BitsAndSplits

Introduction:

The purpose of this article is to provide a transparent and thorough bullish analysis of unknown and misunderstood small-cap, SSC Security Services Corporation (TSXV:SECU:CA)(OTCQX:SECUF), so that investors can decide for themselves whether this is an investment that suits them.

Because there is much less scrutiny and information available in the small-cap space, due diligence is of particular importance. I’ve read the public filings, perused the investor presentations, done the financial modeling, and had a long and insightful chat with SSC CFO Brad Farquhar. An investment in SSC at current prices, I conclude, could offer investors a non-speculative way to multiply their capital; SECU has the potential to be a multi-bagger.

It turns out Brad is well-acquainted with multi-baggers, friendly even, personally knowing Chris Mayers, the successful portfolio manager and author behind the influential book, “100 Baggers: Stocks That Return 100-1 and How to Find Them.” That piqued my interest, and I hope yours as well, knowing that the CFO is interested in generating wealth, not just preserving it.

Let’s begin!

The Story

The concept of ownership is at the center of my current investing philosophy. With every investment I want to feel like an owner of that business, not just an investor in a stock. This way I tend to think longer term and am less likely to sell before the return is fully realized. To get to that point, where I feel like an owner, I need to go beyond the financial statements and earnings calls, I need to know the story of the people involved, where the business has come from, and how it operates. In short, an investor knows just the financials, an owner knows the story.

According to CFO Brad Farquhar, he met Doug Emsley, the current CEO of SSC, while working in politics in Regina, Saskatchewan (which sounds to a Canadian as remote as Omaha, Nebraska does to Americans). Before standing for election, Brad did some consulting work for Doug on a business opportunity involving Saskatchewan farmland. Saskatchewan had recently lifted a law that had restricted ownership of farmland to Saskatchewan residents only. Despite this law being repealed, opening the land to buyers from other provinces, farmland in Saskatchewan was selling for almost half the price of farmland in neighboring provinces. Fortunately for us, Brad lost the election and stayed on working with Doug at this golden arbitrage opportunity.

They raised money and bought land which they then rented to farmers. This enterprise, known as Assiniboia Farmland, lasted for 8 years until the business was bought by the Canadian Pension Plan. According to Brad, they returned 19.9% annually during those 8 years (the Omaha of Canada indeed!). During that time, the management team gained expertise in farming and generated enough wealth to begin undertaking their next idea.

SSC’s Management Team’s first success (Seeking Alpha Article)

The next opportunity was in the fact that canola farmers didn’t have the cash flow to efficiently maximize the yields and profits of the land. Combining their capital and farmland expertise, management created Input Capital, which loaned timely cash to farmers to efficiently increase crop yield and, instead of being repaid principal and interest, received in exchange the option to purchase a portion of the crop at a fixed price, which was then sold at a profit. This business model is common in the mining industry, known as royalty streaming. Blue-chip Franco-Nevada Corp is one of its most well-known and successful practitioners. By 2015, Input Capital was having similarly extraordinary success, growing revenues quickly and with high margins (see this SA article for more details). The stock had institutional ownership and had generated significant returns.

The plan hit a snag when some farmers defaulted on their loans and China banned canola imports from Canada. Input Capital, despite getting all their capital back from the defaulted farmers after court proceedings, and the China ban not greatly impacting business, was nonetheless unable to attract interest in its stock. By 2019, management decided to begin wrapping up its streaming contracts, liquidating its assets and finding a new business. As Brad noted, “You can have the best mousetrap but if no one wants to fund it, then it’s not going to work.” A new idea was needed.

The best ideas are often hidden in plain sight, and such was the case with Input Capital’s decision to move into the security business. SSC’s CEO Doug Emsley and COO Blair Ross, had previously built and sold a security company in the early 2000s and had gotten right back into the business with a security company called SRG Security Resource Group Inc. when their non-competes expired, were looking to expand; they needed capital. The security company’s offices were just down the hall from Input Capital’s and a plan was hatched. Input Capital provided funds from the wrapping up of the streaming business and SRG provided the security platform and operational expertise. In 2021, Input Capital acquired SRG (essentially just taking over the offices down the hall), changed its name to SSC Security Services Corp and a new era for the team from Assiniboia Farmland/Input Capital/SSC Security Services Corp began.

Last year, using Input Capital’s steadily liquidating assets, Security Services Corp went out and acquired Logixx, a security company three times their size, to become Canada’s largest publicly traded security company. They purchased Logixx at just 3x EBITDA, a steal when we consider that well-run, growing companies which provide corporate services often trade in the 6-12x range. If SECU can get some attention and trade in that range, the acquisition of Logixx could be a two, three, or four-bagger on valuation alone.

By the end of 2023, most of the remaining canola streaming contracts will be wrapped up, the land owned or held as security will be mostly sold, and the capital invested, representing somewhere between $13.3M and $18M, will be turned into cash. Add that to SSC’s $11.2M current cash position, and between $5M and $7.5M in cash they expect to put back on the balance sheet after optimizing Logixx’s accounts receivable, and you get a total of up to $36.5M, or over 60% of SECU’s current market cap, ready to be deployed into expanding security operations and growing shareholder value through share buybacks. If $1T Amazon (AMZN) had SSC’s balance sheet it would have no debt and $500-$600B of cash; SSC is in incredible financial position.

Because of multiple name and industry changes, it can be difficult to get a sense of with what and whom we’re becoming part-owner, but with this story its clear (to me) that management is highly experienced and competent; Security Services Corporation is no speculative small-cap.

They’ve built and sold fantastic businesses, raised capital successfully, and generated excellent returns for shareholders multiple times. The only stain on their shirt is not being able to sell the canola streaming idea to institutional investors after some mishaps that were out of their control. This is as understandable as it is unfortunate though, as the streaming business model is not simple, and no one had ever done it with canola before. Security, by contrast, is easily understood and with plenty of precedent. The security business is also the business Doug and Blair know best, having even been in the security business since 1988, much longer than agriculture. Moreover, SSC’s board of directors features two former board members of the Bank of Canada, a former Chairman of accounting firm Deloitte, and the former Chairman of the Ontario Securities Commission; a group with this pedigree is sure to impress institutions as well. As such, I believe the chances of persistent undervaluation of Security Services Corporation are lower than they were for Input Capital.

Management is aware of the issue and is planning an awareness campaign to combat the malaise in which their stock is stuck. Brad tells me that recently, he has been doing half a dozen calls a week with interested institutional investors, which is a positive sign.

The main issue this story highlights is not a problem with the quality of the business or the acumen of management, but the perception of the stock in the market. This, from a shareholders perspective could be frustrating, but from a buyers perspective could be a fantastic opportunity.

The Business

The short version is that Security Services Corporation is the right size, with the right balance sheet, in the right market and with the right management to be growing consistently organically and by acquisition with relatively few risks, including competition and inflation. Estimated 14% returns on equity demonstrate this. A longer analysis is to follow, but this is the gist.

Brad described the competitive landscape as having a few big players, like Securitas (OTCPK:SCTBF), Garda, and Allied Universal, which count employees in the hundreds of thousands, some medium-sized players like SSC which count employees by the thousands, like Paladin, Paragon and Scarlett, and plenty of small “mom-and-pop” companies which count employees in the hundreds, or even tens. Like the astute observations that Saskatchewan farmland was cheaper than it should have been, or canola farmers needed help with cash flow, management knows from experience that these tiny security companies are too small to be of interest to the large companies and that relatively few well-capitalized, well-managed, medium-sized security companies exist to acquire them. Thus, the business opportunity emerged: grow organically and roll-up mom-and-pop security operations.

Because SECU has enough capital to make acquisitions but is small enough for tiny acquisitions to make a difference to the top and bottom line, a niche is carved out. I wouldn’t call it a moat, but a niche it certainly is. These acquisition targets are usually run by one person, many of whom are thinking of selling and retiring. Beneficially, Doug and Blair, with their decades in the industry personally know many of these operators. Even I do! My friend’s dad runs a security operation where I grew up, is over 60 and must be looking to retire. Who else is going to buy his business other than another security company? I like having some personal connection that corroborates a business opportunity, like when I hear someone happily chatting about a business I own, because I know there is at least a grain of truth in the bullish thesis. There are many of these tiny security companies and SSC has plenty of capital and a long way to go before acquiring them stops being accretive.

Compellingly, these acquisitions can be made at very reasonable valuations. Brad noted that deals are often done between 4x and 6x EBITDA, with half up front and, because the former owner is often kept on to ease the transition and maintain relationships, the rest of the payment is performance-based over a couple of years. This has the dual benefit of allowing SSC to not lay out as much cash up front (leaving more for other opportunities as they arise), and if the acquired business doesn’t perform well over the years following, SSC can get it for less than 4x-6x. This sounds reasonable enough, but the opportunity for even better value exists.

Many of these potential acquisition targets are not operating at peak efficiency (peak would be around 5% EBITDA margins), often because of administrative inefficiencies. Significantly though, many of these small owners need to use lines of credit to pay bills while they wait up to 2-3 months for clients to pay for services already provided. These owners are essentially having their personal cash taxed by banks just to provide working capital for their business. With interest rates now greater than zero, increasing debt costs are scraping percentages off already low margins; EBITDA is drying up. Some of these small companies are sure to be distressed, retirements are in question.

SSC is in the position where they can use their business expertise and war chest of cash to clean up these issues, business inefficiencies and debt, which are dragging on margins of some small security companies. Because the multiple paid on EBITDA does not matter much when there is not much EBITDA to begin with, SSC could pay quite a low price, relieve the previous owner of onerous working capital obligations (potentially allowing them to retire), “bring [the business] up to SSC standard,” as Brad described it, and generate a good-sized return for shareholders. SSC could essentially acquire some businesses for the cost of their working capital plus some performance-based costs in the years following. Inorganic growth opportunities such as these are an extremely compelling reason to own SECU.

In addition to the inorganic growth opportunity just presented, organic growth is expected. Management expects organic growth of 10% and the company’s (lone) analyst agrees with this suggestion. SSC has manned guarding, which makes up around 85-90% of revenue, electronic security, like cameras and card access systems, and cyber security, meaning keeping computer networks safe; the last two of which make up around 10-15% of revenue, but are higher margin. Management expects growth in EBITDA to come from increasing margins (past 5%) as electronic and cyber security take up more of the revenue mix, in addition to cross-selling, upselling, and getting new contracts.

The demand for security could decrease, slowing organic growth, but it seems unlikely. A recent article in the Globe and Mail pointed out that in Ontario alone there were more than 100,000 private security guards in 2021, a massive increase from 2016, when there were less than 70,000. Moreover, retail giants Target and Walmart have reported significant increases in shoplifting. Target, in the first three quarters of 2022 reported almost half a million dollars in merchandise lifted, a 50% increase from the prior year, and 2022 wasn’t even over. The public does not seem supportive of increasing funding to the police, and governments are quite indebted so can’t spend much anyways. The author of the Globe and Mail article pointed out, “The rise of private security is, to be sure, a symptom of something horribly wrong with society,” then listed ways in which it could be invested. Notably, he neglected to mention SSC, the largest publicly traded private security company in Canada (he knows now though). Organic growth for SSC is not going to light the world on fire, but it’s likely not slowing.

SSC expects to double revenues in the next 3-5 years, through a combination of organic and inorganic growth. What makes SSC more compelling than the average fast-growing company is the fact that it can do this with the resources it already has. For this doubling of revenues there will be no need for debt, dilution, unsustainably high organic growth, or a questionably high number of acquisitions. It simply needs to acquire a couple small companies ($5M or so each transaction) with cash it already has and grow at 10%. Neither of which criteria are particularly burdensome. Critically, this leaves room to return plenty of capital to shareholders in the form of buybacks and/or dividend increases.

Management emphasizes their per share financials for a reason. Over the last 5 years they’ve bought back 41% of their stock and intend to continue aggressive buybacks for as long as their own stock is more attractive than other uses of cash. With cash and soon-to-be-cash making up 60% of the market cap of SECU right now, the potential for continued buybacks is massive. SECU could double EBITDA/share with no growth whatsoever, just through the elimination of shares. That is a powerful weapon to have in the arsenal, especially when the stock is trading at such low multiples.

Management also personally owns 36% of the outstanding shares and continues to buy more, so is well-incentivized to build shareholder value through buybacks and/or accretive acquisitions; an investment in SECU is becoming a co-owner with management, which can’t be stressed enough. A management who eats their own cooking is much more likely to make good decisions regarding that meal. Take the Logixx deal described earlier. They did that deal at very conservative multiples and showed great discipline. Compare that to the managers of CN Rail and CP Rail who got into a bidding war for Kansas City Southern, jumping over themselves to pay extraordinary multiples. If management of CN and CP were 36% owners, like SSC’s management are, I doubt they would have been so eager. As a shareholder, we have that added safety, that our management think like owners too. Ownership continues to be key.

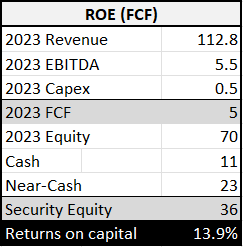

This is reflected in SSC’s returns on capital. Returns on capital are generally viewed as the primary quantitative metric by which to judge the effectiveness of management because it measures how much money is made as a percentage of equity in the business. The less money it takes to make money is clearly more desirable, and it’s the goal of every management to be as efficient in this regard as possible; it is in fact their main job. Returns on capital in the teens is generally regarded as good, especially when bond yields are as low as they are now (the 10-year treasury bond is around 3.5% at time of writing) because the risk-free alternative is unappealing in relation. We would like to see SSC’s returns on capital in the teens.

For SSC, determining returns on capital is a little difficult because the capital employed in and made from the legacy streaming operation has not yet been totally recycled. If we exclude all items related to canola streaming and focus solely on the security business, we find that, according to the analysts, SSC is set to generate around $5 to $5.5M of free cash flow in 2023 from around $110M of revenue. Equity (book value) stands at around $70M, but if we exclude the $34M-ish in cash and near-cash then that number goes down to around $36M dollars, implying a free cash flow return on equity of around 14%.

There is some variability as the near-cash could be anywhere from $18.3M to $25.5M, but doesn’t change the fact returns on capital do not appear concerning. (Author’s Calculation – Numbers from Investor Presentation)

For a low margin business that uses no debt and has just transitioned from a canola streaming operation, this is a very satisfactory return on equity. Management is clearly treating the company’s equity as if it were their own (which 36% of it is).

A comparison is often beneficial when discussing less scrutinized companies; GDI Integrated Facility Services (OTCPK:GDIFF, GDI:CA) is the best comparison to what Security Services Corporation could be. GDI offers mainly janitorial services while SSC does security services. Both have similar margins, similar clients, and a similar business model: grow organically at around 10-15% and roll-up mom-and-pop operations in a fragmented market. In the last 10 years, GDI has returned 1200%, a 12-bagger; an investment of $10,000 has become $120,000. It perhaps shouldn’t come as a surprise that management are significant owners of this business as well.

It would have been tough to buy a small-cap, unknown janitorial roll-up 10 years ago, but with SSC we might have a second crack at it. (Chart from Seeking Alpha)

Of course, we shouldn’t expect this type of return, but the fact it’s been done before by a similar business in a similar market should give us pause to think. If SECU could do even half of what GDI has done, the results would be dramatic.

SSC is a well-managed, well-capitalized, insider-owned company with a niche in a steady industry, and with plenty of options for generating low risk, and potentially considerable, shareholder returns.

This sounds excellent, but perhaps it’s time we temper our expectations.

The Risks

The first, and most prevalent concern, is wage pressure. As we all know, the current market environment is very concerned about inflation and rising wages. Security guarding, being a people business, is clearly affected by this issue. I brought up this concern with Brad in our discussion. The first thing he noted was that all contracts with corporates have annual price increases built-in, so SSC can, over time, pass on some of the wage pressure. Inflation-wise, many clients were also willing to accept a fuel surcharge that was not part of the contract when fuel prices were soaring. Furthermore, SSC conferred with clients when costs were rising quite quickly, and most consented to other non-contractual price increases. Clearly, SSC has good relationships with its clients, which pays off when inflation occurs.

When the relationship is not enough though, SSC also has leverage. Brad relayed to me that all contracts have a built-in “30-day out” clause, meaning either party can exit the contract with 30 days’ notice. At first glance, we might think this makes SSC’s revenue unstable (although they’ve never lost a client to a service issue and it’s a pain to hire a new security firm), but we can also see this clause as benefiting SSC. In a situation where SSC is no longer making money on a contract, they could go to the client and ask to work something out, but if nothing can be worked out, SSC can drop the contract in 30 days rather than be stuck with it for the duration of the contract (usually 3-5 years). Through relationships and contractual leverage, as Brad said, “Inflation is not the bogeyman it could be.” This is not to discount real price pressures, but does serve to show investors that inflation is not a reason to pass over this company.

Secondly, there is not much to demonstrably differentiate one company’s manned guarding from another’s; that is to say, competition for contracts does threaten organic growth. I brought this up with Brad as well, who replied that there have been cases where they’ve been underbid on tenders, only to have been contacted later by the counterparty, asking them to take over the contract when the lowest bidder turned out to be incompetent. SSC clearly has differentiated themselves as a quality service provider as much as they can, judging by this story and the fact they’ve never lost a client for service issues. From an organic growth point of view, SSC is doing about as well as we can expect, though it may just be a fact of life for security company investors that moats don’t really exist. It is something to take into account when considering investing in SECU.

Inorganic growth-wise however, as we detailed above, is where SSC is different from competition. The fish where SSC goes fishing are simply too small for the big players, and other SSC-sized fish are unlikely to have the amount of capital and quality of management that SSC does. It may not be a moat in the Buffett sense, but it is certainly a niche, and one that has worked well so far and was demonstrably successful for the janitorial services roll-up 12-bagger, GDI.

This leads to a logical third concern, that management is not as quality as I’m making them out to be. It’s true, I talked to the CFO, Brad Farquhar, and we got along well, so I may be biased, but if we look at their track record it’s hard to find fault. Their acquisition of Logixx, SRG and a smaller company called Impact, were all done at reasonable multiples and in Q4, this combination did produce around 5% EBITDA margins (excluding legacy operations), just about the maximum a manned guarding service can achieve. The CEO and COO have built and sold security companies before, the most recent being SRG to Input Capital, with a previous sale in 2000 to Securitas. At the time of sale, SRG had 7% margins due to operational efficiencies and use of technology. Looking back further, this management team sold a 20% annual returning farmland business to the Canadian Pension Plan and their next idea, canola royalty streaming, was ingenious and profitable but simply failed to capture investor attention due to its novelty and a shadow being cast on it by events that were out of their control. If I’m not comfortable with a track record like that, then there are very few management teams with whom I would be comfortable.

The main fault I can find in management is that they may not be great salespeople for their stock. This may sound like a strange criticism since we tend not to think of that as their job, but in small-cap land this can be important because many companies compete for little attention. We need not look farther than Input Capital as an example of a quality business that can be perpetually undervalued because a few events made its mild complexity burdensome for investors’ small-cap attention span. As I mentioned earlier, I don’t see investors ignoring Security Services Corporation like they did Input Capital, because it’s much more understandable and defensive (literally and figuratively); Security Services Corporation is an easier sell than Input Capital was, which should be good news to investors, especially if management are not particularly adept salespeople.

Brad, for his part contests this point, and for the reader’s benefit I inserted his reply, as I found it very informative:

I would argue this point based on this: in 2015 and 2016, we won “Best Investor Relations by a TSXV Company” back-to-back. We are just emerging from a period where our story was not very visible in our financial statements, and there was background noise from the old business. That’s past now, and the Logixx acquisition gives us the critical mass for going forward. We have been waiting for the story to develop sufficiently to have a compelling narrative, and now that it is in place, we are only now ramping up our investor outreach program (since Jan 1, 2023).

I think that even in choosing the name, “SSC Security Services Corp” management was going for simplicity and clarity. They could have kept SRG or Logixx, but chose not to. Though the Globe and Mail still couldn’t find their stock, I expect the planned awareness campaign should rectify some institutional blindness towards SECU. That said, there is the possibility that they fly under the radar for some time longer. This could be viewed as a golden buying opportunity by patient investors.

To sum, SSC faces cost pressures from inflation, competition for contracts, a reliance on managerial execution, and the very real possibility of a long wait before SECU is valued properly by the market, if ever. Due to relationships and contractual leverage “inflation is not the bogeyman it could be,” SSC’s uniqueness has carved out a niche for itself, management’s track record suggests they can be relied upon, and the relative simplicity of SSC and lessons learned from Input Capital make perpetual undervaluation seem less likely.

Readers are more than welcome to disagree, as it would only benefit me, but at present nothing dissuades me from becoming a part-owner of SECU – least of all the valuation.

The Valuation

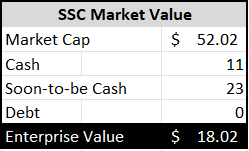

At the current price of ~$2.70 a share, SECU has a market cap of around $52.5M CAD. Factor in that $11M of that is cash, and around $23M of capital will be freed up by the end of 2024, and we see that the market is valuing SSC’s security operations at ~$18M:

Just for reference, that is less than what SSC paid for Logixx, now just a component of their business. (Author’s Calculation)

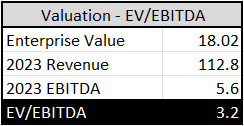

With the acquisition of Logixx, SSC’s pro forma revenue for 2022 was around $100M. SECU’s lone analyst estimates full-year 2023 revenues of $112.8M, representing 12.8% organic growth. EBITDA is estimated to be $5.6M. Below, we can see that SECU currently trades at ~3x EV/EBITDA.

At around 3x EV/EBITDA, SECU is selling for less than the minimum 6x it would garner in private markets. It’s a good example of how public market inefficiencies can be exploited by astute investors. (Table)

SECU’s valuation is lower than the 4-6x EV/EBITDA they pay for other, often lower quality, security companies. This should help elucidate why buybacks are such a powerful tool for SSC. Where else will they find a security company as quality as SSC that will agree to be sold for 3x EV/EBITDA? Only their own stock in the public market.

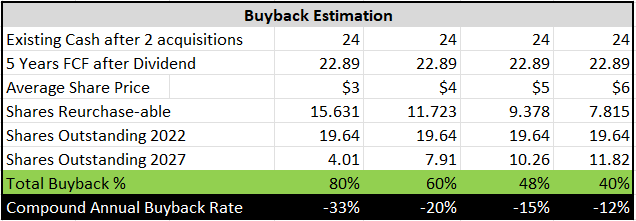

It is difficult to know exactly to what extent management will buy back shares as it is dependent on many factors, especially the relative valuations of acquisition targets and SECU stock. If SECU continues to be valued below what other companies could be bought for, then I expect management will continue to buy back stock. If not, then they may cease eliminating shares and be more acquisitive. It is difficult to know, but for reference I’ve made a table to get a sense of what buybacks could be like under different scenarios:

To accomplish the higher end of the buybacks, they’d have to start buying back shares from people like me, which I won’t be relinquishing easily! (Author’s Calculations)

In the last 5 years, SSC has bought back 41% of its shares, and, as we can see, that trend looks like it could continue if undervaluation persists. It’s not realistic, but just to illustrate the balance sheet’s optionality, if SECU were to take the next 5 years of free cash flow (after the dividend), all existing cash and soon-to-be-cash (passing on acquisitions), and spend it on their own stock, they could buy back the entire company by 2027 at current prices. The power of a strong balance sheet and an undervalued stock should not be ignored.

Sometimes, however, companies deserve low multiples because they have ceased growing or there is something fundamentally wrong with them; these are termed “value traps.” Is SECU a value trap? I don’t think so, as they have steady organic growth and plenty of opportunities for accretive acquisitions, but it is still a good exercise to make sure.

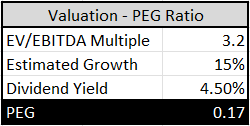

A useful way to avoid value traps is to consult Peter Lynch’s PEG ratio, an improvement on the PE ratio , because it combines growth assumptions with multiples. A PEG of 1 is when a company’s multiple on earnings matches the growth rate of those earnings (eg. 20% growth and a 20 PE). PEGs below 1 are considered favorable, while PEGs above 1 imply sub-par returns.

Management of SECU expect to double revenues and EBITDA by 2027 at the latest, implying a conservative annual growth rate of 15%. They also pay a dividend that currently yields around 4.5%. If we divide those two return factors, estimated growth and dividend yield, by SECU’s multiple of 3.2, we arrive at an incredibly bullish PEG of just 0.17.

3.2/19.5 = 0.17 (Author’s Calculations)

Peter Lynch thought he found treasure when he came across a company with a PEG of 0.5, and here we have SECU with a PEG of 0.17. It makes intuitive sense if consider that SECU’s EV/EBITDA multiple could easily double to 6x (that’s what they acquire security companies for) and growth of 15% implies a doubling of EBITDA by 2027. Combine just those two factors and SECU is already a triple or quadruple. At the very least, we’ve established that SECU’s valuation is compelling, not a trap.

To be more stringent, I’ve conducted a discounted cash flow analysis. This way we can test assumptions and see what is and is not priced into the stock to find out if we’re comfortable with the probabilities. Thomas Hayes, of Great Hill Capital and hedgefundtips.com, frequently says, “Amateurs deal in absolutes and professionals deal in probabilities.” A DCF analysis is the way to get at those probabilities.

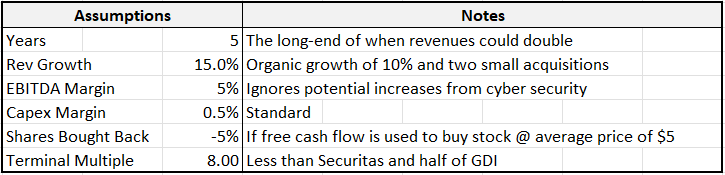

To come up with a conservative fair value, I use the following assumptions:

For context, Securitas historically trades around 10x EV/EBITDA and GDI around 12x. (Author’s Calculations and Notes)

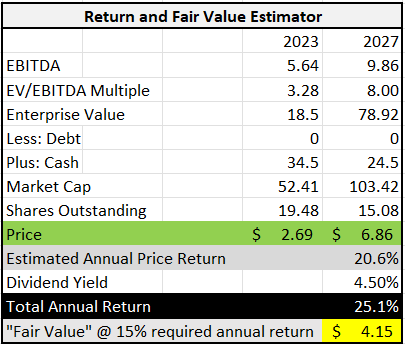

As you can see in the notes, none of these assumptions are particularly aggressive, at all. The business could easily make more than two small acquisitions, grow faster organically, have greater than 5% margins, buy back shares at a lower average price, dip into existing cash to buy back shares and/or be priced like comparable companies. Based on these conservative assumptions I get the following valuation:

A reminder that none of this is precise and is open to interpretation. It serves as a guide for expectations, not a prediction. (Author’s Calculations)

As we can see, even with an almost unrealistically conservative set of assumptions, SECU is still set to return 25% annually over the next 5 years (nearing a triple), with around $24.5M of cash on the balance sheet unused. If we were to require a minimum return of 15% from SECU, we would be buying it right up to $4.15/share, or a full 35% higher than it is now. That is a significant margin of safety on already safe assumptions.

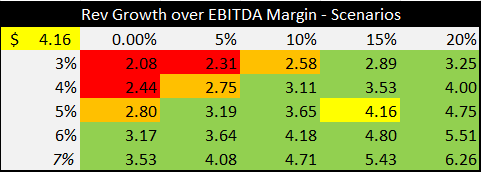

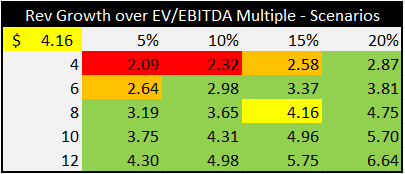

What assumptions then is the current price building in? What is the market thinking will happen to the company in the future to price it so low? Below is a sensitivity analysis that adjusts the fair value of SECU in different revenue growth and EBITDA margin scenarios to find out:

Notably, one scenario our current price is pricing in is only 5% growth and a reduction of margins to 4%, both of which seem unlikely. (Author’s Calculations)

The yellow box is our base-case, outlined in the assumptions above. The orange boxes are the scenarios implied in the current price, where a 15% total return can be expected. The red cells are scenarios where downside is not priced in, while the green are all scenarios with unexpected upside. In my opinion, the stock is pricing in some pretty poor performance, while ignoring the potential for outperformance. You can use this table to decide for yourself, however.

From a profit and growth perspective, SECU looks to have a significant margin of safety. What about from a valuation standpoint? Below is a second sensitivity analysis that tests the fair value estimate against different revenue growth scenarios and EV/EBITDA multiples:

The idea that SSC could return 15% even if they grow revenues at 5% and only garner a 6x EV/EBITDA multiple (the orange 2.64 scenario) indicates a solid margin of safety (Author’s Calculations)

As before, the yellow cell is the base-case scenario, the orange cells are what’s priced in (for a 15% return), the red cells are downside not priced in and the green cells are upside not priced in. What I take from this analysis is that if SECU gets back to a point where it is valued like the companies it buys on the private market (4-6x EBITDA), then there is very little chance of any valuation downside. Its EV/EBITDA multiple is so low that from a valuation standpoint, it is very unlikely a situation occurs where investors get a sub-par return.

To sum, SECU’s valuation is extremely undemanding and with considerable margin of safety. It puts SSC’s management team is in this wonderful position where they have excellent growth opportunities that could lead to a re-valuation, but if that re-valuation doesn’t occur, then they have the cash to buy a significant amount of their own stock. Either way, owners win. If I knew nothing else about this company, that alone might make me buy into it.

Conclusion:

Small size, optionality provided by the balance sheet, clear growth opportunities, exceptional owner-managers, and a rock-bottom valuation make SSC Security Services Corp a potential multi-bagger investors ought to at least closely consider.

I think the man who coined the term “multi-bagger,” famed investor Peter Lynch, would agree. He described his perfect stock in his book “One Up on Wall Street” as having the following characteristics:

It sounds dull, it does something dull, it does something disagreeable or depressing, it’s a spinoff, institutions don’t own it, analysts don’t cover it, it’s in a low-growth industry, it has a niche, people must keep buying it, it’s a user of technology, the insiders are buyers, the company is buying back shares and something is spooking investors out of it.

If Peter Lynch doesn’t already own SECU, I reckon it won’t be long.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment