Alex Wong/Getty Images News

Investment thesis

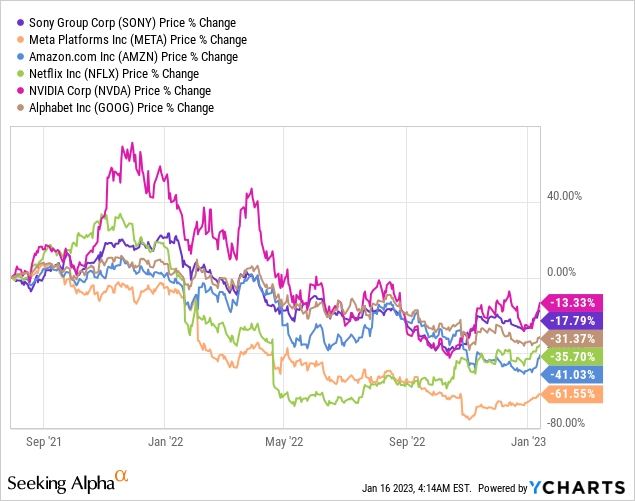

Sony’s (NYSE:SONY) shares have outperformed the majority of its high-growth tech peers, but the slowdown in gaming has been a negative surprise. The outlook longer term remains positive, with its competitive positioning in digital content and market expansion into EVs. We reiterate our buy rating.

Quick primer

Sony is a provider of digital entertainment, consumer electronics, specialty hardware, and financial services (a domestic life insurance business). The company fully consolidated its financial services (Sony Financial) business in FY3/2021. Assets in its equity portfolio include a 58.7% stake in M3 (OTCPK:MTHRY), a 5% stake in Bilibili (BILI), a 100% stake in game developer Bungie (acquired in July 2022), and an undisclosed minority stake in the game software publisher Epic Games.

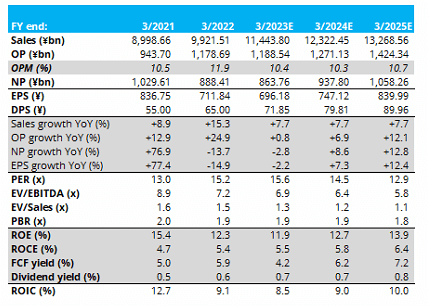

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

Our objectives

We update our view on Sony from August 2021 where we made comparisons with the Big Tech names and rated the shares as a buy on valuation grounds. The result is mixed, as Sony’s shares have outperformed but have fallen on the back of weakness in the Game & Network Services division (called G&NS).

Current air pockets in underlying growth

Despite a weak Japanese yen, Q1-2 FY3/2023 results were disappointing with sales growing only 1% YoY under constant currencies (page 2). Operating margins declined from 13.4% to 12.5%, with operating profits at the key G&NS division falling 40.5% YoY. This weakness has been due to 1) post-pandemic user behavior as gamers started to pursue other activities, as seen in falling MAU (monthly active user) data in the PS Plus online service, and 2) lower-than-expected sales of third-party software titles for the PlayStation 5, despite some major releases such as ‘Call of Duty: Modern Warfare II’ by Activision Blizzard (ATVI).

On a positive note, the Music division performed strongly with Q1-2 FY3/2023 operating profit growing 34% YoY, driven by subscription streaming services. Imaging & Sensing Solutions saw strong sales growth of 28.0% YoY (underlying 10.5% YoY adjusted for FX), but a continued focus on increasing production capacity for smartphone image sensors, as well as R&D for automotive sensors (with the EV partnership with Honda (HMC) called AFEELA), led to profitability decline YoY.

The overall picture for FY3/2023 is flattish earnings growth YoY. Whilst this is not hugely exciting, the various businesses remain relatively stable overall. Sony continues its share buyback program (2.02% of shares outstanding), and although the dividend yield remains low, Sony looks set to continue generating corporate value.

Long-term outlook remains positive

Given the quality franchises that the company operates, the outlook for earnings continues to look stable. As hit-driven businesses, there will be an element of volatility in the earnings profile. But exposure to a growing addressable market in electronic entertainment and digital content, both Music and G&NS divisions should provide future growth. In retrospect, a post-COVID hiatus in the gaming industry was to be expected and not an indication of a business in decline.

Imaging & Sensing Solutions is a relatively new business for Sony, as it pivoted from pushing its digital camera business towards high-end image sensors. Although this business requires significant R&D investment as well as being capex intensive, there is a strong fit to Sony’s legacy in consumer electronics and the new initiative in the EV market. Plans with Honda remain light on detail but the idea is to release an EV in CY2025 (page 58), although, at the CES2023 event, there were doubts over this as pre-orders are expected to be taken that year as opposed to delivery. Sony’s role is likely to be more of a Tier 1 supplier as opposed to it becoming a fully-fledged auto OEM (with low margins), although the partnership structure is a 50:50 joint venture.

Consensus forecasts (see Key financials above) expect a steady earnings growth profile for the next two financial years. This level of growth looks within a reasonable range and is not optimistic. Although Sony cannot be classified as a growth tech stock, it is a quality franchise with room for upside potential.

Valuation

On consensus forecasts, the shares are trading on PER FY3/2024 14.5x and a free cash flow yield of 6.2%. These are not demanding valuations, and we feel has priced in current weakness in recent trading.

Risks

Upside risk comes from third-party game software titles performing above expectations in early CY2023. These include Capcom’s (OTCPK:CCOEY) ‘Resident Evil 4’ remake in March 2023, and ‘Final Fantasy XVI’ by Square Enix (OTCPK:SQNXF) in June 2023.

Greater visibility for Sony’s role as a potential tier 1 supplier to the EV auto industry could open up a major new addressable market, although there is a danger over low returns compared to its content-focused business activities.

Downside risk is from continued softness in the gaming division, with the PlayStation 5 platform requiring more time for major first-party titles to renew interest levels (Spider-Man 2 is slated for a December 2023 release).

A major business expansion into the automotive components industry could require major capex for in-house manufacturing, which could cloud over free cash flow potential for the medium term.

Conclusion

Sony appears to be managing the post-COVID world adequately, although the slowdown in games may have come as a negative surprise. The company’s key competitive positioning in digital content and optical sensors remain intact, and the longer-term outlook for these two key markets remains favorable. Entry into automotive will have to be managed well in order not to lower profitability and use excessive capital, but current management appears to have a limited appetite for going all-out as a high-volume hardware manufacturer, we remain bullish on the shares and reiterate our buy rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment