Zolak

A Quick Take On Squarex Pharmaceutical Corporation

Squarex Pharmaceutical Corporation (SQRX) has filed to raise $17.8 million in an IPO of its common stock, according to an S-1 registration statement.

The firm is a biopharma developing a treatment for oral herpes simplex.

I’ll provide an update when we learn more about the IPO from management.

Squarex Overview

Saint Paul, Minnesota-based Squarex Pharmaceutical Corporation was founded to develop a cold sore treatment drug for herpes simplex with a goal to also investigate treatment of herpes labialis.

Management is headed by founder and CEO Hugh McTavish, Ph.D., who has been with the firm since inception in 2012 and has been President of IGF Oncology and a patent attorney in solo practice.

The firm’s only candidate, SQX770, has completed Phase 1 and 2 trials and

showed a statistically significant effect in non-primary endpoints in both trials of delaying time to next herpes labialis or oral herpes (cold sore) outbreak (from day 1 to day 121 in the Phase 1 and from days 42 to 121 in the Phase 2) and reducing the number of outbreaks of cold sores (herpes labialis) in the period from 42 to 121 days after a single dose in persons with frequent outbreaks (in the Phase 2). (These were not the planned primary endpoints in either clinical trial and the results failed to meet the planned primary endpoints in each trial.)

Squarex has booked fair market value investment of $6.5 million in equity and debt as of September 30, 2022, from investors including various individuals.

Squarex’s Market & Competition

According to a 2022 market research report by Grand View Research, the global herpes simplex market was an estimated $1.5 billion in 2021 and is forecast to reach $3.8 billion by 2030.

This represents a forecast CAGR (Compound Annual Growth Rate) of 10.81% from 2022 to 2030.

Key elements driving this expected growth are an increasing incidence of the viral infection, which can be spread via saliva, semen, vaginal secretion or idiosyncratically.

Also, the chart below shows the historical and projected future growth trajectory of the U.S. herpes simplex virus treatment market:

U.S. Herpes Simplex Market (Grand View Research)

Major competitive vendors that provide or are developing related treatments include:

-

Moderna (MRNA)

-

GSK (GSK)

-

Carlsbad Tech

-

Emcure Pharmaceuticals Ltd.

-

Glenmark Pharmaceuticals

-

Fresenius Kabi AG

-

Apotex

-

Mylan N.V.

-

Teva Pharmaceuticals Industries Ltd. (TEVA)

-

Sanofi (SNY)

-

Novartis AG (NVS)

Squarex Pharmaceutical Corporation Financial Status

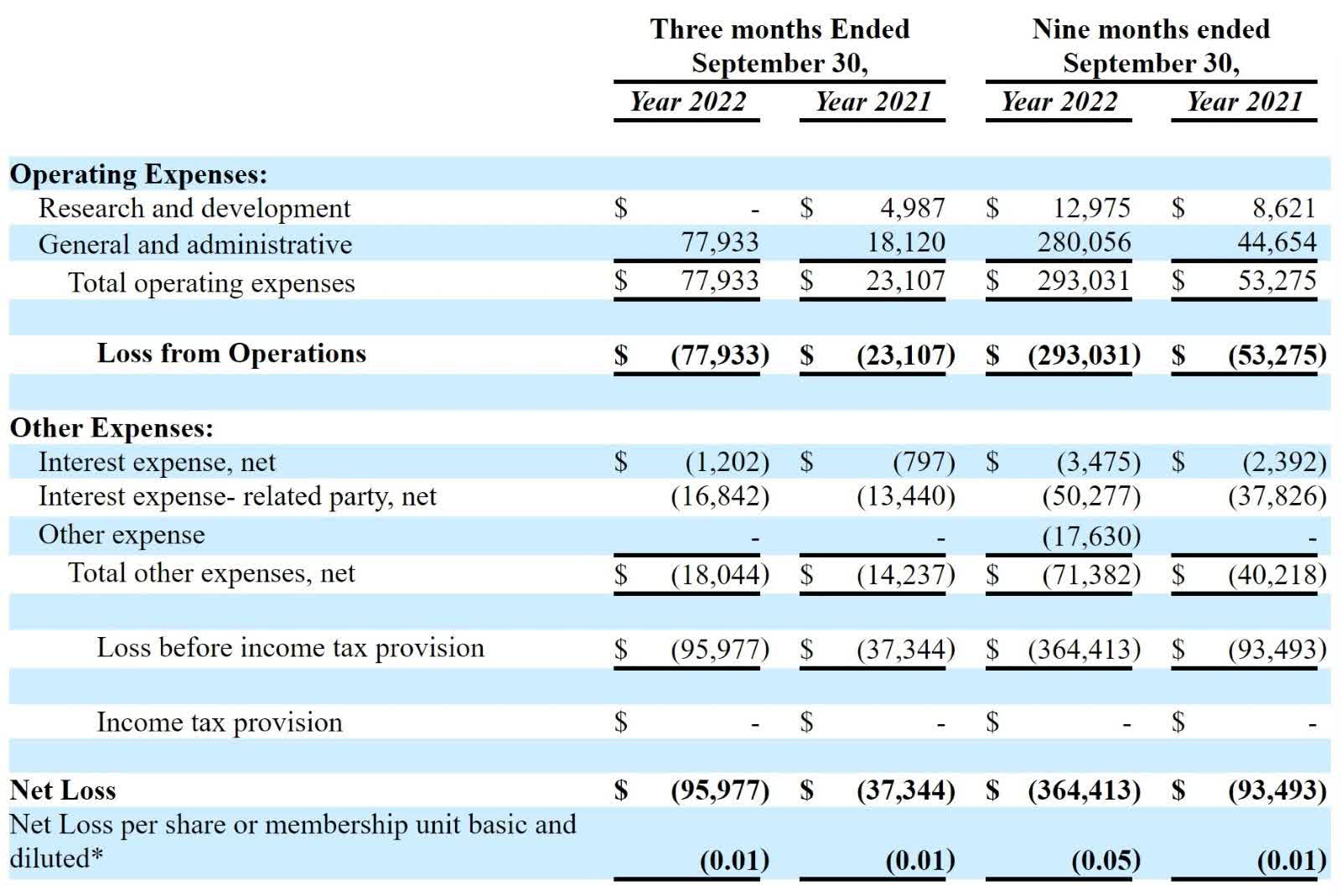

The firm’s recent financial results are typical of a clinical-stage company in that they feature no revenue and R&D and G&A expenses associated with its product development efforts.

Below are the company’s recent financial results:

Statement Of Operations (SEC)

As of September 30, 2022, the company had $8,079 in cash and $1.2 million in total liabilities.

Squarex Pharmaceutical Corporation IPO Details

Squarex intends to raise $17.8 million in gross proceeds from an IPO of its common stock, although the final figure may differ.

No existing shareholders have indicated an interest in purchasing shares at the IPO price, although this element may become a feature of the IPO if disclosed in a future filing.

Management says it will use the net proceeds from the IPO as follows:

Approximately $3,600,000 for Phase 2 clinical trial;

Approximately $540,000 for drug manufacturing and testing; and

the remainder for working capital and general corporate purposes including the associated costs of operating as a public company.

Based on our current projections, we believe the net proceeds of this offering will fund our operations for at least 12 months from the date of this prospectus.

(Source – SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management says any pending legal litigation is not material.

The sole listed bookrunner of the IPO is EF Hutton.

Commentary About Squarex’s IPO

SQRX is seeking U.S. public capital market investment to fund further trials of its drug.

The firm’s lead candidate, SQX770, has completed Phase 1 and 2 trials and management has noted statistically significant improvements in target indications.

The market opportunity for treating herpes simplex is large and expected to grow at above 10% CAGR through 2030, so the firm enjoys strong industry growth dynamics in its favor.

Management hasn’t disclosed any major pharma firm collaboration relationship.

The company’s investor syndicate doesn’t include any known institutional venture capital firms or strategic investors.

EF Hutton is the lead underwriter and IPOs led by the firm over the last 12-month period have generated an average return of negative (66.4%) since their IPO. This is a bottom-tier performance for all major underwriters during the period.

The company is still a very tiny firm with thin capitalization.

I’ll provide an update when we learn more about the IPO from management.

Expected IPO Pricing Date: To be announced.

Be the first to comment