beekeepx/iStock via Getty Images

Thesis

Intro

Smith-Midland (NASDAQ:SMID) is a precast concrete manufacturer of highway barriers, commercial-sized building walls, and other off-site concrete construction products. SMID recognizes revenue through product sales, rentals, royalties, and services. We believe SMID is at an inflection point as their business lines are seeing significant macro-economic and governmental tailwinds while demand is at all-time highs.

Specifically, we see SMID’s SlenderWall and J-J Hooks rental business as major drivers of revenue growth and bottom-line expansion. Along with this, we believe that SMID will have a generational opportunity to acquire high-performing regional production facilities (who are producing SMID products and paying royalties) expanding their geographic presence and further spurring growth.

We see strong revenue growth, significant margin improvement, and improved operating leverage for SMID fueled by continued supply shortages, governmental mandates, and a shift to a higher-margin rental business.

SlenderWall – Macroeconomic Tailwinds

A crisis-level supply shortage of construction workers across the nation is forcing developers to look towards less labor-intensive ways of completing projects. We firmly believe this supply dynamic will cause a substantial shift in near-term/long-term development projects of commercial buildings from traditional construction methods to less labor-intensive off-site modular methods. This will lead developers directly to SMID’s SlenderWall (SW).

SW is an off-site modular wall panel that requires roughly half the labor compared to traditional construction methods. This is because the wall is already built (windows, drywall, insulation, etc.) when it arrives at the job site and it is simply put into place like Legos. Per our conversation with management, they quantified the labor benefit of SW:

- A traditional brick construction requires 30 construction workers versus 7 with SW

- A 30ft by 10ft SW can be completed in one hour compared to nine hours via traditional methods

- SW is 1/3 the weight of traditional precast panels, which allows contractors to use smaller (cheaper) cranes and architects to build taller buildings.

On top of the labor benefits, SW provides benefits to architects, engineers, contractors, owners, and developers furthering the value proposition. Architects and engineers benefit from the flexibility of SW stylistically. Their recent projects highlight this varying from beach-front residential housing consisting mostly of glass to brick-facing office buildings. Contractors benefit from lower labor needs and the certainty of the building timeline. Projects are not delayed due to weather, as SW walls are built inside and can be installed in any type of weather.

Very low maintenance and heating/cooling costs associated with SW benefit owners and developers in the long run. Combined, these benefits equate to costs and construction timelines that are nearly half those of traditional methods.

Smith-Midland Smith-Midland

While SW provides a long list of benefits to all parties, it is still relatively unknown in the construction market. Per our conversation with management, they believe they aren’t even at 100 basis points of market penetration. This lack of penetration and awareness by decision-makers is the biggest hurdle for SW moving forward. To combat this, SMID is hiring two new SL sales reps this year. We believe the expansion of the sales team coupled with increased marketing spend will significantly increase the awareness and sales of SW. As this increased marketing and sales spending comes at the exact time when decision-makers are searching for ways to complete projects amid inflation, surging commodity prices, and labor shortages.

We believe that SW is a hidden asset that is poised to gain traction in the near and long term as labor shortages persist. We point out that Nexii, an off-site modular wall panel company, has recently raised $180M at a $2B valuation. Nexii is primarily focused on lowering the carbon footprint of construction builds of residential housing and small-scale retail through off-site construction. While not a perfect peer, as Nexii’s end market is easier to break into than SW’s, we believe that this is another feather in the cap for the case that off-site modular construction is the way of the future.

J-J Hooks – Business Shift/Governmental Mandates

J-J Hooks (JJH) are SMID’s proprietary, freestanding, and moveable highway barriers. These are the segmented cement barriers often seen during highway construction. Historically, SMID had produced and sold JJH but starting in 2015 a significant pivot was made. With an initial 30,000 linear feet fleet, SMID began renting JJH. This switch has been transformational to SMID and a massive success. It has resulted in higher margins, recurring revenues, and improved cash flow.

The success of the JJH rental business is also be highlighted by the amount of capital SMID has spent since inception, growing rental capacity by 10 fold to 300,000FT. Management has also noted that they are looking to double that capacity by 2024/2025.

JJH are the premier highway barrier on the market. This is because of the ease of installation, worker safety, and minimal labor required. A 2 man crew can install roughly ~45 units per hour, in comparison to competing models where it’s not even possible to set up with 2 workers. The ease of use stems from JJH requiring no pins or connection hardware, it simply “hooks” into place. Along with this, JJH is not a male/female system like competitors, further easing the installation process.

Smith-Midland

Smith-Midland

To go along with this excellent business shift, a recent new mandate from the National Highway Systems, MASH TL3, is forcing all national highway barriers to be updated to meet these new safety requirements over the next 5-7 years. With this in mind, we firmly believe that SMID will see sustained elevated demand for its JJH rental business over the next decade. This elevated demand will be occurring just as SMID is doubling its rental fleet capacity and allowing itself to take on larger more lucrative contracts. Along with this, we believe SMID will see sustained elevated royalty revenues from the 70+ licensed manufacturers across North America producing JJH. Per our conversation with management, they believe this update of the national highway system is only in the second inning, hence our conviction in the long-lasting elevated demand for JJH.

Timely and Insightful Geographic Expansion

Precast concrete product manufacturing is very fragmented by geographic region. This is due to the high costs of shipping the products over long distances. This embedded fragmentation of the market leads to many “Ma & Pa” regional operators. Many of whom produce SMID products and pay royalties.

Because of this geographic fragmentation, we believe that the industry as a whole is ripe for M&A. Furthermore, we believe that SMID is uniquely positioned to acquire high-performing plants. This is because:

- SMID receives monthly royalty data from the 70+ plants producing their products. From this, SMID has direct visibility into which plants are receiving the most business and highest-performing.

- These plants are already equipped to produce SMID products. Therefore SMID would have to spend very little capital, if any, on upfitting or retraining workers.

- SMID is well-positioned financially to acquire assets with $15M in cash, a 2.54 current ratio, a $28.8M backlog, $12.6M in AR, and our model projecting $7.4/10M in operating income in 2022/2023.

To our knowledge, SMID is the best-positioned small-cap company to conduct serious M&A in the coming years. We believe this dynamic sets up a generational opportunity for SMID to become a national powerhouse during a time when the demand for its products is at an all-time high.

Background

SMID is headquartered in Midland, Virginia with production plants in Virginia, North Carolina, and South Carolina. Along with SL and JJH the company manufacturers and licenses out an array of other precast concrete products such as SoftSound, a noise-reducing highway barrier, and underground concrete utility boxes used for data centers. Management has commented they are seeing robust growth for their utility boxes from new data center builds, seeing a 251% increase in their last quarter on a YoY basis.

SMID was founded in 1960 when the founder, Rodney Smith, created an innovative new pre-cast cattleguard product. Since then, the company has gone on to launch many innovative pre-cast concrete products. SMID went public in 1995 listing on the OTC and was uplisted to the NASDAQ on November 12, 2020. Management is very well aligned with shareholders as they own ~17.5% of the stock.

SMID receives royalties through the licensing out of their products to 70+ manufacturers across North America and the Pacific Southeast. Per our conversation with management, there are currently 40 plants producing JJH and 4 producing SL with a 5th awaiting an order from the west coast region to bring it online. SMID currently receives a 6% royalty, which management believes they can increase in the future. Management does not believe an increase in royalty fees would cause a loss in business. This is because the demand for SMID products is so strong and there are few suitable substitutes for them.

SMID’s current geographic reach for their own production and rental products is contained mostly to the mid-Atlantic region. Stretching as far north as NY, as far west as TN/KY, and as far south as FL/AL. As stated earlier, the limitations of SMID’s geographic reach are due to the high costs associated with shipping.

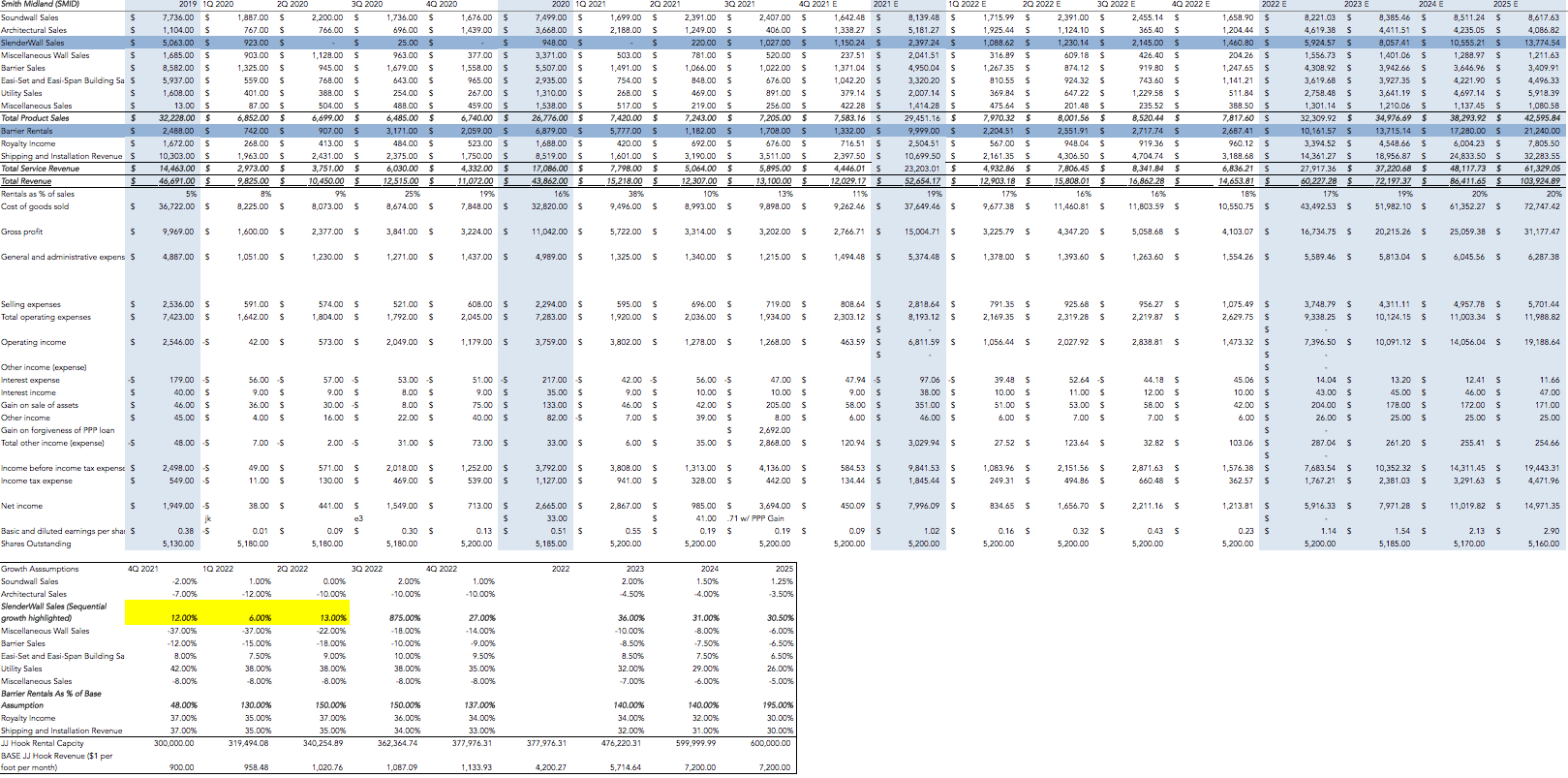

Valuation and Model

Our model is created using our conversations with management, our own expectations, industry trends, and past results to project out SMID’s income statement through 2025. SMID reports 11 different revenue streams, for which we modeled each out differently. As our thesis indicates, the largest drivers of growth in our model are SW sales and JJH barrier rentals. Utility sales (data centers) and royalties are secondary key drivers. We model declines in JJH product sales, architectural sales, and miscellaneous wall sales. On the whole, we see SMID’s revenue and EPS compounding annually through 2025 at 19% and 30% respectively.

We note that our revenue estimates are modest and we believe there could be significant upside to our projections. This is because we use growth rates for the significant drivers that are well below what those business lines have recently seen. For example, JJH rental revenue has seen an 80% increase through the first nine months of 2021 on top of a 176% jump in 2020 in comparison to our mid-20s yearly growth assumption.

We choose to model out steadier growth based on the expansion of their rental capacity and leave the, very likely but hard to predict, scenario of landing large contracts to the upside. In our conversations with management, they explained they model out $1 per foot per month for the JJH rental fleet. So we applied that same assumption to our own model for our projections.

Per our conversation with management, they are very confident in their ability to continue to land large contracts in the future because of the expanded capacity. We also highlight SMID has recently shown its ability to land large contracts through their $6.4M project with Hampton Roads Connector Partners. For SW we model a jump of 140% in 2022 (17% growth compared to 2019) led by an increase in sales and marketing spend followed by a normalized growth rate in the mid-30s.

Our model assumes gross margins steadily expand, as the higher-margin rental business becomes a larger part of revenue, stabilizing at 30% as rental sales grow to 20% of revenue. We also model 33% growth in 2022 for selling expenses as SMID brings on new sales personnel and increased marketing spend for SW. We assume an effective tax rate of 23%. Our model does not assume any acquisitions, which would also lead to greater sales and profit but higher costs.

Below is a screenshot of our model:

Below is a table of SMID’s current valuation based on our estimated 2022/23/24 sales/EBIT/earnings and SMID’s market capitalization as of March 25th. Also below are our Bull/Median/Bear price targets.

| Valuation Metrics | 2022 | 2023 | 2024 |

| P/s | 1.91 | 1.59 | 1.33 |

| P/EBIT | 15.55 | 11.40 | 8.18 |

| P/e | 19.44 | 14.43 | 10.44 |

| Price Target Model | P/e on 24′ earnings | PRICE TARGET |

| Bull | 17 | $36 |

| Median | 15 | $31.75 |

| Bear | 13 | $27.50 |

BxB Estimates

Potential Catalysts

- Large contract wins in either JJH rental business or SL.

- Initiation of sell-side coverage. Currently, zero analysts cover SMID which we believe is because of the lack of capital needs SMID has. Coverage by Wall St. could lead to more investor interest in SMID, resulting in increased inflows.

- With only ~5M shares outstanding any incremental investor interest should result in an increase in share price.

- Acquisitions of smaller regional manufacturers, expanding SMID’s geographic presence and production capacity.

- Increase of their royalty fees or an increase in the number of plants manufacturing SMID products paying royalties.

- State government mandates forcing DoD projects to use JJH during construction.

Risks

- Lack of execution by new sales personnel and marketing with SW resulting in lower than excepted sales.

- Construction projects pivoting to lower cost barriers over JJH as other costs continue to rise due to inflation.

- State governments forcing DoT projects to use non-JJH barriers during construction.

- Construction labor shortages subside and developers continue to focus on traditional methods for developments over SL.

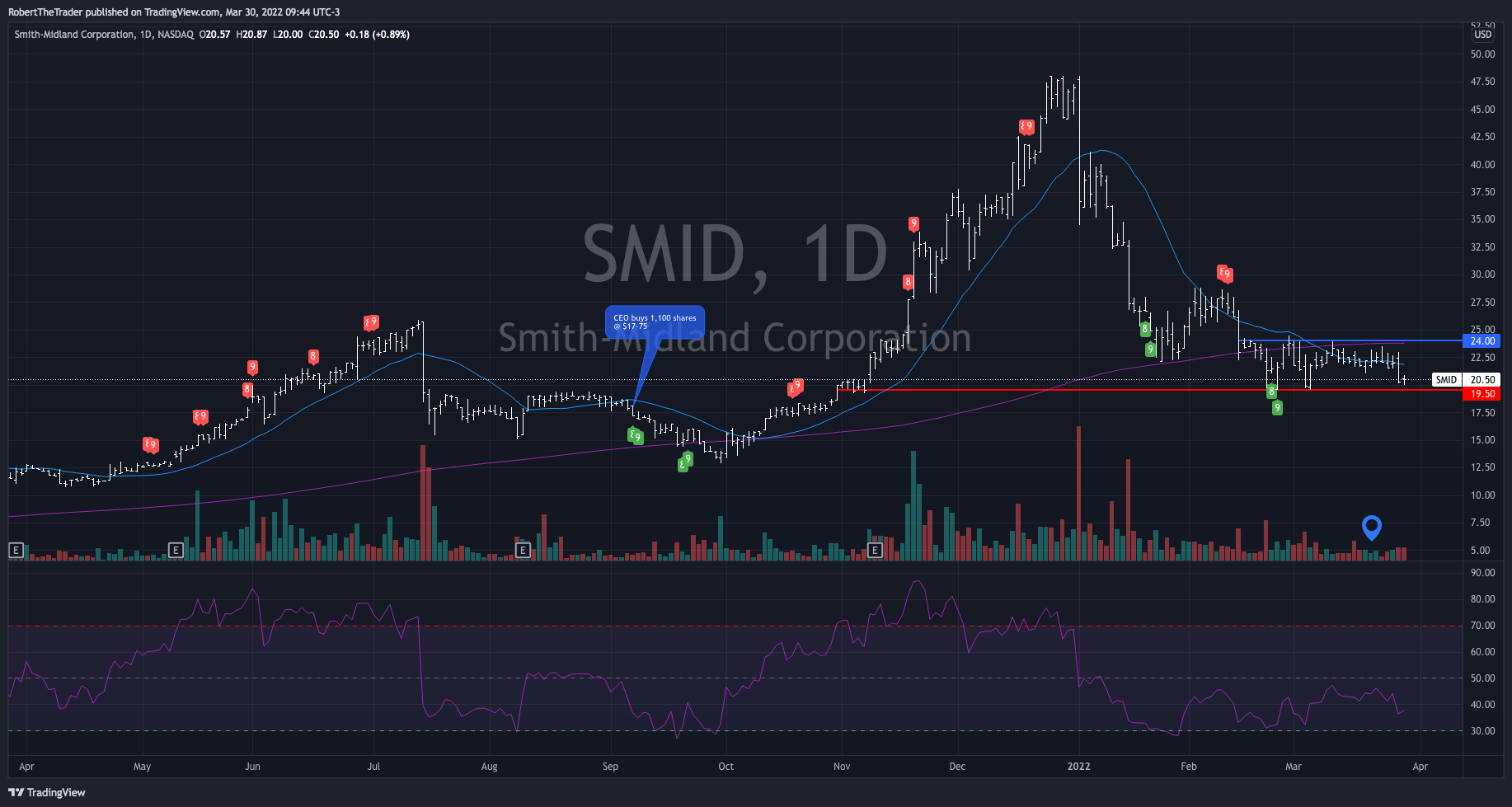

Technicals

On a technical basis, SMID is in a very intriguing spot heading into 4Q earnings on March 31st. The stock saw a massive run going from the low teens to the high 40s in a 9-month span. However, it has fallen more than 50% from those highs through the start of 2022.

Since that fall, SMID has formed a trading channel over the past month with support at the $19.50 level and a resistance level at $24. We believe entering here represents an optimal risk-reduced entry point with upside exposure for the earnings report. As 19.50 has been a strong support since October 2021, before the run-up to all-time highs, and has continued to be a support as this recent trading channel has formed. We think it is very likely that a strong 4Q report and forward guidance could be the catalyst that pushes SMID out of the recent trading channel and into the high 20s.

SMID 1-Year Chart (Trading View)

Conclusion and 4Q Expectations

We believe that SMID is one of the most compelling unknown growth stories in the micro-cap space. With forward compounding revenue growth at 19% and EPS growth at 30% over the next 5 years, the stock is not pricing in this growth. We think that just the JJH or SW business by itself could be a reason to own the stock, not to mention together along with a well-aligned management, strong balance sheet, and possible immediately accretive M&A. As the market has recently turned sour on high-multiple growth stories or profitless growth stories, we think SMID is a clear option for growth investors looking for a reasonable valuation and profits.

With the company reporting after the market close on Thursday, March 31st we will be looking for total revenue of $12.02M, JJH rental sales of $1.33M, SW sales of $1.15M, Gross Margins of 23%, and EPS of .09. As for guidance for 2022, we are expecting total revenue of $60.22M, JJH rental sales of $10.16M, SW sales of $5.92M, Gross Margins of 28%, and EPS of $1.14. We would like to hear commentary on the expansion of their rental capacity along with progression on SW bids and expansion of their sales team. We would welcome any comments on the possibility of expansion through acquisition planned as well.

Be the first to comment