to $10.45. Considering their strong growth year-to-date, I believe they can probably deliver the high-end of their full-year guidance.

During the earnings call, they also indicated an initial guidance of 10%+ organic revenue growth for FY24. I find this guidance to be quite reasonable. As they pointed out, hospital staffing issues are gradually improving globally, and Stryker is benefiting from supply chain improvements over time. More importantly, the patient backlog is expected to support elevated orthopedic procedural demand through 2024.

While hips and knee replacement surgeries can be postponed for a certain period of time, patients cannot defer these surgeries for too long due to enduring long-term pains. As such, I anticipate this backlog will be translated into Stryker’s revenue in FY24, and I am quite confident that they are going to issue a fairly strong guidance for FY24 in the next quarter’s earnings.

Mako Shoulder and Spine Launches

Mako is expanding its platform into the shoulder and spine end-markets, and this expansion is crucial for Stryker’s future growth. Mako has a significant installed base across hospitals, with many surgeons performing robot-assisted surgeries for hip and knee replacements. This installed base enables Stryker to generate additional revenue streams by adding shoulder and spine capabilities to the Mako platform.

During the call, their management indicated that the Mako shoulder and spine developments are progressing on track. They expect the spine launch in the middle of 2024 and the shoulder launch at the end of 2024. Regarding the adoption curve, they mentioned that a fast ramp-up should be expected for their spine applications, given a couple of players already in the market. For their shoulder application, a slower ramp-up is anticipated as it is the first-time application, and bone preparation is also complicated.

I consider the Mako shoulder and spine launches as crucial catalysts for their stock price in 2024 and 2025. While the initial launch in 2024 may not generate tremendous revenue, the adoption of these applications is vital for their long-term success. Mako has been highly successful in hips and knees, and Stryker enjoys the first-move advantage. The adoption of shoulder and spine applications on the Mako platform can help Stryker leverage its massive installed base and increase monetization from existing customers. Additionally, these new applications have the potential to expand their market reach across hospitals globally.

Model Update

The model assumes 10.5% organic revenue growth in FY23 and 10% in FY24, in line with their guidance. The revenue growth assumption for FY23 also includes 1.7% growth from acquisitions and -0.6% from foreign exchange. For normalized revenue growth, we forecast 9% organic growth and 2.9% acquisition growth based on their historical averages.

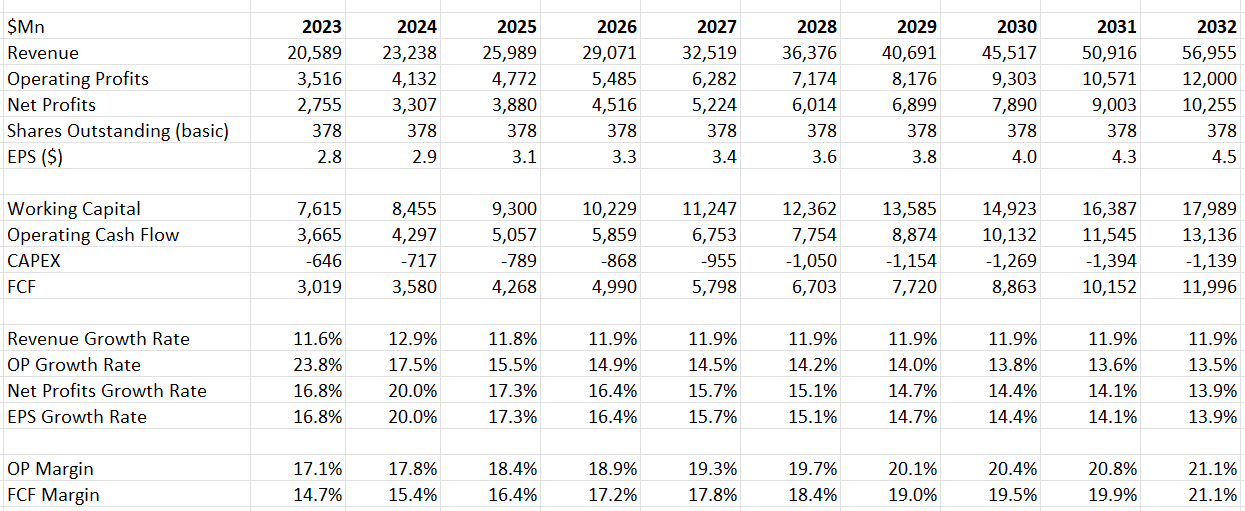

SYK DCF

Their operating margin expansion is primarily driven by operating leverage, with double-digit top-line growth and mid-single-digit expense growth. The model employs a 10% discount rate, 4% terminal growth, and a 14% tax rate, resulting in a calculated fair value of $320 per share.

Near-term Risks

Other than the main risks I discussed in my introductory article, investors should be aware of Stryker’s upcoming Q4 results, as the company is expected to face a strong year-over-year comparison. Stryker’s organic revenue grew by 13.2% in Q4 FY22, making it a challenging comparison. However, I believe everything has already been factored into their guidance.

Additionally, China’s entire healthcare industry is relatively weak in the post-COVID times, as the local government grapples with healthcare funding issues and has allocated a significant portion of the budget to COVID testing during the pandemic. The good news is that China only represents 2% of the total revenue, so the impact would be relatively small.

Conclusion

I believe the Mako shoulder and spine launches in 2024 will be notable catalysts for their stock price. Stryker is truly a growth compounder in the medical device industry. I reiterate a ‘Buy’ rating with a fair value of $320 per share.

Be the first to comment