Sundry Photography/iStock Editorial via Getty Images

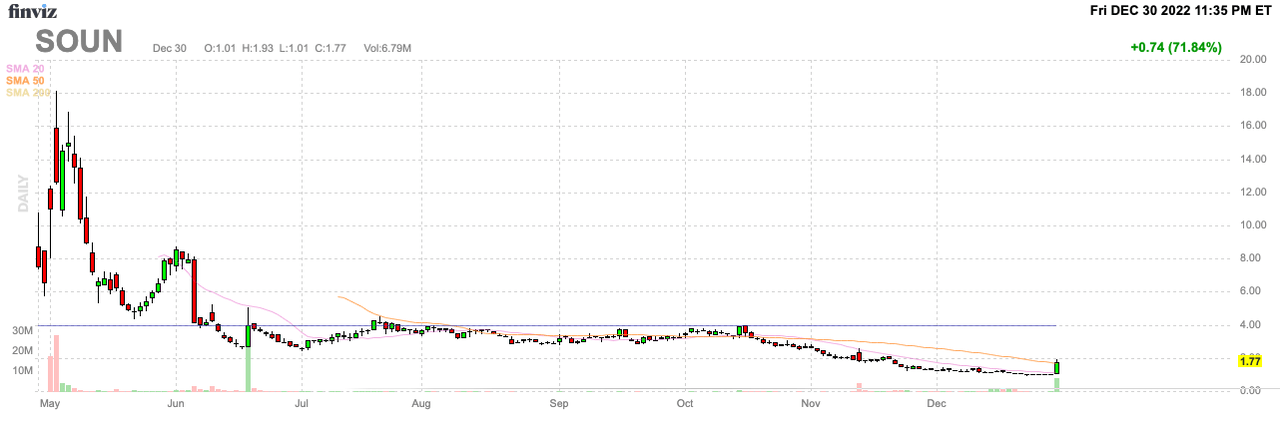

As with a lot of SPACs in 2022, SoundHound AI (NASDAQ:SOUN) appears to have collapsed to $1 irrespectively of their results. The custom voice AI company has solid financials for a small company, yet the market has no interest at the moment investing in a growth story. My investment thesis is Bullish on the stock trading close to $2 after a big rally to end the year, though shareholder dilution is a big headwind.

Source: FinViz

Undeniable Market Opportunity

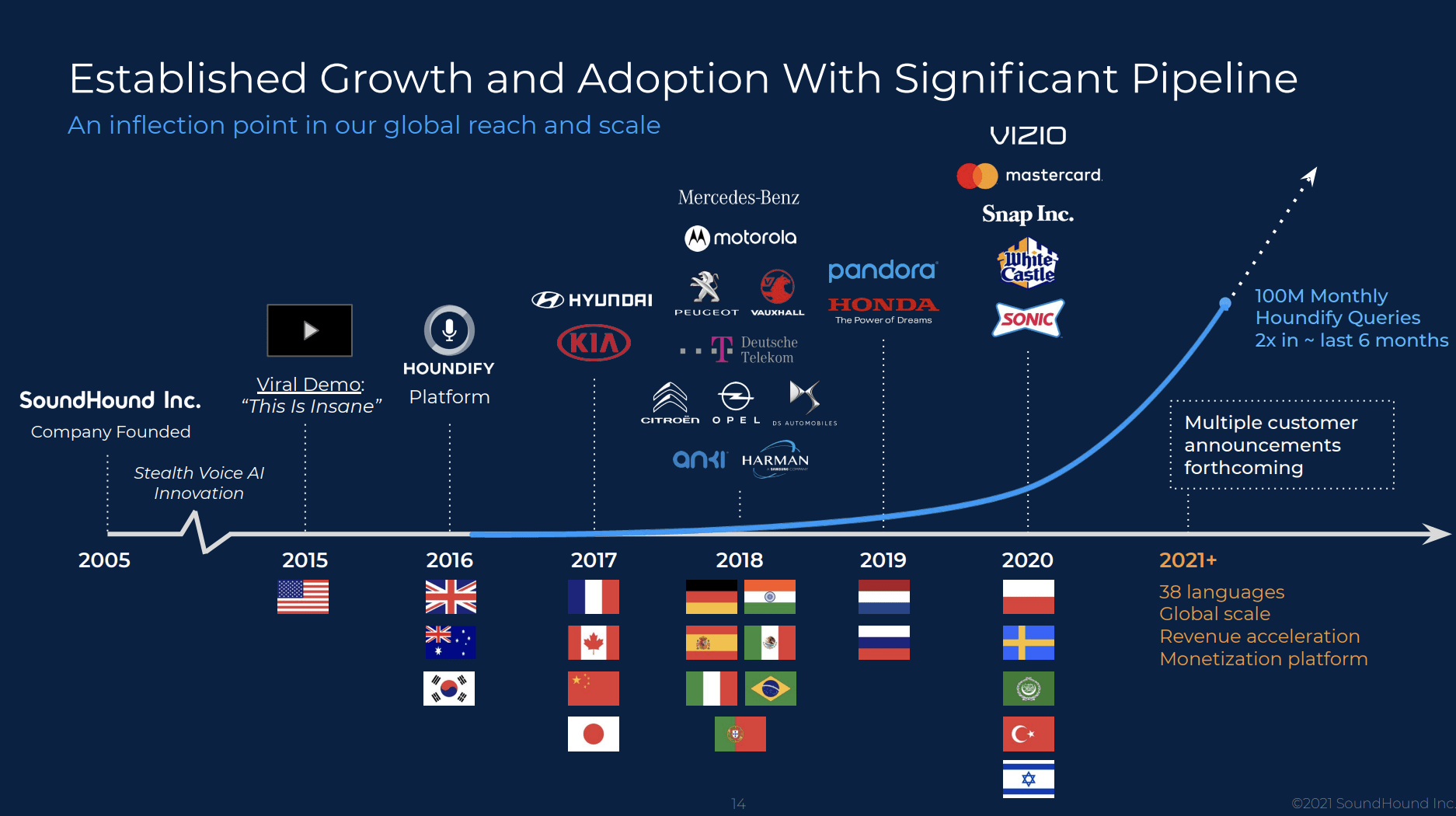

SoundHound AI has been around for years, with a viral YouTube video going back to 2015. The big question is whether the company can outflank the tech giants in voice AI.

The voice AI market opportunity reaches $160 billion and SoundHound has a strong customer base working with the likes of Snap (SNAP), Mastercard (MA) and Vizio (VZIO). Along with the Q3 earnings, the company outlined relationships with 17 automotive brands in the strong sign of how corporations want to work with independent technology solutions over offerings from big tech.

Source: SoundHound SPAC presentation

The SoundHound for Restaurants product is on the path to order completion exceeding human levels due to advanced AI technology. Companies from Toast (TOST) to Square (SQ) are working with SoundHound on these technologies for improving food orders.

The company recently released Dynamic Interaction to further take conversational AI to the next level. This AI technology allows for instant responses improving order taking and other opportunities due to faster responses versus prior technology focused on “taking-turns”.

Impressive Financial Start

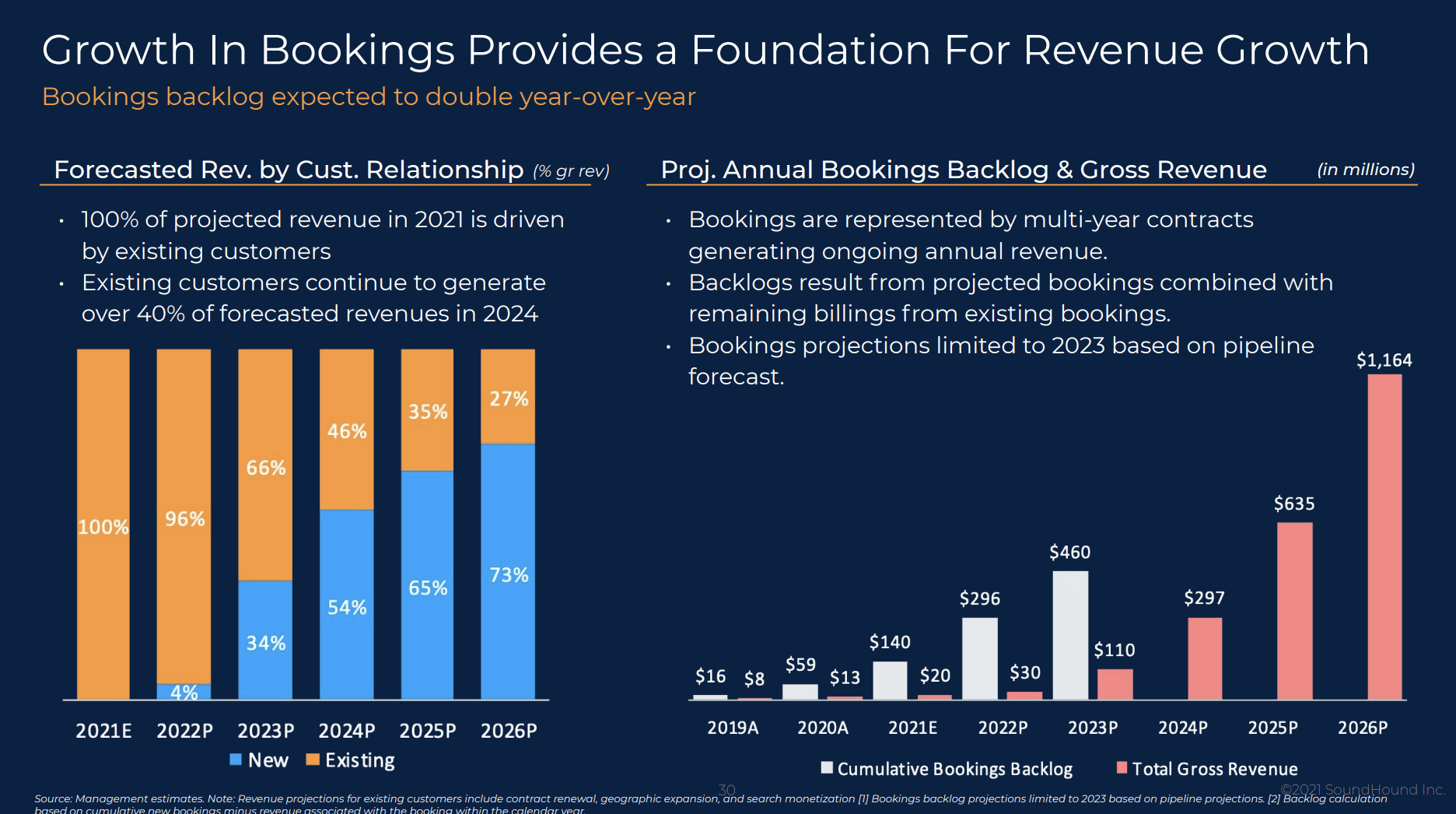

At $1, the market cap had fallen all the way down to $200 million. SoundHound ended Q3’22 with a record bookings backlog of $302 million with a five-year weighted average contract length. The backlog grew from $283 million in the prior quarter, and the restaurant business is only now launching with new customers.

The AI company even reported a record quarterly revenue of $11 million, up 178% YoY. The prior peak was $6 million just back in Q2, with the annual revenue target forecasting $7 million to $11 million in Q4 after a large deal in Q3 boosted revenues.

Just as impressive, SoundHound already has gross margins of 77% providing the gross profits to quickly cover a lot of spending. A lot of the worse SPACs are the companies not even generating a positive margin, leaving the company far away from any scenario where a profit is possible.

At the time of the SPAC deal last year, SoundHound forecast a bookings backlog for 2023 of only $296 million. The company has already topped this figure by $6 million.

Source: SoundHound SPAC presentation

Based on Q3 revenues nearly doubling the prior quarter levels of $6 million, SoundHound would appear on the path to strong revenue growth in 2023. The company originally targeted revenues of $110 million while analysts only forecast revenues of $64 million now, though the voice AI company has limited analyst coverage.

This stock market doesn’t like that SoundHound posted an adjusted EBITDA loss of $17 million, up from $15 million last Q3, but the voice AI company is still in growth mode. Unfortunately, SoundHound was recently required to cut expenses by 10% to conserve cash in a tough macro environment when investing should be the only goal.

Though, the biggest issue with SoundHound was the inability to raise additional funds with the SPAC. The company only has a cash balance of $33 million to end the September quarter.

On the Q3’22 earnings call, CFO Nitesh Sharan outlined the cash position and capital raising plans going forward:

Our cash position at quarter end was $33.4 million. We continue to leverage the proceeds we received from going public in April while continuing to infuse new capital. For example, in Q3, we added a new committed equity line of credit, which once available we expect will provide ongoing access to incremental capital to help us continue to fuel growth. In addition, we are currently in late stage discussions to provide additional more immediate cash to the balance sheet.

Despite all of the exciting aspects of the business, SoundHound needs access to more capital while the stock trades in the $1s. The equity line of credit with CF Principal Investments LLC of $25 million will help fund investments, but the company won’t avoid shareholder dilution. Unfortunately, the company will definitely want to raise additional funds in the next year to fund the ongoing substantial EBITDA losses.

Takeaway

The key investor takeaway is that SoundHound is definitely a very speculative investment. The market doesn’t like SPACs providing the opportunity to invest in a promising voice AI company with a large backlog on the cheap. Even with the rally today, the market cap is hardly above the $300 million bookings backlog here. Considering the large EBITDA losses, investors have to understand the risk of loss in a such an investment, but the rewards clearly exceed the risks here.

Be the first to comment