Melpomenem

“Let us never negotiate out of fear. But let us never fear to negotiate.” – John Fitzgerald Kennedy

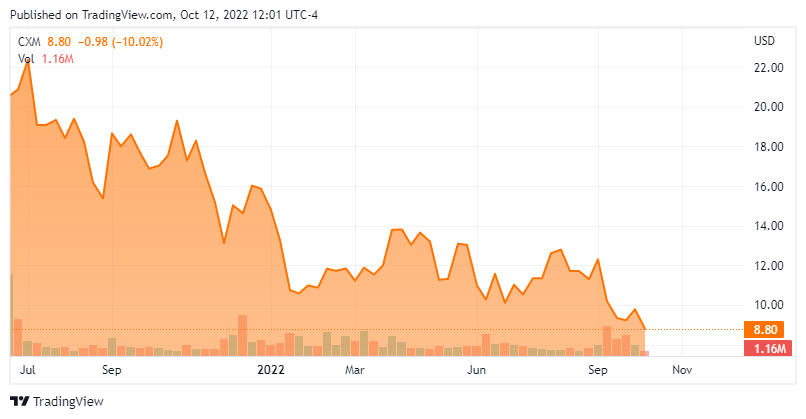

Today, we take our second look at Sprinklr, Inc. (NYSE:CXM). As you can see, this enterprise cloud software provider has quickly moved into ‘Busted IPO’ territory after going public in the second half of 2021. Since we first visited this name in late Spring of this year, the company has posted solid second quarter results. The stock is also down some 15% from where we passed on making any investment recommendation on the shares. Better results and guidance merited a further review, however. An updated analysis follows below.

Seeking Alpha

Company Overview:

June Company Presentation

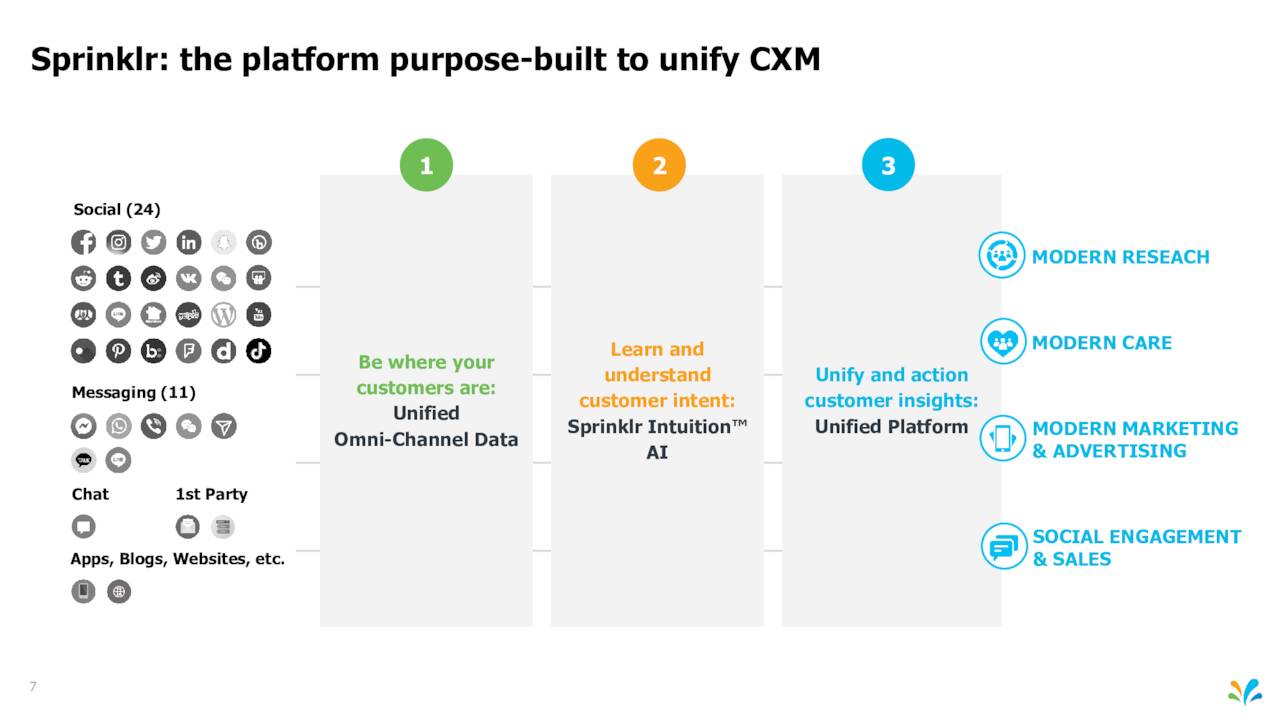

Sprinklr, Inc. is based in New York City and came public in the first half of last year. The company develops and provides enterprise cloud software products that help provide customer-based analytics across channels and integrates all stages of the customer journey. The company has two-thirds of the Fortune 100 companies on its platform. The stock currently trades at just under nine bucks a share and has an approximate market capitalization of $1.35 billion.

June Company Presentation

Second Quarter Results:

On September 9th, Sprinklr posted second quarter numbers. The company had a non-GAAP net loss of three cents a share, the consensus was expecting a six cent a share loss. Revenues rose 27% on a year-over-year basis to $150.6 million. $133.1 million of this total was from subscriptions, up 29% from 2Q2021.

During the quarter, the company grew its customers that spent at least $1 million annually to 98, a 32% increase over the same period a year ago. Management also boosted guidance slightly on its topline forward guidance and significantly on its bottom line forecast. Leadership now expects the following for this fiscal year (FY2023):

- Subscription revenue between $543 million and $547 million.

- Total revenue between $616 million and $620 million.

- Non-GAAP operating loss between $8 million and $12 million.

- Non-GAAP net loss per share between $0.06 and $0.08, assuming 261 million weighted average shares outstanding.

Analyst Commentary & Balance Sheet:

The analyst community has mixed opinions on CXM at the moment. Since second quarter results were posted, six analyst firms including BTIG and Oppenheimer have reiterated or assumed Buy or Outperform ratings on the stock. Price targets proffered range from $12 to $22 a share. Both Morgan Stanley ($14 price target, up from $12 previously) and Citigroup ($13 price target, up from $12 previously) elected to maintain Hold ratings on this equity.

Less than three percent of the current outstanding float on this equity is currently held short. Numerous insiders are frequent sellers of the stock, despite the decline in the shares. They sold nearly $2.8 million worth of shares collectively in the third quarter. No insider purchases have occurred since Sprinklr IPO’d. The company ended the second quarter with approximately $540 million of cash and marketable securities on its balance sheet against no long-term debt.

Verdict:

The current analyst consensus has the company losing seven cents a share in this fiscal year (FY2023) as revenues increase some 25% to just under $620 million. They project Sprinklr, Inc. will make a very slight profit on just over 20% sales growth in FY2024.

When we first looked at Sprinklr in June, the stock was going for just over 3.5 times forward sales equating for the net cash on the company’s balance sheet. It is now going for just under three times forward sales using the same equation.

In addition, management was forecasting a non-GAAP operating loss between $37 million and $41 million at that time which has now been reduced significantly to $8 million to $12 million. Analysts were also expecting an approximate 10 cents a share loss next fiscal year. They now project a slight profit.

Given these improvements, I am taking a small ‘watch item‘ position in CXM via covered call orders given the company’s prospects have brightened since our first piece on it.

“Where two principles really do meet which cannot be reconciled with one another, then each man declares the other a fool and a heretic” – Ludwig Wittgenstein

Be the first to comment