S&P 500 OUTLOOK:

- The S&P 500 declines and posts losses for the fourth day in a row

- Sentiment remains fragile on Wall Street as the crisis in Ukraine drags on for another day

- A retest of the 2022 low appears increasingly likely in the short term for the S&P 500

Most Read: Dow, S&P 500, Nasdaq 100 Forecasts: It’s a Mess

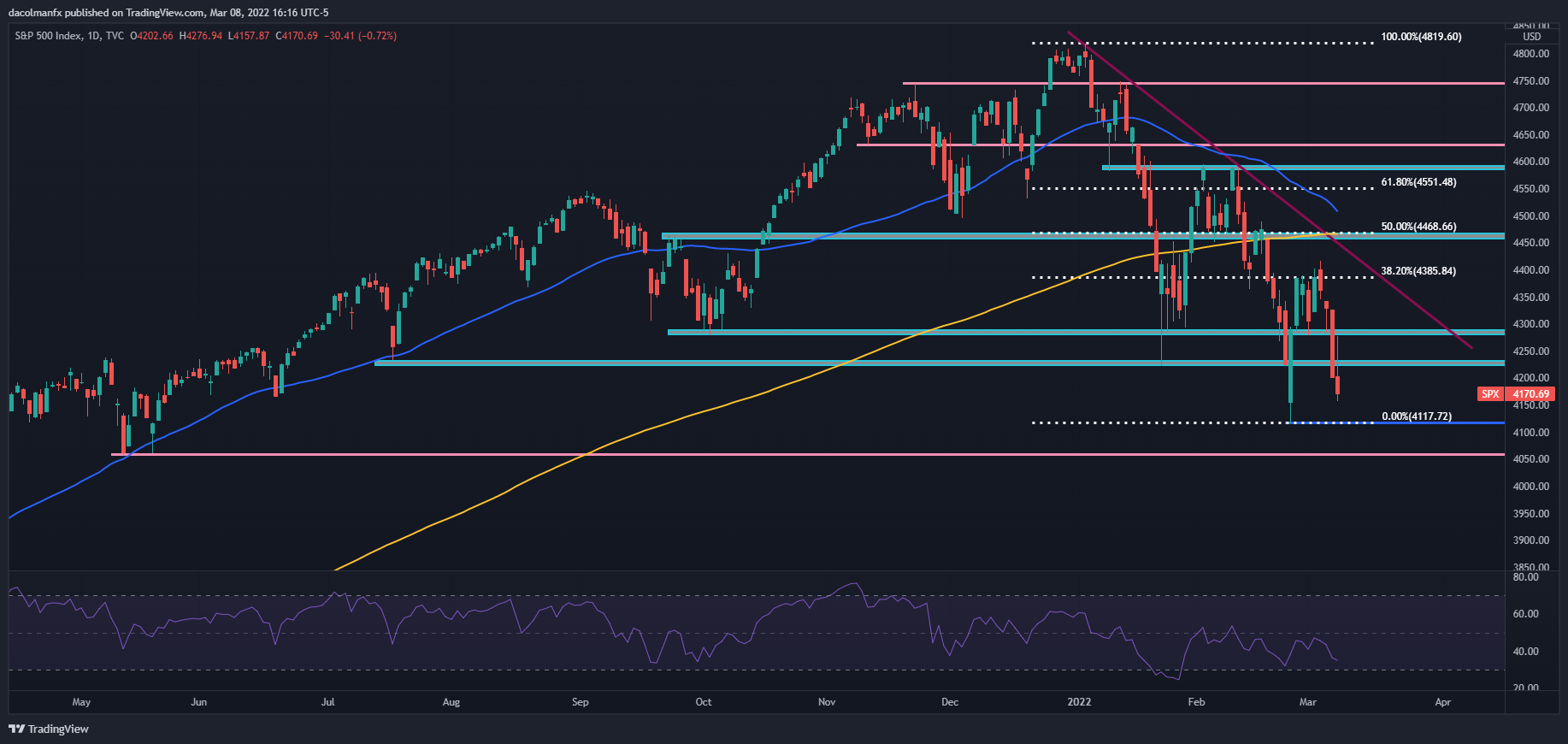

Volatility was on the menu again on Wall Street today, with sentiment all over the place and at the mercy of war-related headlines crossing the wires. To add context, S&P 500 was selling off in the morning trade amid soaring oil prices following the U.S. decision to ban Russian crude imports, but then swung up towards positive territory and exploded higher on reports that Kyiv was no longer pressing for NATO membership. However, the midday rally was clearly a dead-cat bounce as the index ended up giving up all gains to finish the day 0.72% lower at 4,170, posting losses for the fourth consecutive day.

For now, any recovery in the equity space may not gain traction if geopolitical risks stay elevated. At this point, there is no evidence to argue that there is a path to reach a détente in the ongoing conflict in Eastern Europe. In fact, it is increasingly likely that President Putin will stay the course until he fully captures Ukraine, to avoid losing face at home and enduring harsh criticism for a horribly executed military operation that will only bring economic misery to the Russian people.

Focusing on economic links, U.S. companies have very low revenue exposure to both Russia and Ukraine, so this is obviously not the reason why stocks have fallen dramatically in recent weeks. The problem stems from the price shock in the commodity market. After the West imposed heavy sanctions on Moscow for invading a sovereign country, raw material prices surged on supply flow disruptions, with crude oil (Brent) and wheat (US) up roughly 35% and 45% respectively in the last two weeks.

Soaring commodity prices will exacerbate inflationary pressures at a time when headline CPI is already at the highest level in four decades in the U.S. (7.5% year-on-year in January). Red-hot inflation will weigh on consumer confidence, erode business margins and lead the Fed to raise interest rates numerous times in 2022, setting the stage for slower economic growth. Justified or not, this combination of circumstances is stoking fears of stagflation among investors, sparking risk-off episodes on and off.

With volatility elevated across asset classes, the flattening of the Treasury curve, and the outlook subject to extraordinary uncertainty amid growing geopolitical headwinds, sentiment will remain fragile and cautious in the days and weeks ahead, preventing a sustained and meaningful rebound in stocks at the index level. As things stand, dip buyers may choose to stay on the sidelines and investors may be reluctant to increase their equity exposure, especially if the market continues to behave erratically and moves violently on war-related news.

For the reasons mentioned before, I would not rule out the S&P 500 retesting this year’s low soon. Short-term traders should be careful here because if this support does not hold, selling momentum could accelerate, exposing the May 2021 low near the 4,050 area.

On the other hand, if buyers return and retake control of the market, resistance lies at 4,225 and then at 4,285. If the index manages to clear these hurdles, the 38.2% Fibonacci retracement of the 2022 decline near the 4,385 area would become the next upside target.

S&P 500 TECHNICAL CHART

{kind=link}

S&P 500 (SPX) Chart by TradingView

EDUCATION TOOLS FOR TRADERS

- Are you just getting started? Download the beginners’ guide for FX traders

- Would you like to know more about your trading personality? Take the DailyFX quiz and find out

- IG’s client positioning data provides valuable information on market sentiment. Get your free guide on how to use this powerful trading indicator here.

—Written by Diego Colman, Contributor

Be the first to comment