Portra

Thesis

If you’re worried about a potential recession coming in 2023, but don’t want to sit on the sidelines and risk that you will be left out of the next bull market, it might be a good idea to invest into REITs that have significant tailwinds going for them, such as the industrial sector.

One such REIT is STAG Industrial (NYSE:STAG) which is well positioned within the industrial space and has a proven track record. The company should benefit from the overall double digit sector growth as well its relatively smaller size compared to Prologis (which dominates the space). The operational results are as good as ever with occupancy above 98% and growing rents, and the company generates enough cash to meet all of its debt repayments in the near future.

However, as everyone piles into this growing sector, the stock has likely become overvalued, which could negatively affect the total return earned and lead to underperforming the overall market. I only buy companies that are well positioned within their sector, financially reasonably healthy and undervalued (or occasionally fairly valued with high expected growth rates). Since STAG doesn’t fulfil all of these criteria, it’s a HOLD for me. With that said, it’s definitely a stock to watch, because it can be a good buy at the right price.

Industry with significant tailwinds

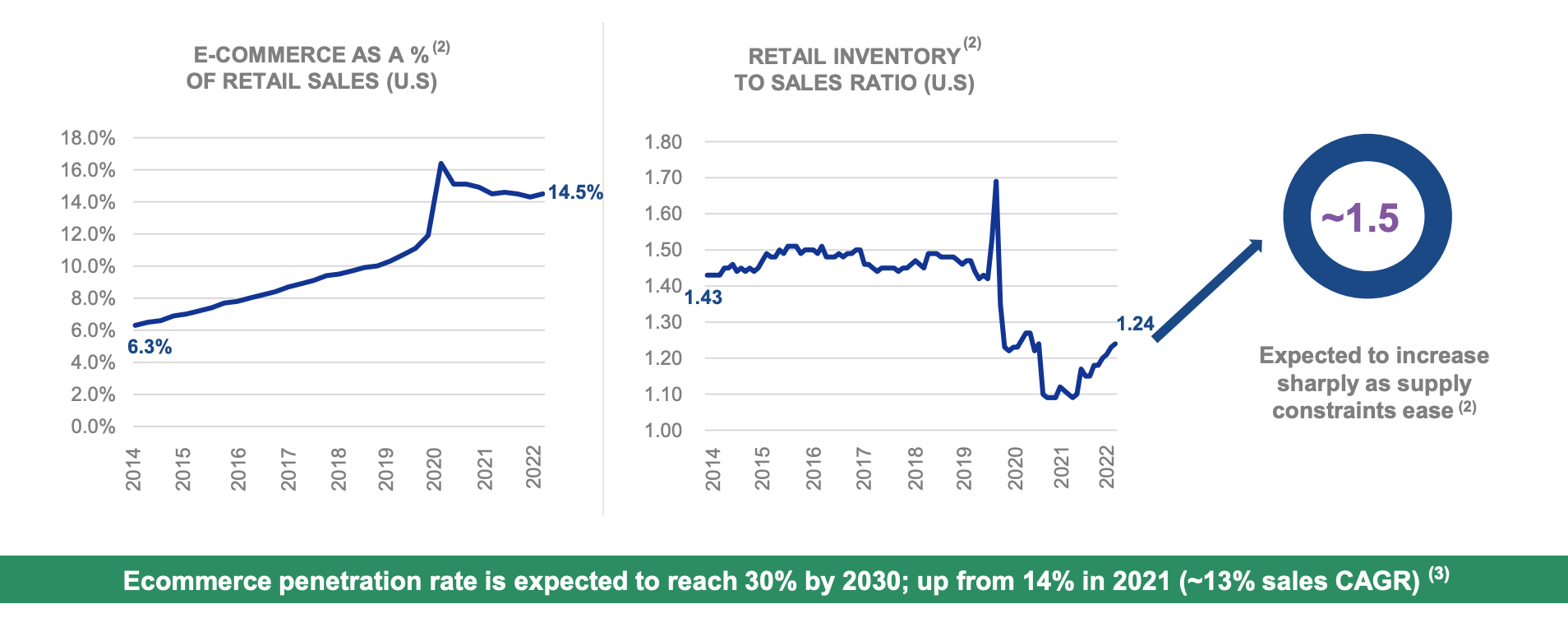

The industrial/logistics sector has seen a boom through the pandemic, but unlike some stay-at-home stocks whose rise has been short lived (I am looking at you Zoom and Peloton), the e-commerce industry (the main driver of demand of industrial space) is likely here to stay. Not only that, according to STAG e-commerce is expected to reach 30% of all retail sales by 2030 (up from 14.5% today). This represents a CAGR of 11% for the rest of the decade (note: I don’t know where the 13% CAGR in the picture below comes from, I did my own calculation). With such strong growth, it will be significantly easier for players within this industry to deal with hard macroeconomic conditions and I therefore expect this sector to outperform and to be able to grow their FFO faster than other sectors of REITs.

STAG Fall 2022 Report

Operations

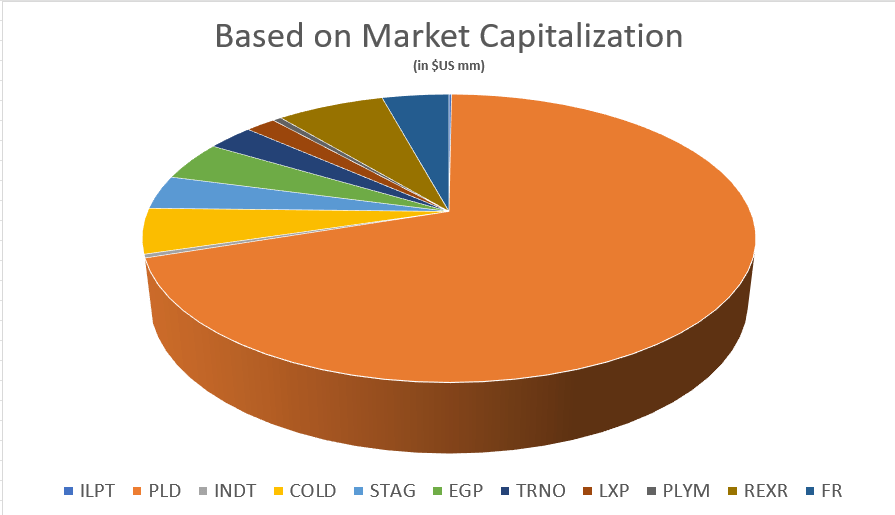

STAG Industrial, Inc. is a real estate investment trust (REIT) that specializes in acquiring and operating industrial properties in the United States. The company was founded in 2011 and is headquartered in Boston, Massachusetts. Frankly, STAG it is not the largest of industrial REITs, as this category is totally dominated by Prologis (PLD) which has a market cap triple that of all other major competitors. Still, STAG is a major player with a market cap of $6.5 Billion and its smaller size could even play to its advantage as it has more room to grow.

Brad Thomas, iREIT on Alpha

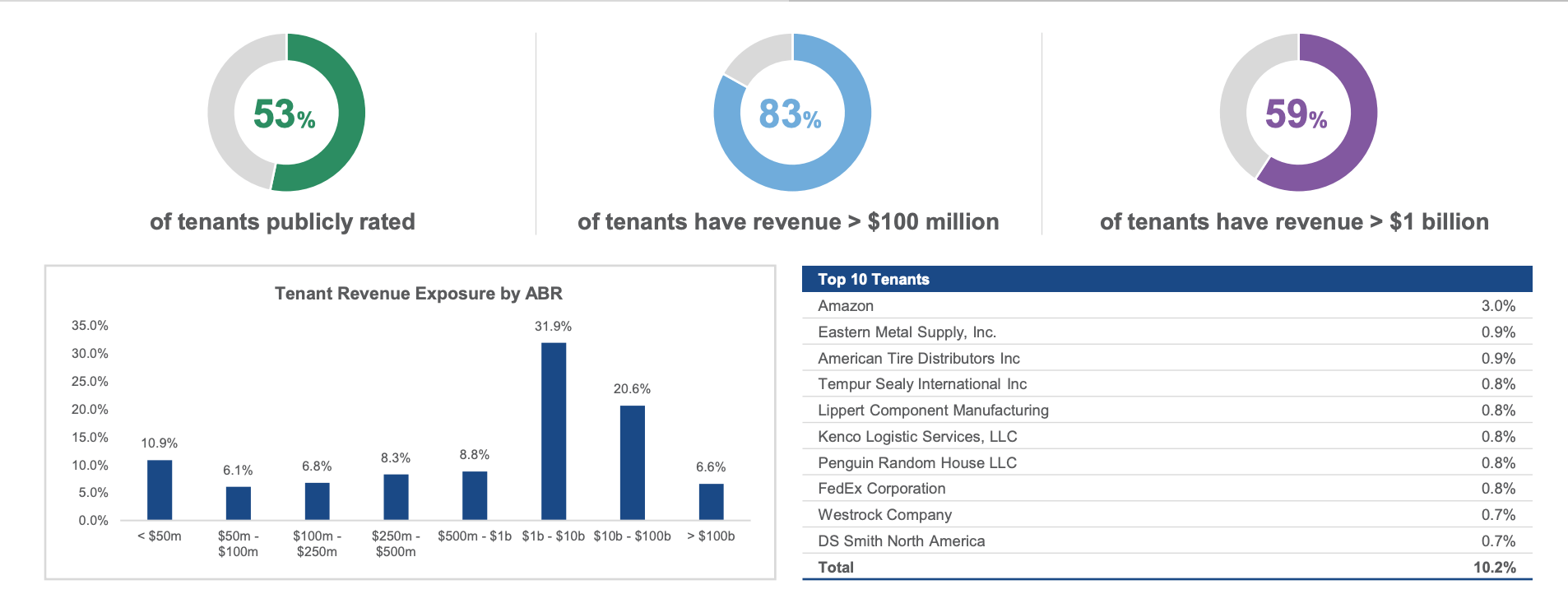

The company leases to some of the biggest and strongest companies in the world. Notably, 59% of STAG’s tenants have revenue over a billion dollars and 83% have revenue over 100 million. Moreover, the tenant mix is very diversified – Amazon being the largest tenant rents 3% of space, while the second-biggest tenant only rents 0.9% of total space. I consider this a big plus as it significantly reduces the risk to the company, should one of its tenants struggle financially.

STAG Fall 2022 Report

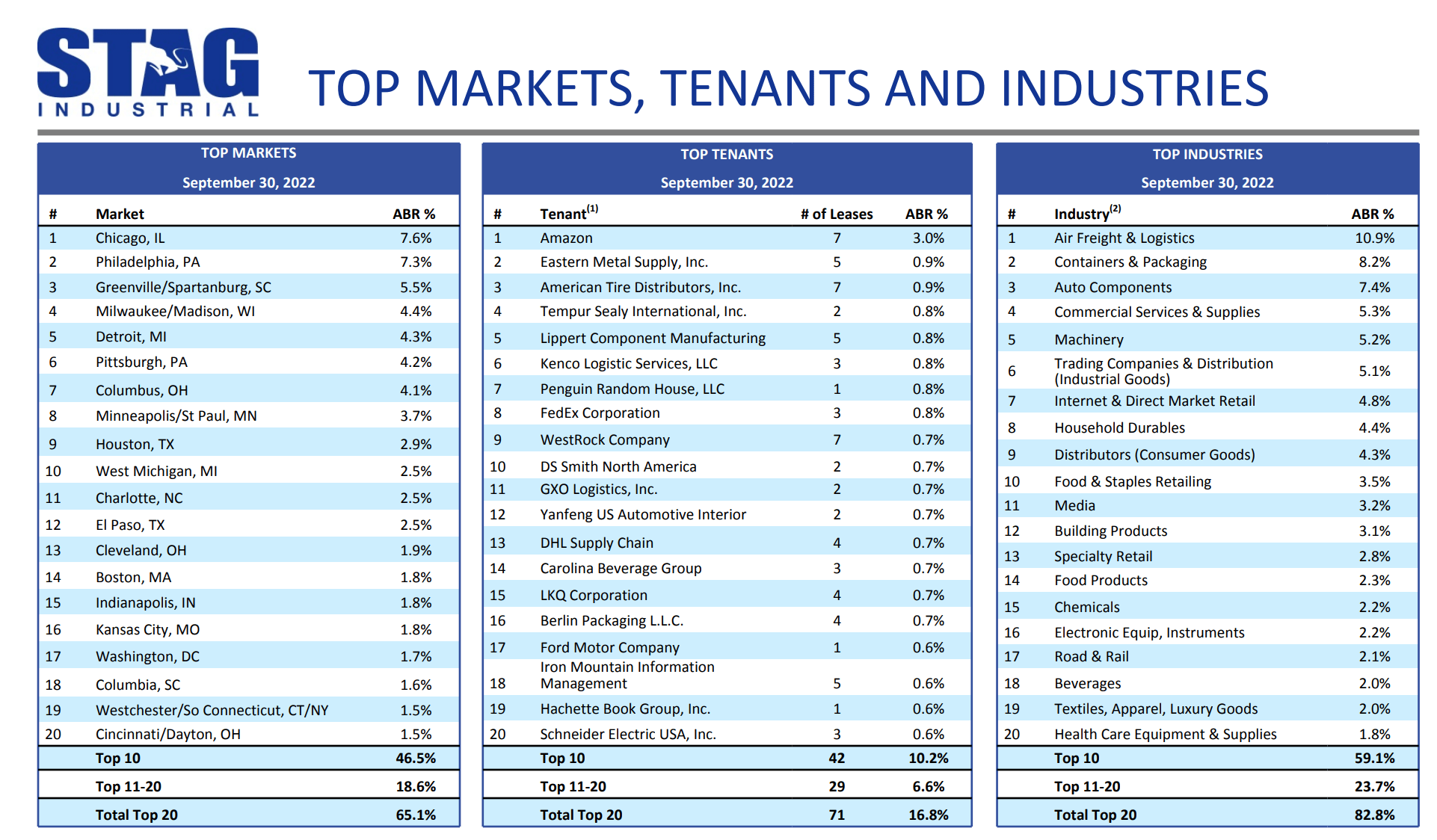

The company is just as diversified with respect to the location of their properties and the industry of their tenants. The industry of the tenant can give an indication of risk of financial problems during a recession. I like the fact that the mix is not heavily weighted in one industry and I only see a couple of sectors that could struggle significantly during an economic downturn (maybe auto components, building products and electronics). Overall, I view STAG’s operations as very well positioned, even in a potential recession.

STAG Q3 2022 Report

Digging into the financials a little deeper, the company’s operational results have been very solid through 2022. The portfolio of properties has an occupancy of 98.2% with a WAULT of 4.9 years with leases spread quite evenly over the next decade. Same store cash NOI was up 5% over the past year.

Management has improved their guidance for 2022 to an FFO of $2.20 per share during their Q3 2022 earnings call. With Q4 earnings coming up on February 15, 2023, I don’t expect a big surprise (to either side) as this has been a fairly stable business. Going forward, management as well as other analysts here on Seeking Alpha see the FFO growing at 4-5% over the next three years. This faster growth compared to a residential or office REIT is what could generate good total returns and increase the dividend over time.

Financials

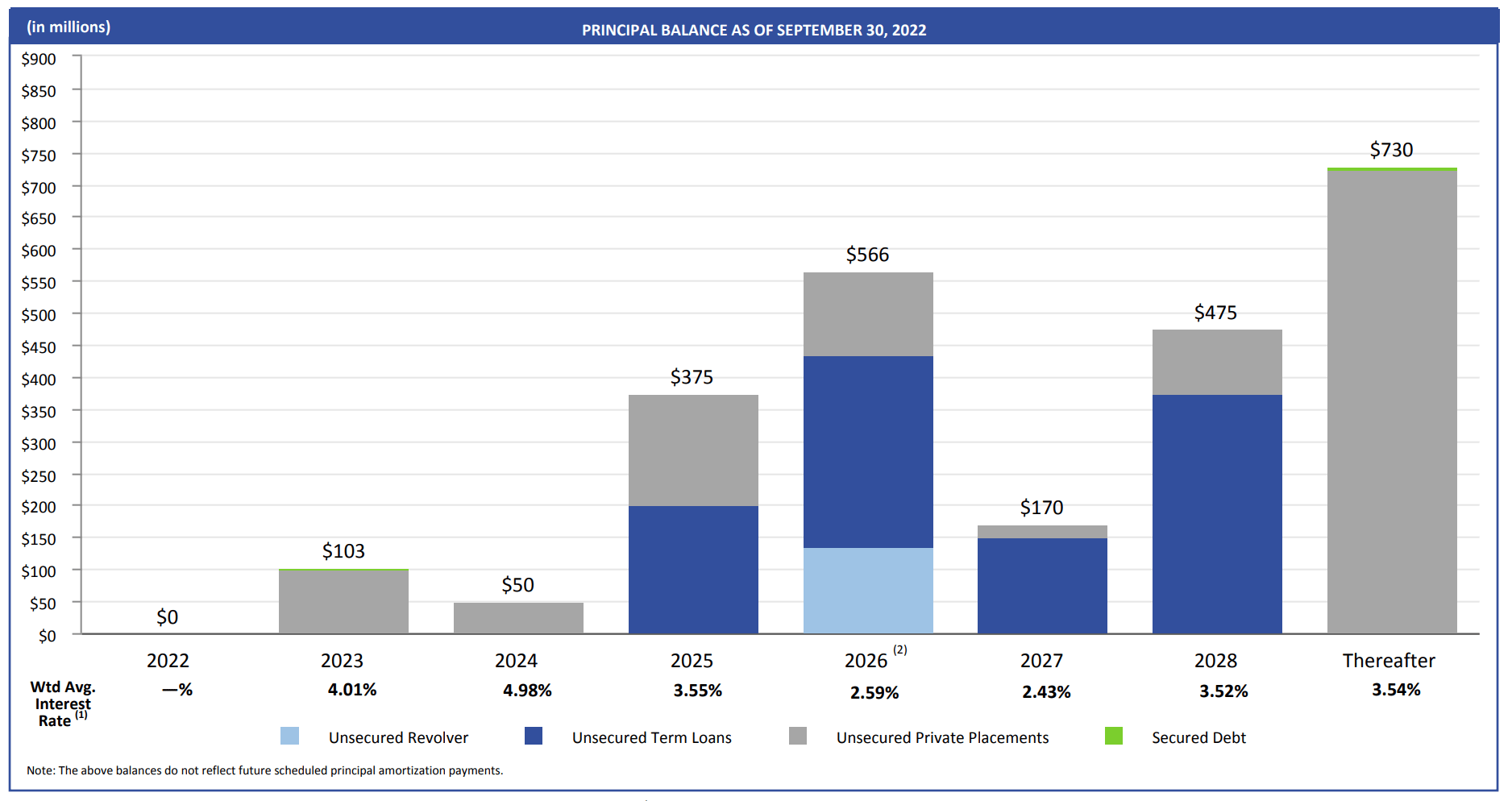

From a debt point of view, STAG is quite healthy. It has $2.5 Billion of debt outstanding at an average interest rate of 3.29%. All of their long-term debt is fixed-rate, with only the revolving credit facility being floating-rate. This is very important in the current environment with increasing interest rates, as it makes it much easier to forecast cashflows. I also like the fact that the company will not face large debt repayments over the next two years. There are two series of unsecured debt due – $103 Million in 2023 and $50 Million at rates of 4% and 5% respectively. I’m confident that the company will be able to refinance these and since the rates are already pretty high it shouldn’t have a major impact on the bottom line. Should STAG not refinance, they should be able to cover this repayment from their cash available for distribution (discussed below) or in the worst case they have a credit facility with a limit of up to $1 Billion of which less than $150 Million has been used to date which gives them ample flexibility should they need it.

STAG Q3 2022 Report

Dividend

The company is expected to post 2022 FFO of about $400 Million ($2.20 per share). Cash available for distribution (‘CAD’) is expected at $340 Million ($1.87 per share). Dividends in 2022 totalled $1.464 and were well covered with a payout ratio of 66% vs. FFO and 78% vs. CAD.

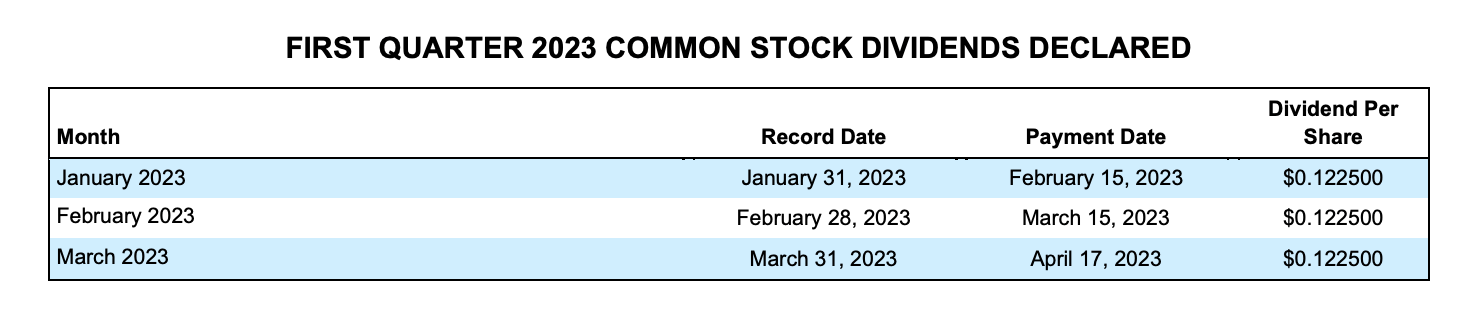

For 2023 the company has announced a symbolic dividend increase of 0.5% to $1.47 per share. With the share trading at $36.00 this represents a yield of 4.0% which is paid out monthly.

STAG announcement

Now let’s do some math to see whether the company will have enough cash to repay their debt due in 2023.

FFO is expected to grow by 4% in 2023, assuming the same rate of growth for CAD, the cash available for distribution should reach $1.95 by year-end. After the dividend of $1.47 there will be about $0.48 per share left. With 180 Million shares outstanding, there will be just under $90 Million of cash available. While not enough to repay the full $103 Million due in 2023, it is not far off and combined with cash already on their balance sheet + the available credit facility, the company should have no problem in dealing with this debt, as they are in a very good shape profitability wise.

Valuation

By now, you should be fairly comfortable with STAG’s performance, it is a very healthy company that is likely to do well in the future. The problem is that it is too obvious, resulting in a valuation that is not very appealing.

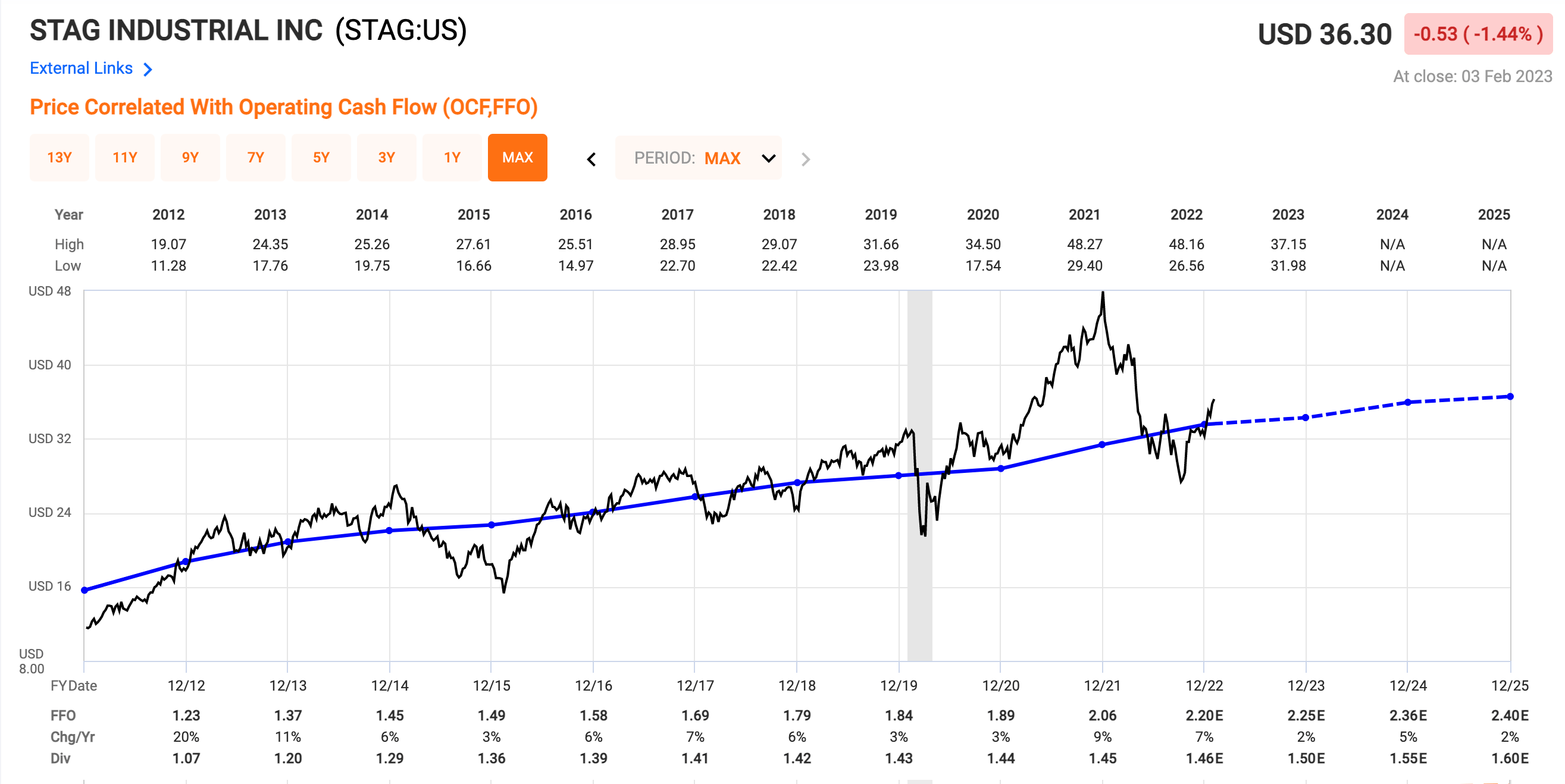

Firstly, on a relative multiple basis, STAG currently trades at 16.5x FFO, which is above its long-term historical average of 15.2x (blue line). Even if we only look at more recent history, which might be skewed to the upside because of the boom during the pandemic, STAG is by no means undervalued here.

If we assume that FFO will grow by 4%, by 2025 it should reach $2.47 per share. Multiplying this by the average multiple, we get a price target of $37.50 per share. This is essentially flat from the price today at $36.00 and with a dividend yield of only 4.0%, the total return will most likely underperform the market, unless we can get significantly higher multiples again.

Fast Graphs

From an NAV (net asset value) point of view, the story is very similar.

Properties are kept at a book value of $5.9 Billion and generate an annual NOI of around $500 Million. This means that they are kept on the books at a yield/cap rate of 8.5% which arguably is high. I would argue that a reasonable cap rate for their assets would be <6%. At a 6% cap rate, the asset would be worth $8.3 Billion. Subtracting debt of $2.5 Billion, we get an adjusted NAV of $5.8 Billion. At $36.00 a share, the market cap stands at $6.5 Billion or about 12% above the already adjusted net asset value. This tells a very similar story to that of relative multiple valuation. STAG is simply about 10% overvalued here, and therefore, I expect it to underperform the market.

Investor Takeaway

STAG is a great company. It is positioned in an industry with significant tailwinds over the next decade and has a well-diversified and efficient business model with a very reasonable debt structure. The problem, it seems, is that everyone is aware of this and the stock has become too crowded. As a result, the company has become about 10% overvalued here. For these reasons, I rate STAG stock as a HOLD here at $36.00, but will keep an eye on the stock and consider buying if the price falls below fair value (below $32.00 or so).

Be the first to comment