Gilnature/iStock via Getty Images

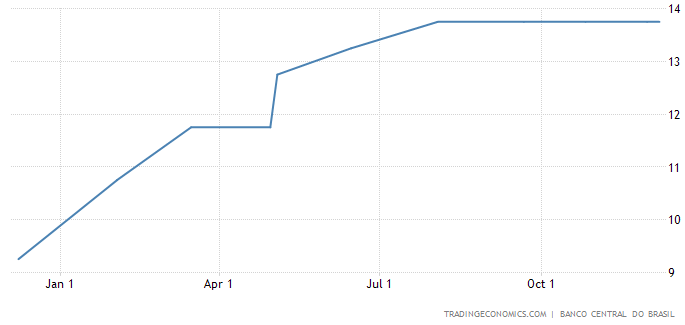

2022 proved to be a challenging year for many stocks, especially in emerging markets, and StoneCo (NASDAQ:STNE) was no exception. With the Brazilian economy feeling the impacts of a broader macro slowdown, the central bank aggressively rose interest rates to 13.75% to an effort to fight high inflation and normalize their economy.

While STNE remains one of the leading fintech companies in Brazil, the macro challenges have caused many investors to remain on the sidelines until macro visibility improves. The company has reported good financial results in recent quarters; however, the focus continues to be on how the macro environment reacts in the coming quarters. In my scenario outlined below, I believe it’s possible EPS could reach $1 by 2024, which could result in a $16 stock, assuming the valuation multiple remains flat. Even if the $1 EPS target were to be pushed out until 2025, a $16 stock by the end of 2024 would still yield a near-30% CAGR over the next two years.

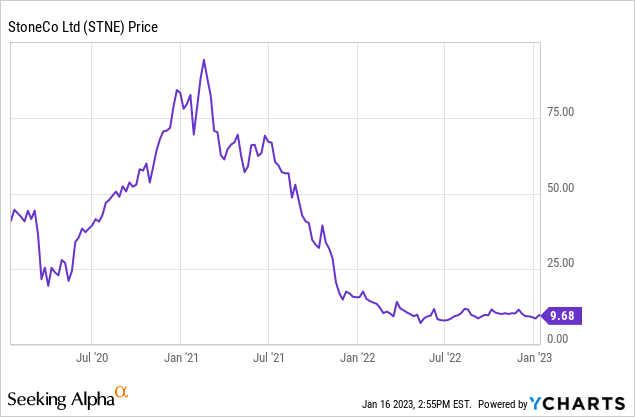

The stock remains significantly below its all-time high of $90+ and while I am not advocating for a return anywhere close to those levels, I do believe long-term investors will be rewarded with the stock currently <$10.

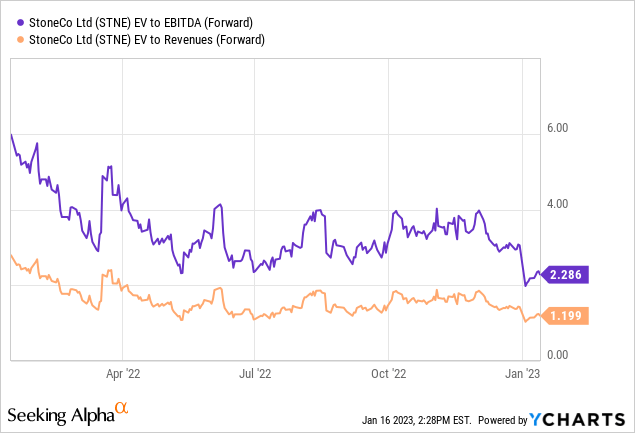

STNE currently trades ~16x 2023 EPS, which seems to appropriately take into consideration a volatile Brazil macro environment. Assuming STNE continues to execute well and capture additional market share in a rather underpenetrated market opportunity, I believe there is a meaningful path towards improved profitability.

Yes, there will continue to be macro challenges and negative sentiment around Brazil, especially in light of the more recent political transition, however, long-term investors may be rewarded handsomely for holding onto the leading Brazilian fintech company.

Macro Pressuring the Stock

While the Brazilian economy continues to operate in a volatile fashion, investors should look on a multi-year time horizon to fully appreciate this market. Throughout 2021 and 2022, STNE was impacted by a myriad of factors, including a challenged Brazilian (and global) macro environment, rising interest rates, and uncertainty about the future.

Nevertheless, one of the biggest positive development since the global pandemic has been the acceleration in the use of digital payments. Prior to 2020, Brazil was largely a cash-based economy, with consumers and businesses slower to adopt digital payment methods. Just by looking at the company’s stock chart, investors can see how much optimism was embedded shortly after the pandemic-lows, and many thought Brazilian would rapidly shift to digital payments, with STNE being a large benefactor.

However, macro pressures such as rising interest rates and a stronger USD became sentiment overhangs, something that has continued in recent quarters.

Trading Economics

Back in December 2022, The central bank of Brazil left their interest rate at 13.75%, which marked the third consecutive meeting the interest rate did not change. During this policy meeting, the central bank noted the following.

The central bank of Brazil left its key Selic rate steady at 13.75% for a third consecutive meeting in December 2022, in line with market expectations, saying the decision aims to balance risks to inflation and growth. Policymakers said the economy is expected to slow while inflation remains elevated and also mentioned the uncertainty around the fiscal policy at a time spending boost is panned by the new President Lula. The central bank added that future monetary policy steps can be adjusted and that it will not hesitate to raise rates again if the disinflation process does not go as expected.

In my opinion, it seems likely that interest rates in Brazil may remain at elevated levels for the foreseeable future as their economy potential slows and inflation remains high.

For STNE, it’s possible that they continue to raise their rates, meaning they could potentially make a bigger spread on deposits, loans, and more. So while the economy remains uncertain, I believe is largely embedded into the company’s stock and investor sentiment.

Financial Review and Outlook

During STNE’s Q3, revenue grew 71% yoy to R$2,508 million, which came in 4.5% above the company’s guidance. In addition, adjusted EBITDA during the quarter came in at R$1,154 million, which represented a margin of 46.0%, which was slightly better than the 45.9% last quarter and much better than the 32.2% margin in the year-ago period.

StoneCo

Even though interest rates in Brazil have significantly increased over the past two years, STNE has initiated several pricing increases to help offset the corresponding higher expenses. While these price increases lag the interest rate increases, meaning revenue has been impacted near-term, the lack of ongoing interest rate hikes should be viewed as a positive. This gives STNE some time to catch up on possible price increases, ultimately benefitting their revenue line in future quarters.

StoneCo

Yes, the macro environment will likely be volatile over the near-term and can impact revenue and profitability trends. However, I continue to believe the long-term trend of digital payment accelerate will continue, thus driving a powerful tailwind that will propel long-term revenue growth.

Within Financial Services, which represents around 85% of total revenue, revenue grew 84% yoy with adjusted EBITDA margin expanding over 400bps during the quarter. As previously discussed, growth in this segment benefitted from strong performance of SMBs as well as increased TPV and take-rates, driven by STNE’s recent price increases.

When looking at Software revenue, this grew 22% yoy with adjusted EBITDA more than doubling yoy. Adjusted EBITDA margin was around 15%, which expanded around 830bps yoy, demonstrating the company’s ability to improve profitability as they scale. Over the next few quarters, management expects EBITDA margins to improve as there continues to be some non-recurring cloud expenses.

Across the business, STNE has significant room for growth, as demonstrated by their relatively unpenetrated market opportunity. Management has talked about there being millions of mid- and small-sized businesses within Brazil that they can go after. With STNE have just under 2.5 million businesses as customers, there remains a significant runway left for growth.

In the last four years our active client base increased ten-fold, reaching 2.4mn clients. Despite that growth, we still have only 11% market share in payments in Brazil and we see an addressable market of more than 13.5 million MSMBs in the country. So, there is still plenty of room to grow.

STNE is expected to report Q4 earnings some time in February and despite the ongoing macro volatility and uncertainty, I believe the company remains well positioned to deliver strong revenue growth and improving profitability metrics.

Valuation

Clearly, the Brazilian economy plays a large role in the stock’s valuation and stock price action. This continues to be a significant swing factor and given the political turmoil the country has seen in recent months, it appears Brazil will maintain their “volatile” status for the time being. In addition to the political uncertainty, the central bank has openly stated that if economic policy measures are not able to reduce inflation, they will not shy away from rising interest rates again. While over the long-term STNE can capture some benefits of spreads, this has several near-term headwinds, including a slower economy and short-term revenue pressure (as pricing actions lag rising rates).

STNE was down around 45% in 2022 and while the stock is up around 15% to start off 2023, the current ~$9.70 price is well below all-time highs of $90+. While I am not advocating for the stock to 10x near-term, I do believe there remains some upside to this story.

Currently, consensus expects 2023 EPS of $0.61 (per Yahoo! Finance), implying the stock currently trades at just ~16x 2023 P/E. In my opinion, these estimates could prove to be conservative if the macro environment starts to stabilize and if interest rates remain stable. With management expected their adjusted EBITDA margins to improve over the coming quarters, this seems to imply improving profitability, regardless of top line growth.

Longer-term, I believe the stock sets up nicely <$10. If EPS can reach $1 by 2024, then assuming the stock’s multiple remains stable at 16x, this implies a $16 stock by the end of 2023, implying a potential upside of 60%.

The above estimates do not seem overly optimistic, as it implies a stable valuation multiple and ongoing profitability improvement. Even if we don’t see $1 of EPS until 2025, then a $16 stock by the end of 2024 is still a great outcome, implying around 28% CAGR over the next two years.

One of the biggest risks to STNE’s thesis remains around the macro uncertainty and the trajectory of the Brazilian economy in the coming quarters. If we see global economies start to stabilize, then STNE’s upside could potentially be much larger than my thesis above. However, if global economies enter into a severe recession, then STNE could see increased revenue and profitability pressure, thus potentially pushing the stock much lower from current levels.

Be the first to comment