Sundry Photography

The SoundHound AI (NASDAQ:SOUN) rally in early 2023 wasn’t surprising, though the magnitude of the AI hype has been a shock. The company entered 2023 with a strong order backlog ignored by the stock market due to large operating losses. My investment thesis is now Sell on the AI voice company with SoundHound AI trading at $4.

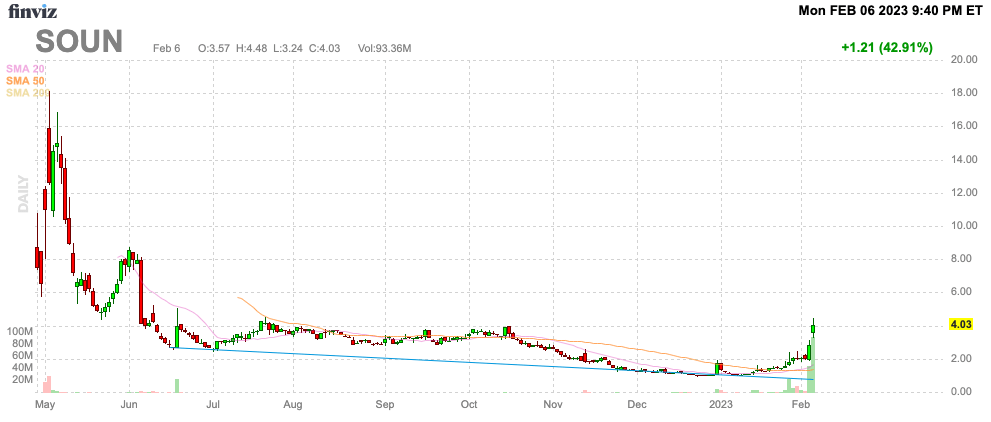

Source: Finviz

AI Surge

Due to the ChatGPT phenomenon, any business focused on AI has seen some big stock gains this year. SoundHound AI is no exception with the stock trading below $1 in December and topping $4 to start February.

As an example, C3.ai (AI) has rallied ~150% since the start of the year after losing 90% since the peak. Neither company has announced anything warranting large stock rallies other than having “AI” in their name.

Oddly, SoundHound AI announced a major restructuring of the business to focus on existing AI voice verticals like restaurants, smart devices and automotive. The company cut costs by reducing investments in new verticals to reduce costs by up to 40% without a big hit to near-term revenue growth, or the impressive $300+ million backlog.

While SoundHound AI reported impressive growth in Q3, the company only generated meager revenues of $11.2 million while total operating expenses were $27.0 million. The adjusted EBITDA loss was only $16.9 million, but the AI voice company reported a loss in excess of the revenue level despite 77% gross margins.

The company targeted a $60 million reduction in annual operating costs, though the guidance isn’t specific on the inclusion of stock-based compensation. The Q3’22 total GAAP operating expenses were $38.2 million, or slightly above $152 million on an annual basis. A 40% cut to these expenses amounts to a $60 million reduction in operating expenses.

What ultimately matters is the ability of SoundHound to become adjusted EBITDA profitable. The $60 million cut eliminates ~$15 million in quarterly operating expenses, but a big question is how much of these expense reductions are tied to the $9 million spent on SBC in Q3 that isn’t included in the EBITDA loss.

Focus On Key Markets

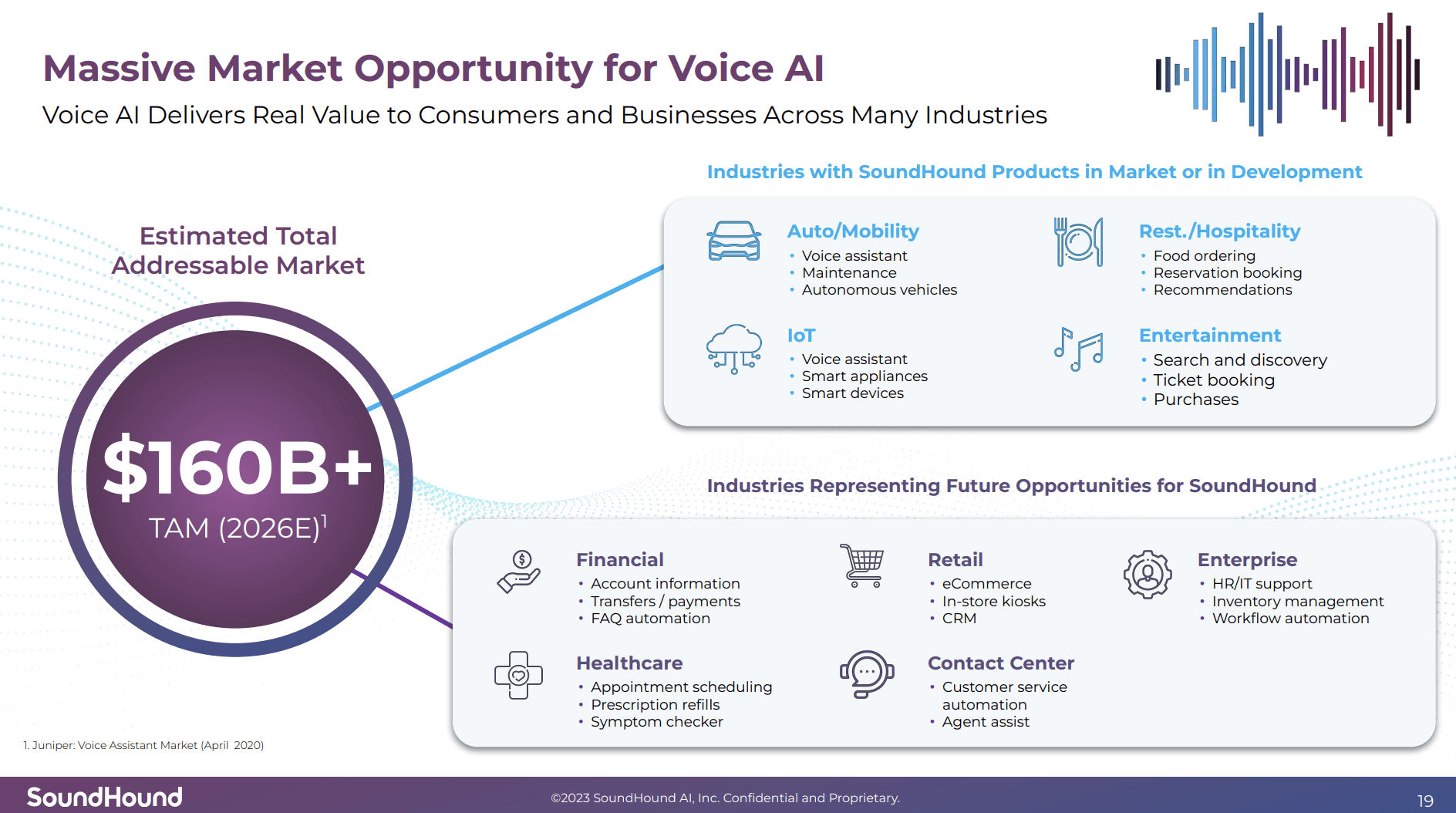

The downside of cutting off development on new verticals is that SoundHound AI reduces some of the long-term upside. The good news is that the Voice AI market is massive and the company is probably far wiser to focus on a few key verticals.

Source: SoundHound AI Jan. ’23 presentation

The company already has massive potential in auto and restaurants to not overextend in other areas. SoundHound recently had to raise $25 million via a convertible debt offering highlighting the better option to focus on verticals providing profitable growth for now in order to avoid additional dilution with the stock trading this low.

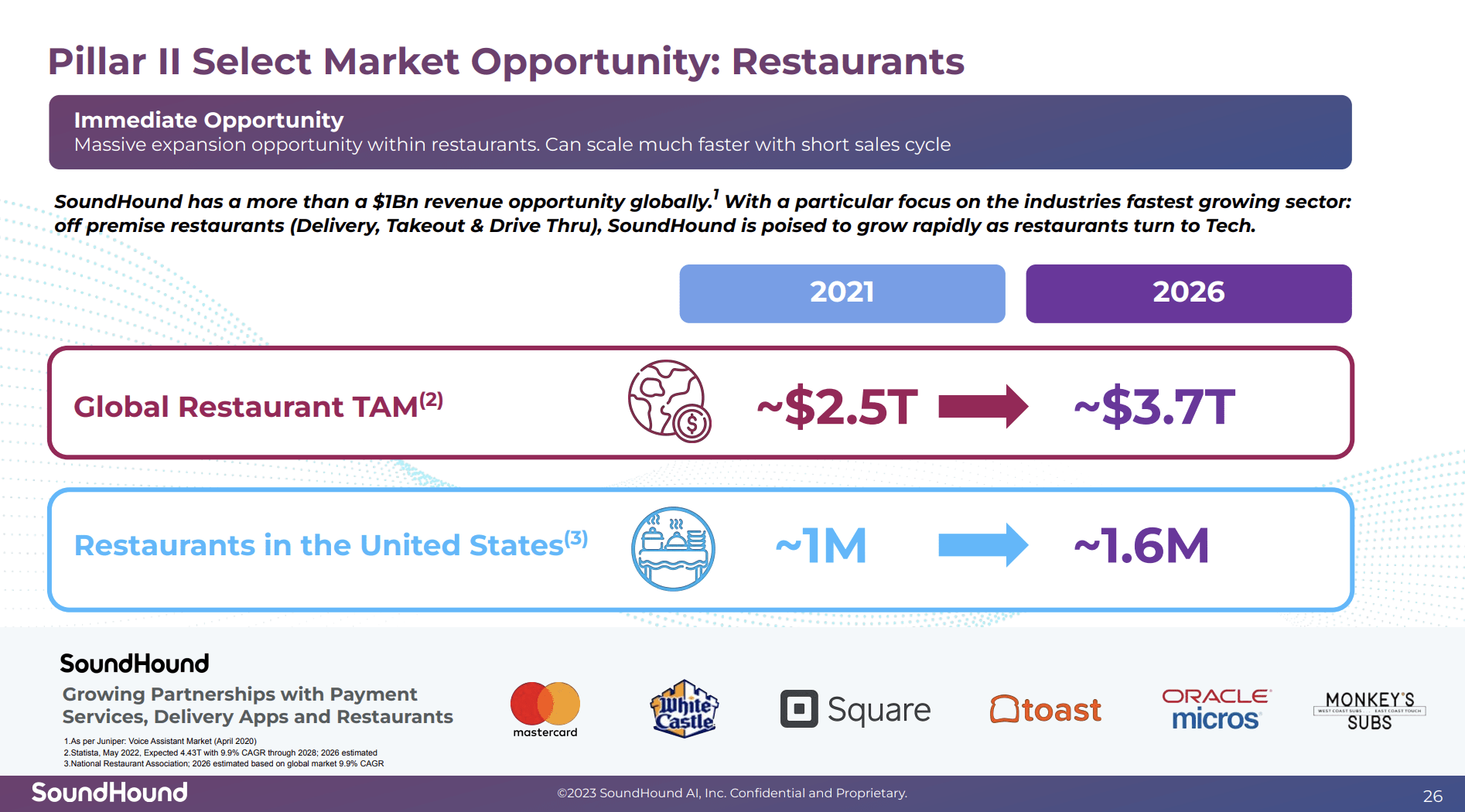

SoundHound predicts the restaurant vertical alone offers a $1+ billion annual revenue opportunity. The company has already shown voice AI products that improve the ordering process and reduce the need for employees in time when worker costs have soared.

Source: SoundHound AI Jan. ’23 presentation

The AI stock rally has greatly changed the valuation equation for SoundHound AI. The stock is now worth over $800 million and the guidance for only 50% revenue growth isn’t impressive enough for the current valuation.

The company hopes to be cash flow positive by Q4’23, but the 2023 revenue target of $50+ million isn’t impressive for the current stock value. SoundHound AI already has a net debt position and the recent $25 million preferred stock offering could quickly convert into 20% of the outstanding shares in a very expensive fundraising days before the stock more than doubled.

Takeaway

The key investor takeaway is that SoundHound AI has quickly gone from beaten-down SPAC to speculative AI play. Investors following the previous Buy recommendation can now Sell for a quick profit and wait for a better re-entry point. The stock could easily rally even more, but SoundHound is definitely expensive now trading at up to 16x sales targets.

Be the first to comment