Rich Fury

Introduction

Despite what the share price action of the last 2+ years suggests, SoFi Technologies, Inc. (NASDAQ:SOFI) is a fast-growing, loss-narrowing company with good business execution. Started with nothing but refinancing student loans, SoFi Technologies is now an official bank offering its customers all the standard banking services through a “one-stop-shop” app. Furthermore, SoFi provides a service with which its customers can buy and sell cryptocurrencies. The goal is to offer the easiest and most convenient digital access to these services without customers relying on branches. Therefore, the target audience is primarily younger people, also called “digital natives.” So far, that strategy has functioned well, with customer count being the fastest-growing metric in SoFi Technologies’ earnings reports.

Quick overview about previous business results

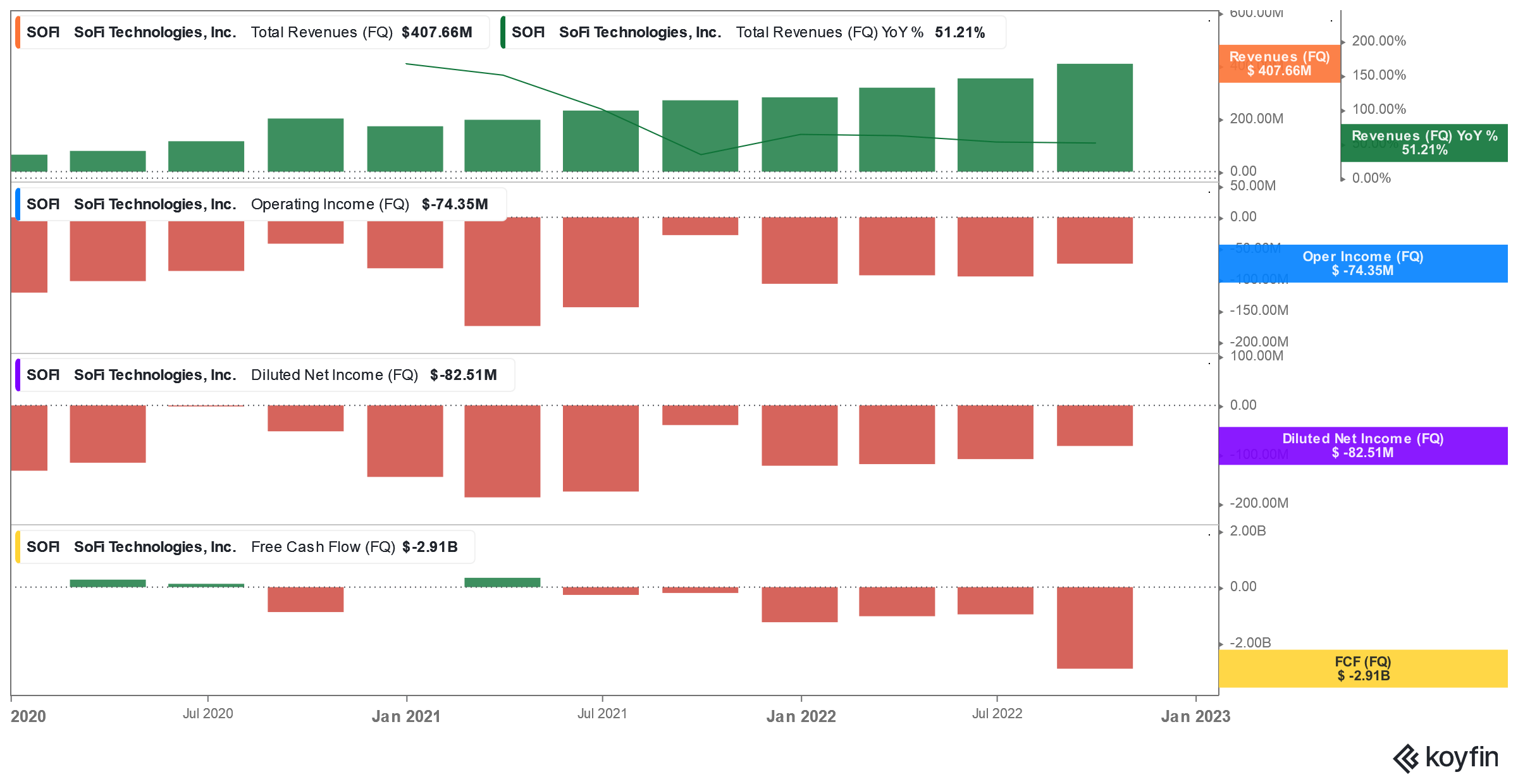

So far, SOFI has done very well in continuously growing revenue and narrowing losses. Except for the free cash flow, which dropped a lot in Q3 2022.

Sales and earnings past quarters (koyfin.com)

Most critiques I read about SOFI are that the company is still not profitable, an argument I do not share. SOFI is continuously narrowing losses and has done most of its business structuration in the last two years.

Business execution timeline (SoFi IR)

As you can see, SOFI has done so much in the last year alone, the most significant being the regulatory approval to become a national bank. Or the launches of multiple products, like the 3% cash back, SoFi Smart Energy ETFs, or the options trading rollout. But how has all this contributed to sales and earnings? Let’s look at the latest quarter and the whole year 2022.

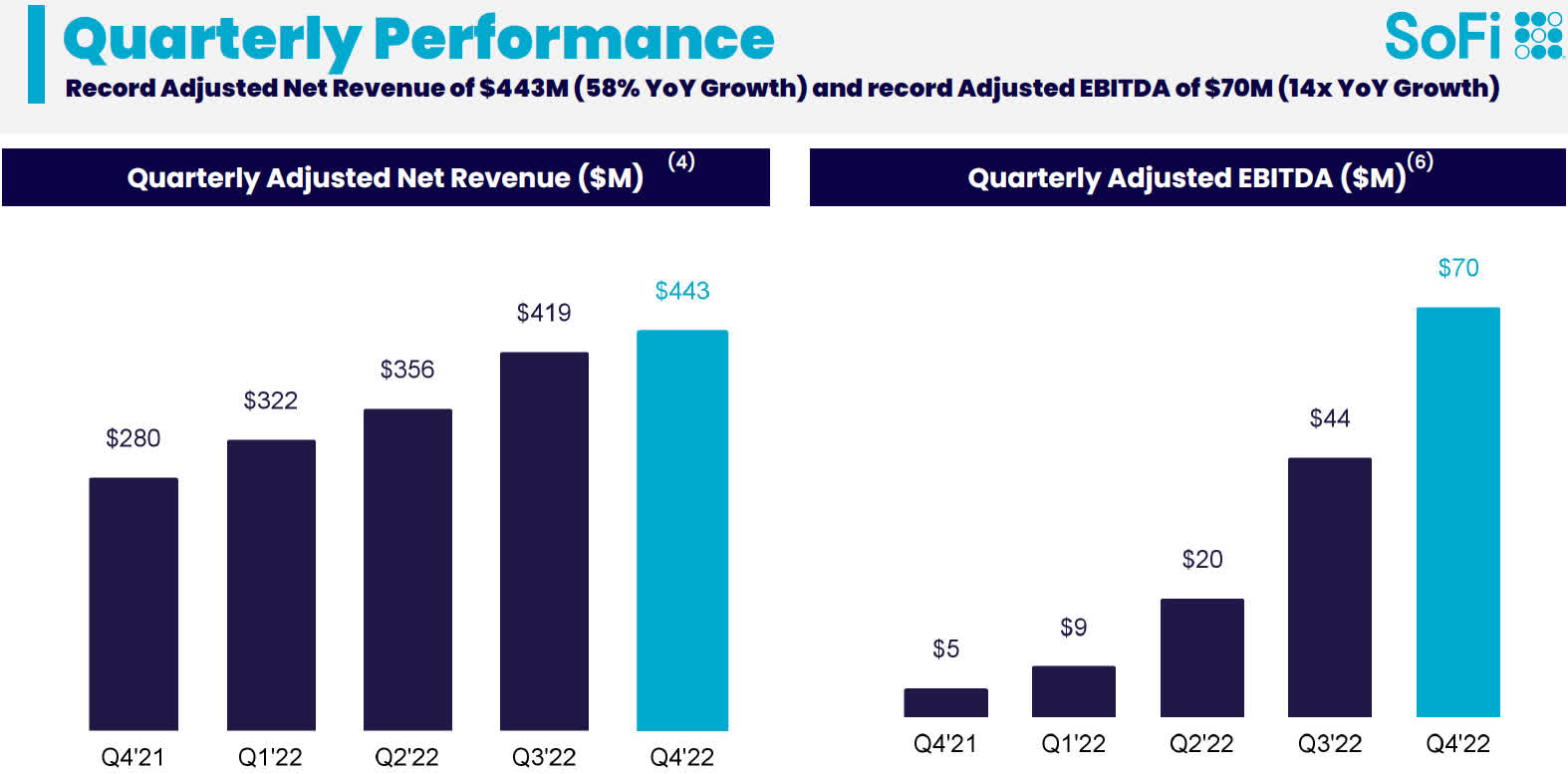

Q4 earnings report

SOFI managed to grow its revenue by 58% YoY, which is higher than in the last two quarters (52%, 51%). Adjusted EBITDA was multiplied by 14 from $5M in Q4 2021 to $70M in Q4 2022.

Quarterly performance (SoFi IR)

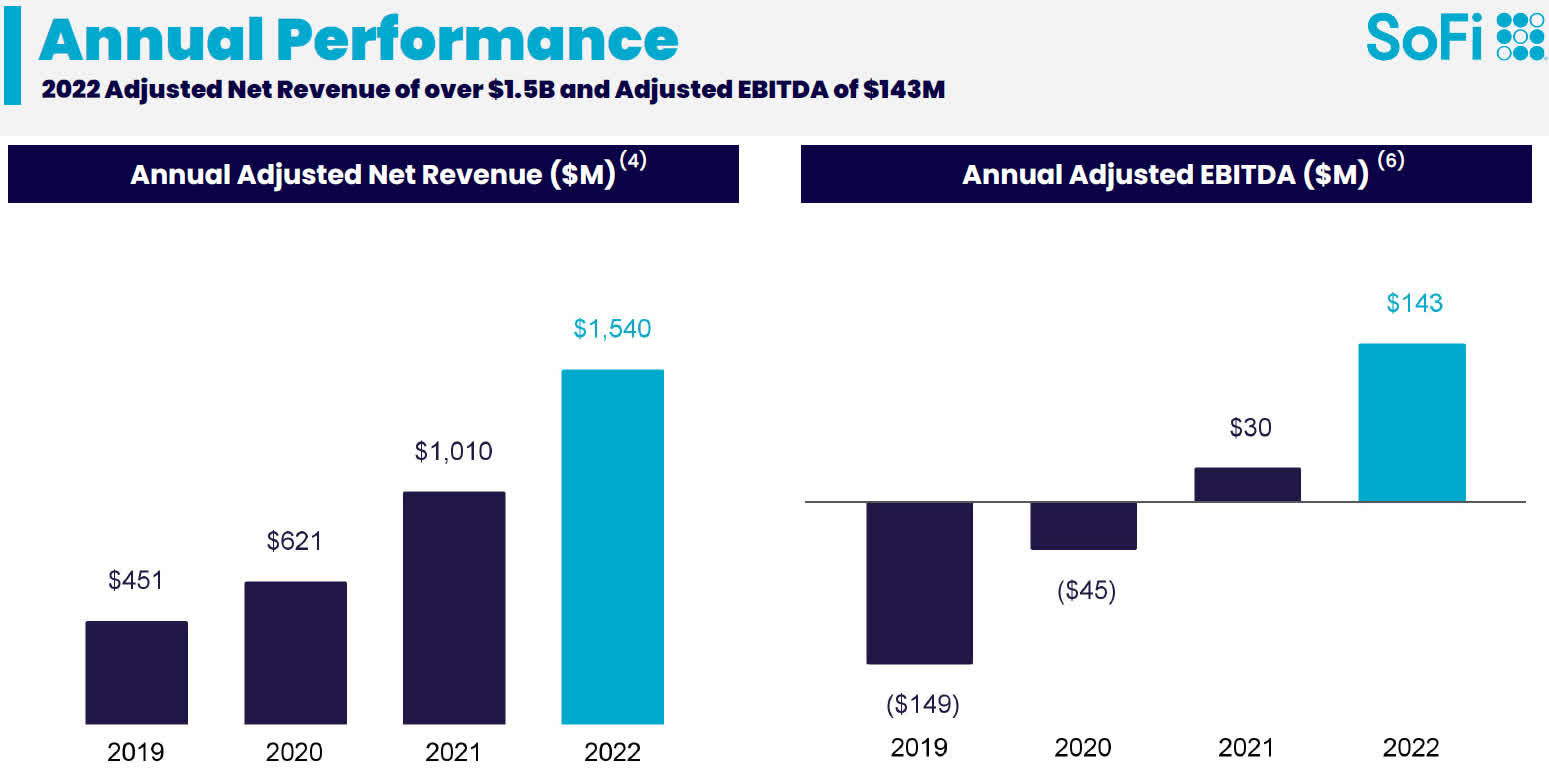

Annually, revenue growth reached 52.5% YoY, and adjusted EBITDA grew by an astonishing 377% YoY.

Annual performance (SoFi IR)

Because adjusted EBITDA is only sometimes representative, because the management can calculate it in a way it looks better than the actual earnings, I will show the GAAP measures.

GAAP measures (SoFi IR)

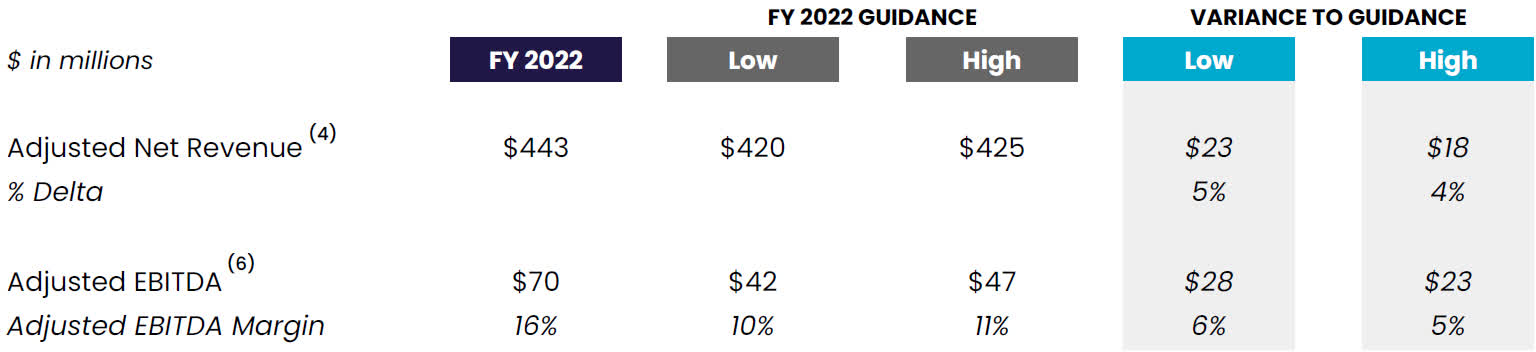

From a positive $70M adjusted EBITDA, SOFI drops to a negative $40M net income on a GAAP basis. While this could sound more compelling, we must look at the development. Quarterly, SOFI narrowed the net loss by 64% and 67% per share, which is excellent news. Annually, this doesn’t look as good as quarterly but is still decent, with a reduction of total net loss of 34% YoY and 60% YoY per share. These results were comfortably above managements guidance:

FY22 results vs guidance (SoFi IR)

Company metrics

To analyze SOFI’s business execution and growth, it is crucial to look at the company’s own metrics. I want to begin with members, SOFI’s customer count:

Members (SoFi IR)

SOFI’s members hit an all-time high of >5.2M, which grew by 480K or 51% YoY. Even though growth is continuously trending slower, >50% customer growth is still impressive. SOFI’s product count shows similar growth, with almost 700K products added, or 53% YoY growth.

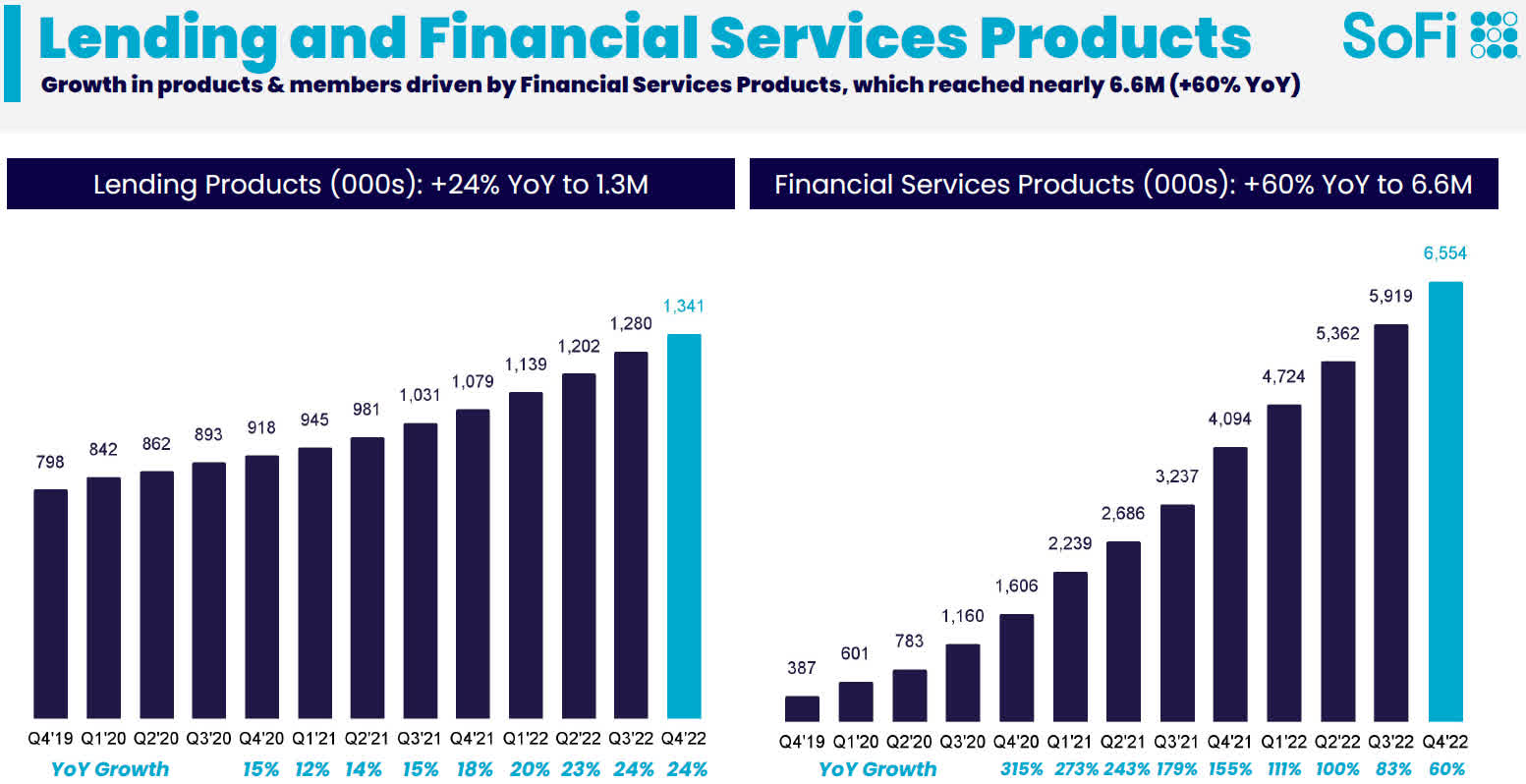

Products (SoFi IR)

Again, growth is slowing but still very good.

For me, it is essential to know SOFI’s “products per member” to see if existing users also grow their usage of SOFI’s services. In Q4, products per member were 1.51 against 1.51 in Q3 and 1.5 in Q4 2021. So SOFI expands its products almost simultaneously to its members. I would be happy to see that number rise again because it would show more adoption of SOFI’s services by existing members.

Product structure (SoFi IR)

Looking at the growth in different sections, we can see that lending products are growing much less than financial service products (24% vs. 60%). This is due to the student loan moratorium the Biden administration has still in place. As of now, it will continue until August this year, but since it got extended multiple times already, I wouldn’t bet on an end in August. As soon as this is over, SOFI should see accelerating demand for student loan refinancing, which should boost growth.

Galileo, SOFI’s financial technology platform, which they bought in 2020 for $1.2B, is growing its members decently with 31% YoY.

Galileo accounts (SoFi IR)

Considering the big announcement SOFI’s management made when they acquired Galileo, I thought it would grow faster, but this is still more of a future growth driver.

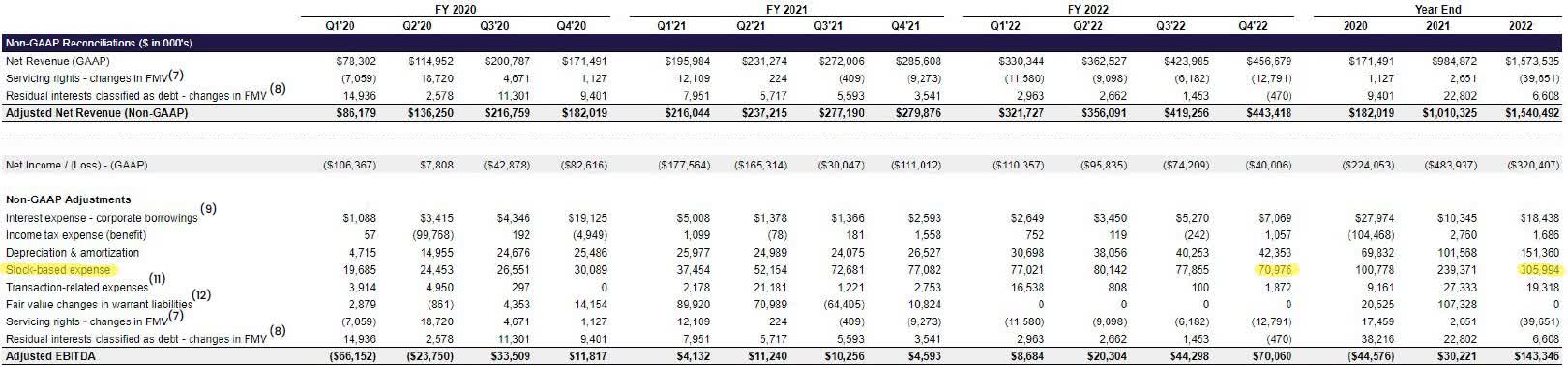

One of SOFI’s problems is the stock-based compensation (SBC), which is very high and dilutes the shareholders.

Stock based compensation (SoFi IR)

In Q4, SBC was the lowest since Q2 2021, with $70M, which sounds good initially. Looking at the whole year, we can see that SBC was the highest ever, with almost $306M. I want to see this number go down significantly in the future.

Guidance

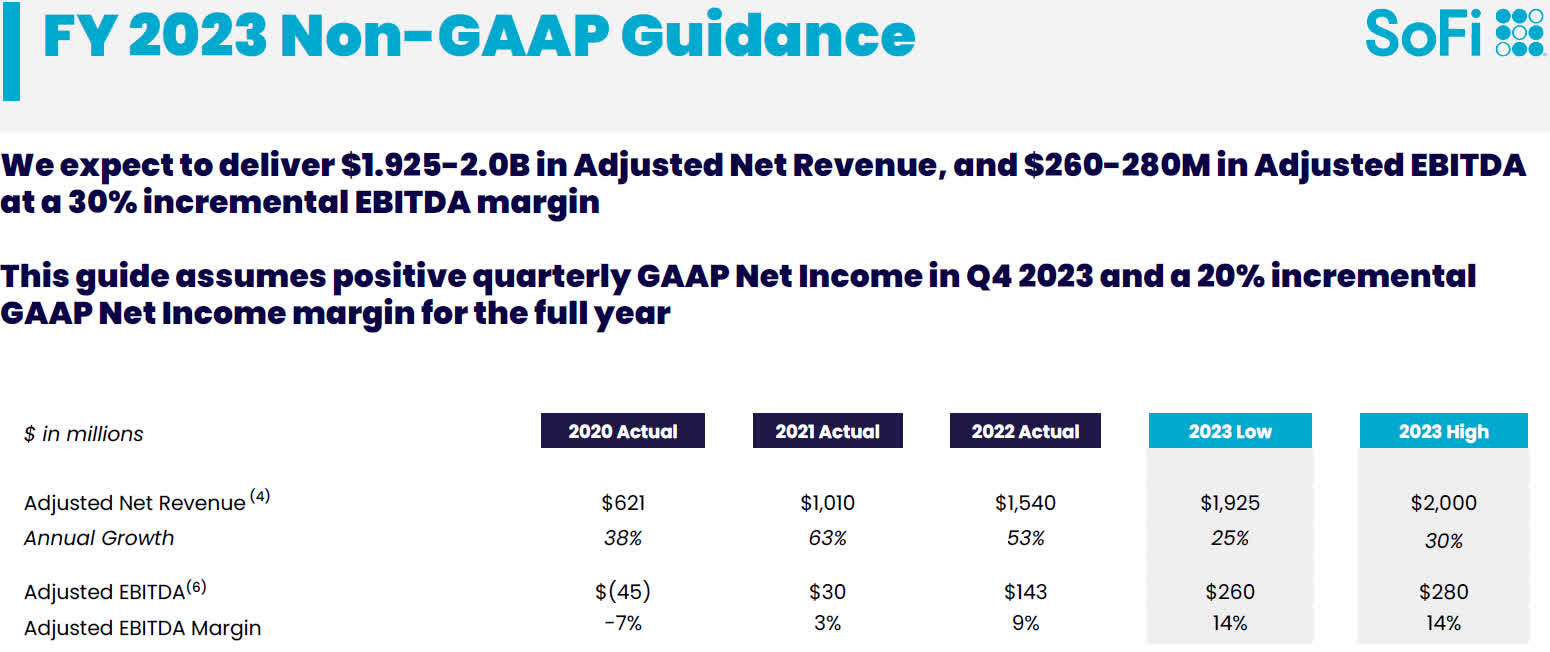

For Q1 2023, SOFI’s guidance is relatively conservative, with $430M – $440M in adjusted revenues, forecasting a YoY growth of 34-37%. Quarterly, this would mean no increase at all. Adjusted EBITDA is intended to be $40m – $45M, or 9-10% YoY growth. Quarterly, this would mean a decline of about 40%.For the whole fiscal year 2023, guidance looks better.

FY 23 guidance (SoFi IR)

Revenue and EBITDA are projected to slow down by a considerable margin. I think that guidance looks rather conservative, which could either mean management believes their prospects are weakening or they purposely undermine their ability to grow to then beat their guidance. Either way, the end of the student loan moratorium isn’t calculated into this guidance, so if it indeed ends within the year, the guidance should be raised rather significantly.

Conclusion

SoFi Technologies, Inc., again, showed it could grow rapidly and improve its earnings. Should the development continue, I could see profitability at the end of 2023 or in the first quarter of 2024. This would be a big step, and the share price should appreciate accordingly. Apart from that, SoFi Technologies, Inc. management is excellently launching new products and developing the business structure to rely less on student loans and become the one-stop-shop for the banking it wants to be. Therefore, I consider SoFi Technologies, Inc. a buy, but recommend being aware that the share price is at +50% YTD, which would mean a correction could be on its way, and there could be a chance to buy in lower.

Be the first to comment