Funtap/iStock via Getty Images

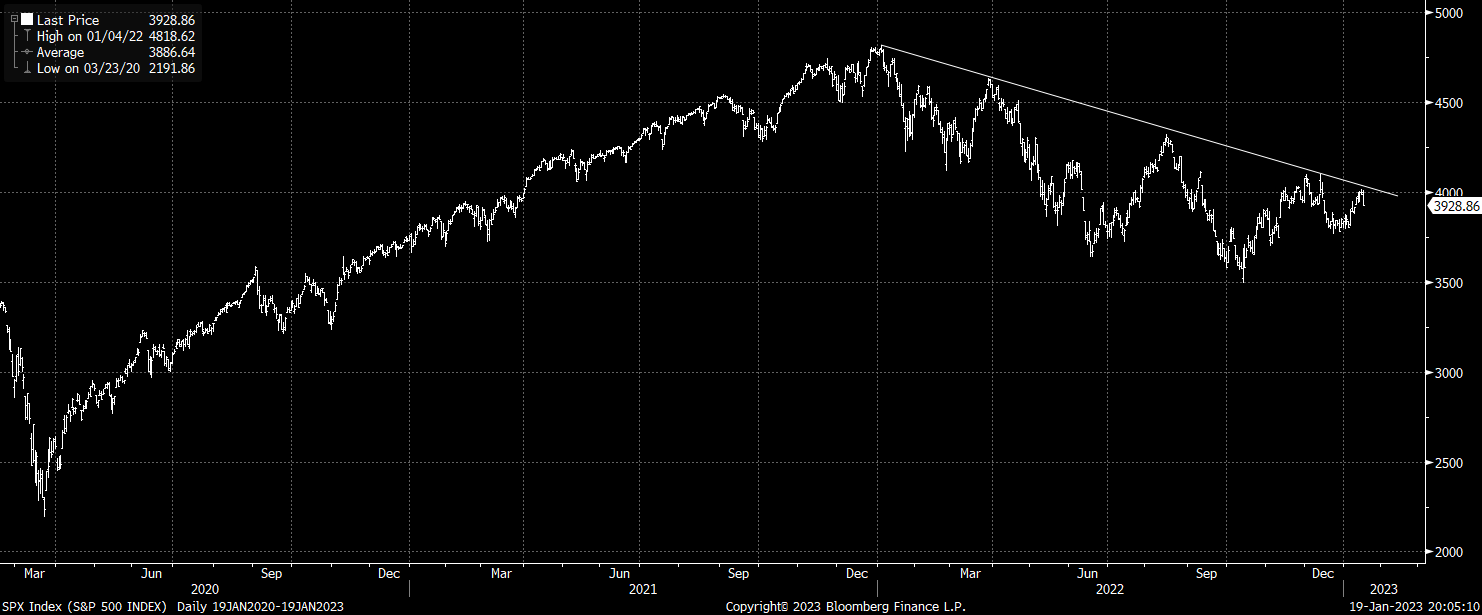

The strong close seen on Friday following the CPI report has given way to renewed selling in the SPX, and another down leg looks likely after the index failed to overcome key downtrend resistance. It is noteworthy that stocks have declined even as bond yields have fallen, which is a strong indication that markets are waking up to the weak economic outlook. This may well be the start of a major rotation out of stocks and into bonds.

SPX Just Can’t Catch A Break

I noted on January 10 that the bear market in the SPX was far from over, and that the failure to break out of the downtrend from the January 2022 kept the focus on the downside. The failure of the SPX to build on last week’s gains has once again kept this resistance level intact, and another wave of selling looks likely.

SPX Share Price (Bloomberg)

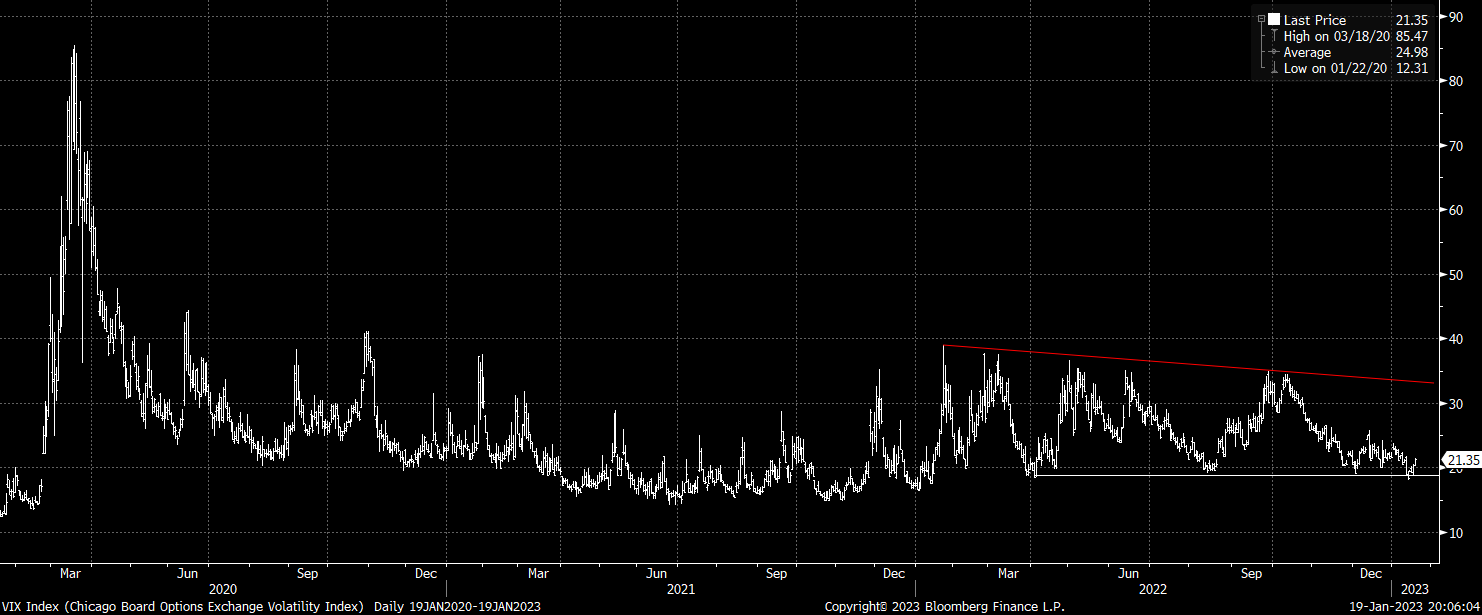

The failure of the Nasdaq to take out its own resistance level is also a negative sign as tech stocks have led on the downside during this bear market. Furthermore, the false downside break in the VIX volatility index has sent the so-called fear gauge back into its recent range.

VIX Volatility Index (Bloomberg)

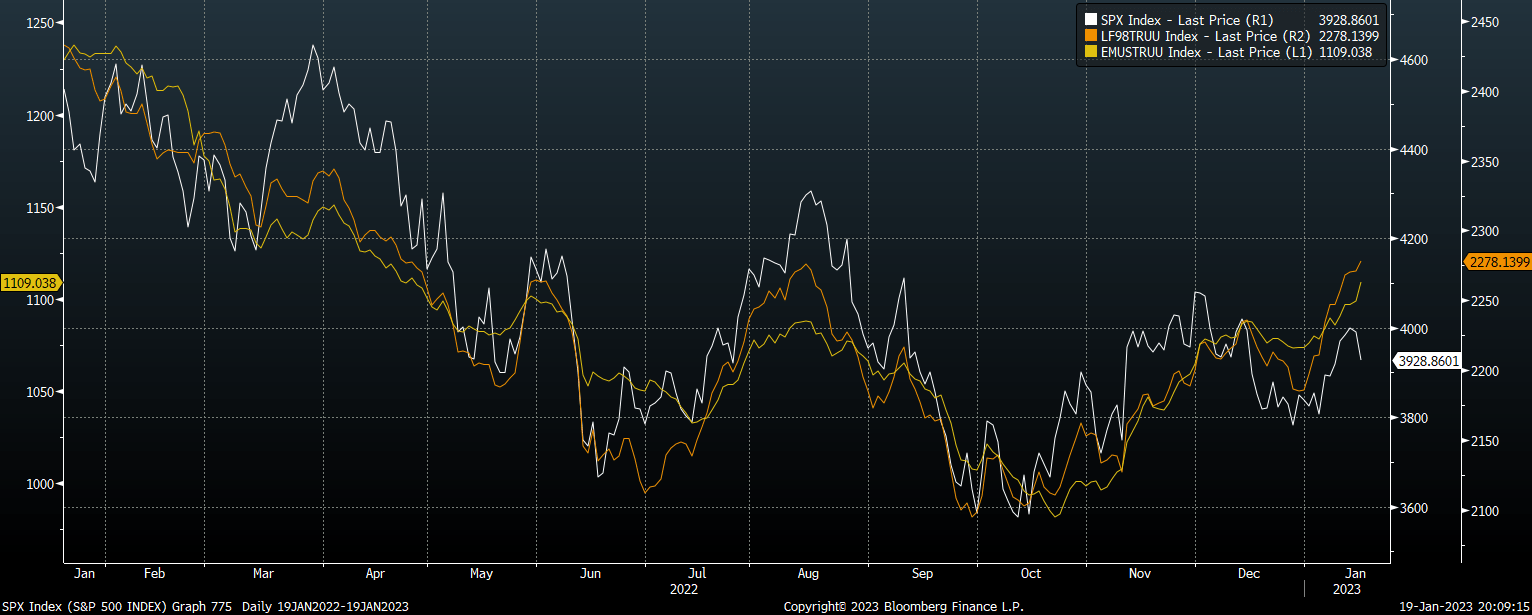

Strength In Corporate Credit At Odds With SPX Weakness

The weakness in stocks has occurred despite the strength seen in credit markets. As the chart below shows, high yield bond prices have remained firm despite renewed equity weakness, and emerging market bond prices have actually continued to rally.

SPX Vs High Yield And EM Bond Prices (Bloomberg)

Ordinarily I would say this is a net positive for the SPX as strength in high yield bonds indicates that market risk appetite remains bullish, which may translate into a recovery in stocks. However, it is equally likely that we are seeing the early signs of a broad-based shift in demand from equities to fixed income.

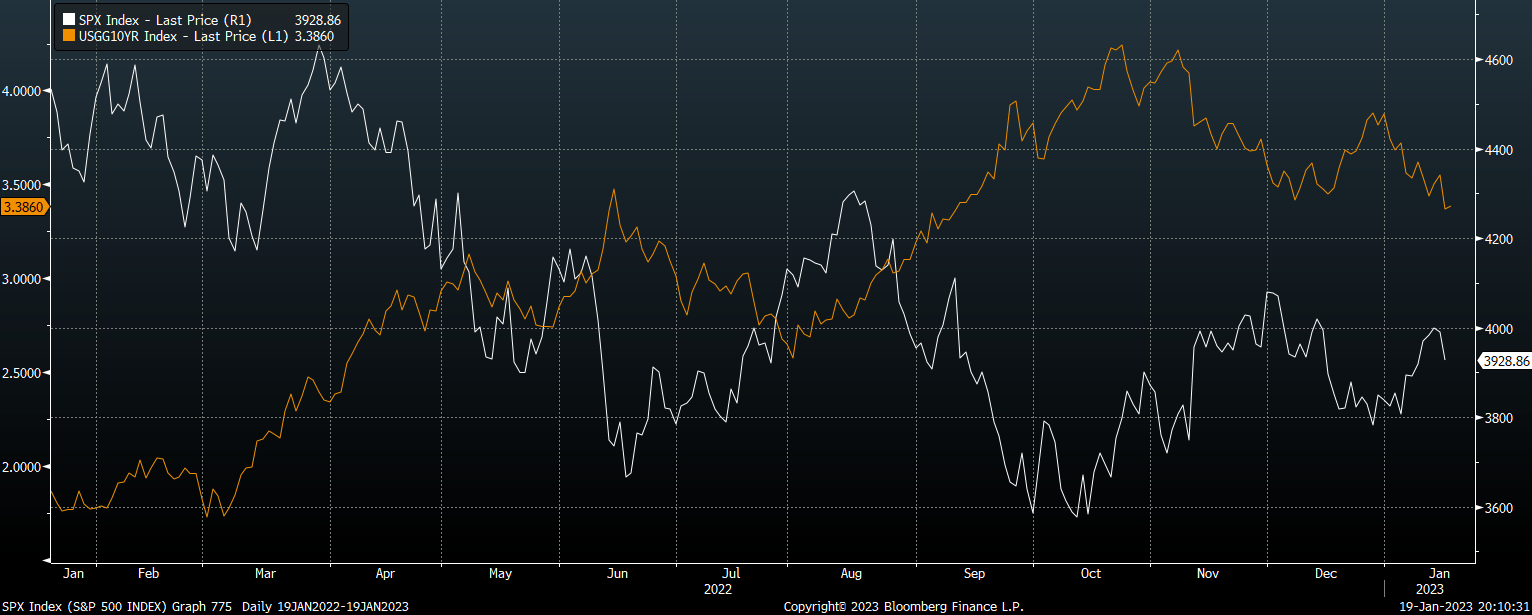

A Rotation From Stocks To Bonds As Recession Risks Rise

In stark contrast to the weakness seen in stocks for most of 2022, the declines seen in the SPX over recent days have occurred alongside a decline in US Treasury yields, which seems to reflect growing fears about the economic outlook. Lower bond yields should not be positive for stock valuations if they reflect a weakening in the growth and/or inflation outlook, and I expect to see this positive correlation between stocks and bond yields remain in place as recession fears rise. This should see stocks underperform high yield bonds as we have seen in recent sessions.

SPX Vs US 10-Year Bond Yields (Bloomberg)

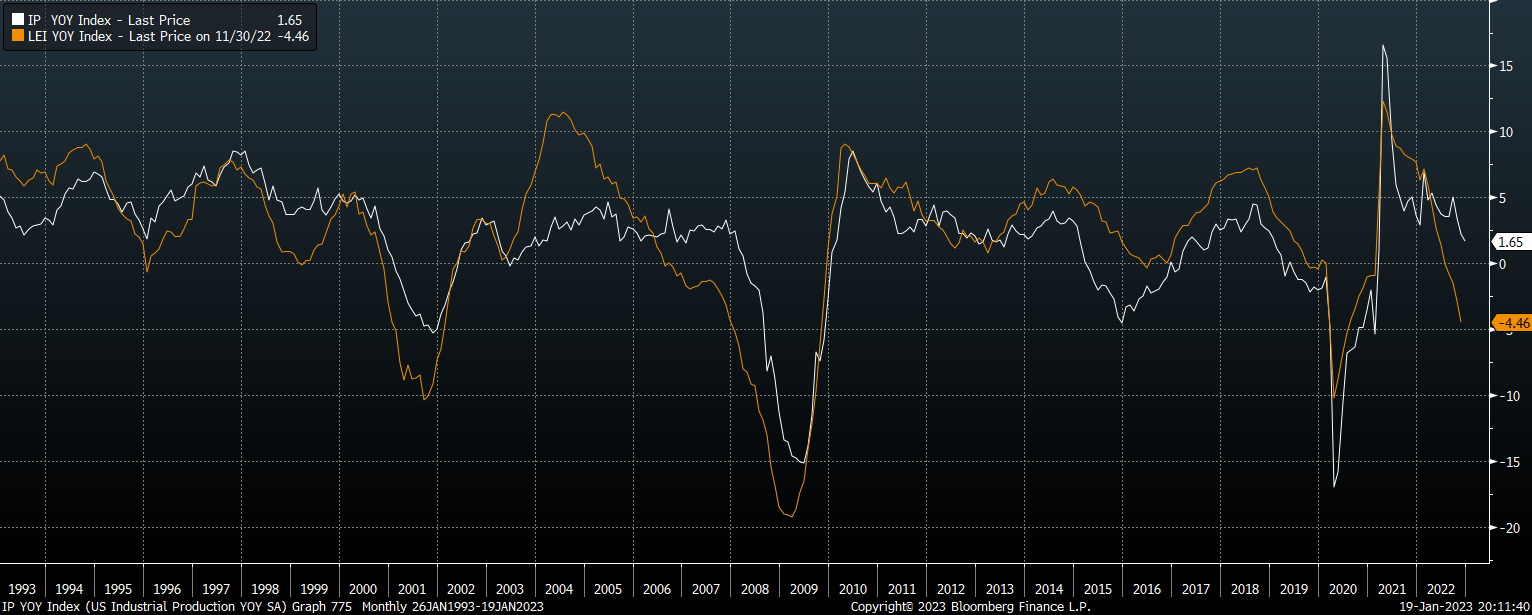

I have noted the rapid decline in leading indicators over the past few months, most important of which is the Conference Board’s leading economic indicator index, which has an excellent track record of predicting recessions. This indicator continues to move south, and at -4.4% y/y in November, it is the same level we saw in March 2020, when the Covid recession was well underway.

US Industrial Production and Leading Indicator Index (Bloomberg)

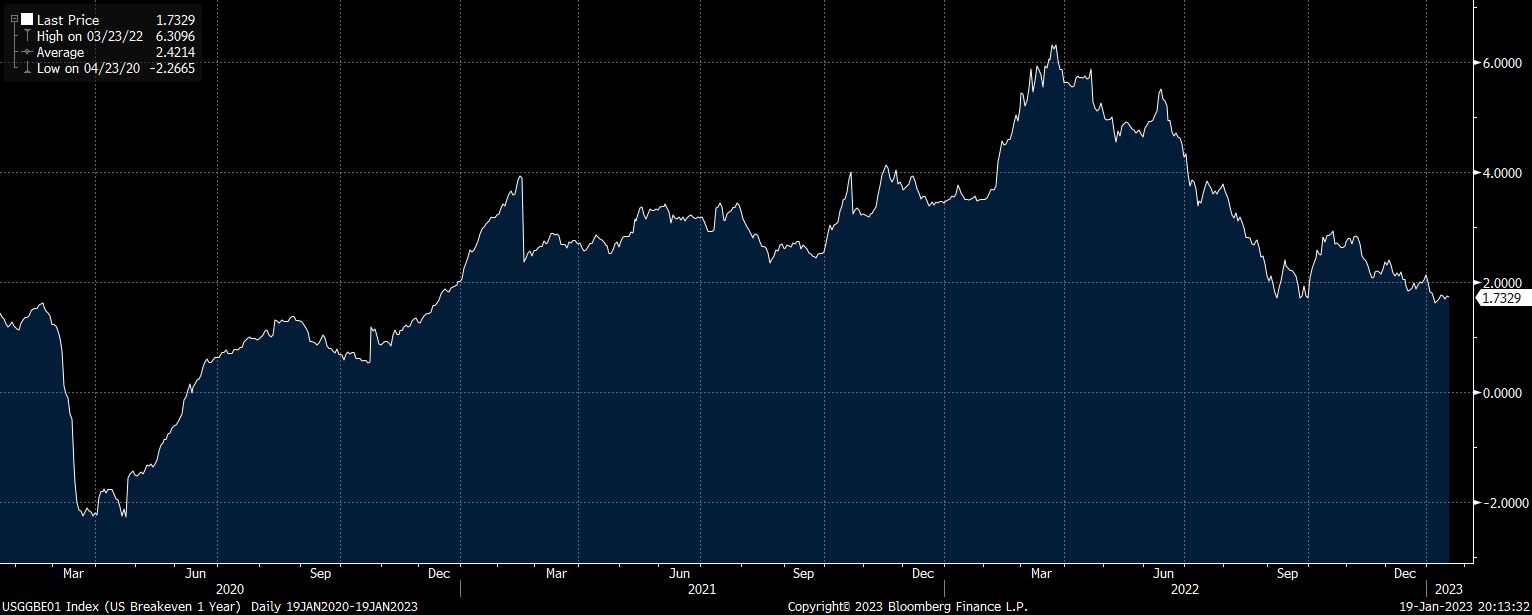

Yesterday’s industrial production release confirmed the weakness seen in the leading indicators, posting a -0.7% y/y print, while the manufacturing component fell 1.2%, and is now negative in year-over-year terms. In addition, inflation expectations as measured by the inflation-linked bond market continue to decline. The average inflation rate expected over the next 12 months is just 1.8%. While the Fed remains focused on tackling inflation, there is a growing risk of an outright decline in nominal GDP and corporate over the next 12 months, which very few appear to be anticipating.

US 1 Year Breakeven Inflation Expectations (Bloomberg)

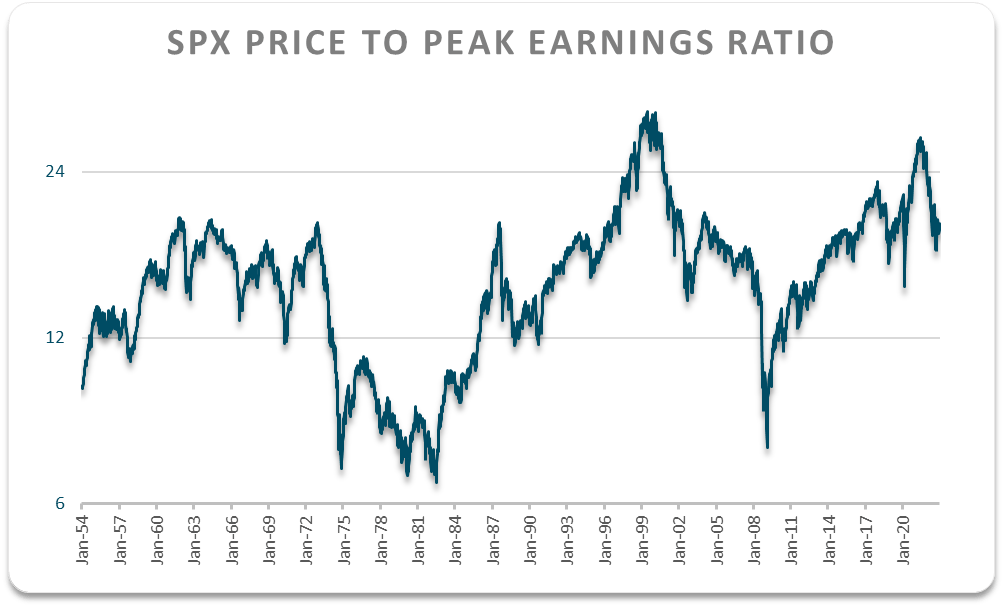

Any outright decline in SPX sales would be almost certain to result in lower earnings, as has been the case without exception across history. This would expose the extent to which stocks remain overvalued. Even at current near-record profit margins, the SPX trades at 19x earnings, which is 10% higher than the long-term median going back to 1954. If we strip out the impact of periods of declining profits by using the price-to-peak earnings ratio, the current level is more than 20% above its long-term median.

Bloomberg, Author’s calculations

Summary

The SPX looks to be embarking on another down leg after once again failing to take out downtrend resistance. Recent weakness has occurred despite a fall in bond yields, which may be a sign of the start of a rotation out of stocks and into bonds as recession risks rise. Both economic activity and inflation expectations falling fast, an outright contraction in nominal GDP and corporate sales cannot be ruled out over the next 12 months. This would expose the extent to which the SPX remains overvalued and drive a rotation out of stocks and into bonds.

Be the first to comment