monsitj

Dear Partners and Friends,

Our partnership recorded a gain of +27.0% net of all fees, expenses, and allocations for the quarter ending September 30, 2023. Over the same period, the S&P 500 recorded a loss of -3.3% including dividends.

|

Period1 |

Partnership Returns1,2 |

S&P 500 Returns1,3 |

|

Q3 2021 |

9.5% |

(0.9%) |

|

Q4 2021 |

13.5% |

11.0% |

|

2021 |

24.5% |

10.0% |

|

Q1 2022 |

(1.3%) |

(4.6%) |

|

Q2 2022 |

(18.9%) |

(16.1%) |

|

Q3 2022 |

(12.8%) |

(4.9%) |

|

Q4 2022 |

18.8% |

7.6% |

|

2022 |

(17.0% ) |

(18.1% ) |

|

Q1 2023 |

7.8% |

7.5% |

|

Q2 2023 |

17.1% |

8.7% |

|

Q3 2023 |

27.0% |

(3.3%) |

|

2023 |

60.3% |

13.1% |

|

Annualized Return Since Inception |

25.9% |

0.9% |

|

Cumulative Return Since Inception |

65.8% |

1.9% |

The below table highlights the partnership’s key portfolio composition metrics as of September 30, 2023:

|

Key Portfolio Composition Metrics4 |

|||

|

Number of Holdings: |

13 |

Average Market Cap5: |

$319MM |

|

Top 5 Holdings Concentration: |

61.6% |

Investments Non-U.S.6: |

74.2% |

|

1Sohra Peak Capital Partners LP launched July 22, 2021; results for the Partnership and S&P 500 Index for Q3 2021 are presented from that date forth. 2Returns are presented on an unaudited basis for a theoretical Limited Partner net of expenses, 1% management fee, and 15% performance allocation. 3S&P 500 Index returns include dividends reinvested. Please refer to the disclaimer at the end of this letter regarding comparison to indices. 4Metrics reported in this table exclude short and derivative positions held by the fund intended as market or position-specific hedges. 5Calculated as the median market capitalization in USD among our portfolio holdings. Excludes cash. 6Measured as the percentage of portfolio assets, excluding cash, invested in companies with primary operations conducted outside of the U.S. Please see important footnotes to the above tables under the “Disclaimer” section at the end of this letter. |

Our partnership performed quite well this quarter on both an absolute and a relative basis. As our readers know, our sole objective at Sohra Peak is to compound our partnership’s capital at the highest rate of return responsibly possible. In order to accomplish this objective, we relentlessly seek out exceptionally mispriced equities within the small-cap and micro-cap segments of the market across the developed world. I am happy to report that our investments delivered against our partnership’s objective these past several months in a big way.

Since inception, our results so far have corroborated our longstanding belief that deep structural inefficiencies exist within our investible universe, as well as our confidence in our perceived ability to identify mispriced securities within this universe with decent accuracy. We remain tireless in our pursuit of unearthing compelling investment opportunities, which this quarter has yielded new holdings, and we look forward to continuing to execute upon our partnership’s guiding objective for years to come.

While a +27.0% gain would represent a terrific year, let alone a quarter, we remain humble, realistic, and focused on the long-term performance of our individual holdings and our collective portfolio. We regularly review our holdings accordingly in a disciplined fashion.

As always, I would like to extend a thank you to all of our outstanding limited partners, including those of you who have recently joined our partnership, for your steadfast commitment and trust. For prospective partners wishing to learn more, we are currently open to new introductions.

Trip to Australia

In October, I spent 10 days traveling through Australia’s cities Perth and Sydney to conduct primary research on two of our partnership’s holdings, Mader Group (OTCPK:MADGF) and Duratec. The purpose of this trip was to confirm or disconfirm existing hypotheses held for each company, to gain a more granular understanding of each company’s business model, and to uncover any new, useful data points. The trip proved to be valuable on many fronts, and the overall takeaways for both companies were positive.

One interesting element on Australian publicly listed businesses that was reinforced to me during my discussions with operators, investors, and locals was just how isolated Perth and Western Australia are from the rest of Australia, in several regards. Geographically, Western Australia contains 33% of Australia’s land mass, yet only boasts a population of 2.7 million people or 11% of Australia’s 25.7 million total population. Within Western Australia, its most populous and only true city Perth fields a population of around 2 million.

In addition to being physically separated from Eastern Australia, it also seems that Western Australia is considered by many in the east to be a different country altogether. It is even generally viewed as an afterthought when compared to the country’s more popular eastern cities. Interestingly, this mindset appears to prevail within Australia’s investment community as well, and as a result, Perth-based companies seem to receive less coverage and less interest than their eastern-based counterparts. I don’t have empirical evidence to verify this observation, but I expect it may partially explain why I have also found Perth-based companies to be less efficient, all else equal, than their eastern-based peers within Australia.

With respect to Mader Group and Duratec, below is a summary of my field research takeaways.

Mader Group

Mader Group’s executive team was kind enough to welcome me to their headquarters where I was introduced to various business functions and team members, as well as given a tour of one of their offsite maintenance centers where select mining vehicle repairs take place.

After having spent over two years studying and investing in this business, it was helpful to finally see the vehicle repairs in action while being accompanied by CEO Justin Nuich and the maintenance center’s General Manager. This allowed for a more granular understanding of the nuts and bolts of the company’s business model.

It was also valuable to meet various internal business teams such as culture unit Three Gears, which is undertaking initiatives to maximize mechanic retention, and the centralized mechanic oversight unit, which is harnessing the power of Mader Group’s significant investments in proprietary technology, a key reason why no competitors have been able to scale beyond a fraction of Mader Group’s size and scope.1

Above all, perhaps the most important takeaway from my time spent with Mader Group was the evident pride and passion for the company, almost electric, that radiated from just about every employee. Looking around at all of the optionally-donned polo shirts with company logos and chatting with a handful of folks, it was evident to me that upper management has fostered a culture where employees across all functions are ambitious for the company and feel unified in their mission of success. In my experience, having a powerful culture, which can manifest in different forms, is one of the intangible business attributes that is difficult to quantify, but many of the companies that experience long-term success possess it.

We remain excited about Mader Group’s long-term business prospects and its potential to generate attractive returns for our partnership. The company’s vast organic rights to win in North America, where it currently only captures 2-3% of its total addressable market, should provide a long runway for earnings growth in the years to come.1 For context, Mader Group possesses over 40% market share in Australia, which suggests a potential multi-billion dollar opportunity in North America of 10-20x its current annual revenue there.1

Duratec

Duratec’s executive team was extremely kind in the depth and breadth of access they allowed me to meet with executive management, spend time with business unit leaders, and perform site visits across just about every business segment.

As an asset remediator, Duratec is quite unique in its collection of business segments in which it performs work including Department of Defense naval sites, mine sites, oil and gas projects, buildings & façades projects, and various Government works.

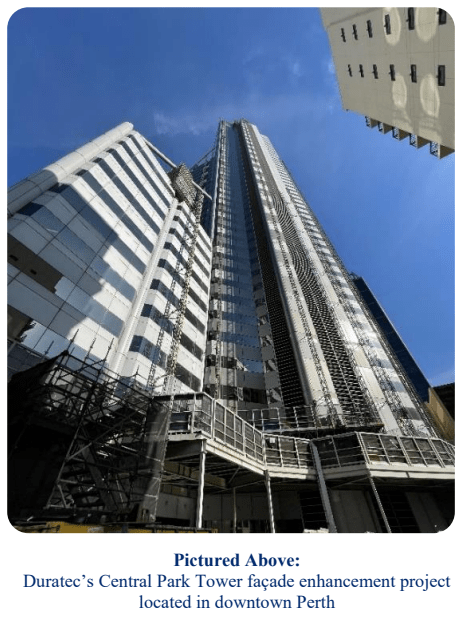

Fortunately for me, Duratec was able to arrange site visits for at least one project across each of its major business segments. This included trips to the Garden Island naval base off the coast of Perth, the Boddington gold mine two hours south of Perth, the Central Park Tower façade enhancement project, a tour of Wilson’s Pipe Fabrication’s warehouse facilities, the Cockatoo Island remediation projects in Sydney, and more.

Each of these visits was accompanied by a manager at Duratec. This made for educational experiences and crystallized my understanding of how each business unit operates within the greater company, how each business unit fits within its competitive landscape, and the clear paths to continuing to expand each business unit’s revenues and profits. During these visits, it was the finer details such as the interactions at Boddington gold mine with mine site engineers and Newmont decision-makers, and at the Garden Island naval base with Duratec field staff, that helped tie loose ends and improve my comprehension of Duratec’s business in ways that would not have been possible from behind a desk in New York.

Spending time at MEnD Consulting’s main office in Perth was also certainly a highlight. MEnD’s senior employees walked me through the 3D modeling software equipped with their proprietary AnnoView API as well as their NATA-accredited petrography lab. The team at MEnD is clearly highly motivated and driven to remain at the cutting edge of technological applications within the field of asset remediation, which should continue to bode well for Duratec as a whole going forward.1

The most impressive takeaway during my time spent with the Duratec team was the sheer depth of talent they possess throughout their first- and particularly second-level management. Having discussions with executives across all business functions mentioned above, as well as with DDR and the East Coast main office, made it clear to me that Duratec’s business units are run in a largely decentralized fashion. Segment leaders take direction from top management, but carry heavy responsibilities themselves, and also exhibit a strong sense of entrepreneurial spirit. Over the course of car rides and shared meals, if there were one consistent theme among these managers, it was the deep well of ideas all of them had to improve their businesses, coupled with an eagerness to implement these ideas and score meaningful wins for their teams.

In examining Duratec’s business units, there is a lot I find to be enthusiastic about for the company’s future:

- The company’s fast growing Department of Defense business segment, most recently delivering $229MM in annual revenue, appears well-positioned to eventually become a $1B+ annual revenue standalone business unit.1

- The mining and industrial segment continues to deepen its ties within existing bases and gradually win additional high-margin work.1

- The buildings and façades segment should continue enjoying the nationwide flammable cladding remediation tailwind for the next ~5-10 years. This unit should be well-positioned to win recladding work after the 2024 completion of its $63MM Central Park Tower recladding project, the country’s biggest recladding project to date, which should serve as an excellent showcase of Duratec’s proficiency to prospective clients.

- DDR, despite its hiccup in results last year which was the result of delayed Government spending, should be poised to return to its FY 2022 results, and over the long-term potentially far greater, thanks to strong demand for remediation work by Aboriginal-owned businesses and DDR’s strong competitive position within the space.1

- Wilson’s Pipe Fabrication, most recently delivering just $27MM in annual revenue, has a tremendous opportunity to become “as large as defense” according to top management, or greater than $200MM in annual revenue, driven by domestic geographic expansion and untapped addressable market opportunity.1,2

- MEnD Consulting continues to add enormous value to Duratec and increasingly attract the attention of major asset owners.1 As mentioned in Duratec’s FY 2023 update, one or more existing clients have demonstrated interest in utilizing MEnD’s services for other assets they own internationally, demonstrating the value clients are finding in MEnD Consulting’s services.

We remain excited about Duratec’s long-term business prospects and its potential to generate attractive returns for our partnership. There is a high likelihood, in our view, of double-digit growth to persist across most or all of Duratec’s business segments for the foreseeable future, and we believe this could reasonably allow the company to deliver AUD $1.0-1.2 billion in revenue in 4-5 years at similar bottom-line margins as today, or AUD $40-50 million in net income.1 We look forward to monitoring Duratec’s evolution.

Closing Thoughts

Thank you for taking an interest in our latest letter. I am excited about our partnership’s future.

I remain confident that our partnership’s north star will always be to compound our capital at the highest rate of return responsibly possible. In some respects, this approach may render our partnership uninvestible by many institutional investors. That is perfectly fine by me. We will continue to accept as partners only those who understand, and who are aligned with, our objective.

If you wish to learn more about the partnership, please feel free to reach out to me directly. Our partnership currently welcomes introductions to new investors who are aligned with our philosophy and our long-term approach. Accredited Investors interested in receiving future letters can also register on our website at www.sohrapeakcapital.com.

I value the trust you have placed in me to invest your hard-earned capital, as the substantial majority of my own wealth is presently invested alongside yours. I look forward to writing to you again next quarter.

Most Sincerely,

Jonathan A. Cukierwar, CFA

Manager of Sohra Peak Partnership LLC, the General Partner of Sohra Peak Capital Partners LP

|

Footnotes 1Source: Estimates, thoughts, opinions, and research of Sohra Peak Partnership LLC. 2Source: Duratec, Presentation at NWR Vantage Point Conference, May 2023. http://bit.ly/3MI40TQ. DisclaimerThis report is based on the views and opinions of Jonathan A. Cukierwar, which are subject to change at any time without notice. The information contained in this report is intended for informational purposes only and is qualified in its entirety by the more detailed information contained in the Sohra Peak Capital Partners LP offering memorandum (the “Offering Memorandum”). This report is not an offer to sell or a solicitation of an offer to purchase any investment product, which can only be made by the Offering Memorandum. An investment in the Partnership involves significant investment considerations and risks which are described in the Offering Memorandum. The material presented herein, which is provided for the exclusive use of the person who has been authorized to receive it, is for your private information and shall not be used by the recipient except in connection with its investment in the Partnership. Sohra Peak Partnership LLC is soliciting no action based upon it. It is based upon information which we consider reliable, but neither Sohra Peak Partnership LLC nor any of its managers or employees represents that it is accurate or complete, and it should not be relied upon as such. Performance information presented herein is historic and should not be taken as any indication of future performance. Among other things, growth of assets under management of Sohra Peak Capital Partners LP may adversely affect its investment performance. Also, future investments will be made under different economic conditions and may be made in different securities using different investment strategies. The comparison of the Partnership’s performance to a single market index is imperfect because the Partnership’s portfolio may include the use of margin trading and other leverage and is not as diversified as the Standard and Poor’s 500 Index or other indices. Due to the differences between the Partnership’s investment strategy and the methodology used to compute most indices, we caution potential investors that no indices are directly comparable to the results of the Partnership. Statements made herein that are not attributed to a third-party source reflect the views, beliefs and opinions of Sohra Peak Partnership LLC and should not be taken as factual statements. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment