metamorworks/iStock via Getty Images

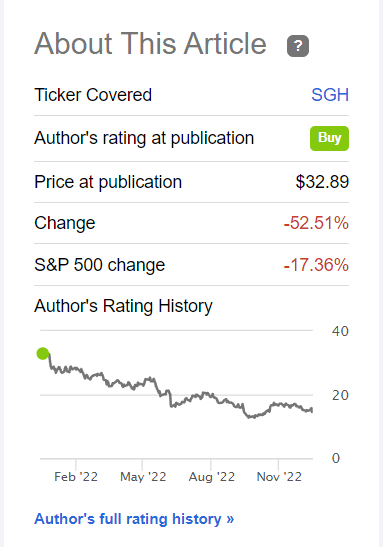

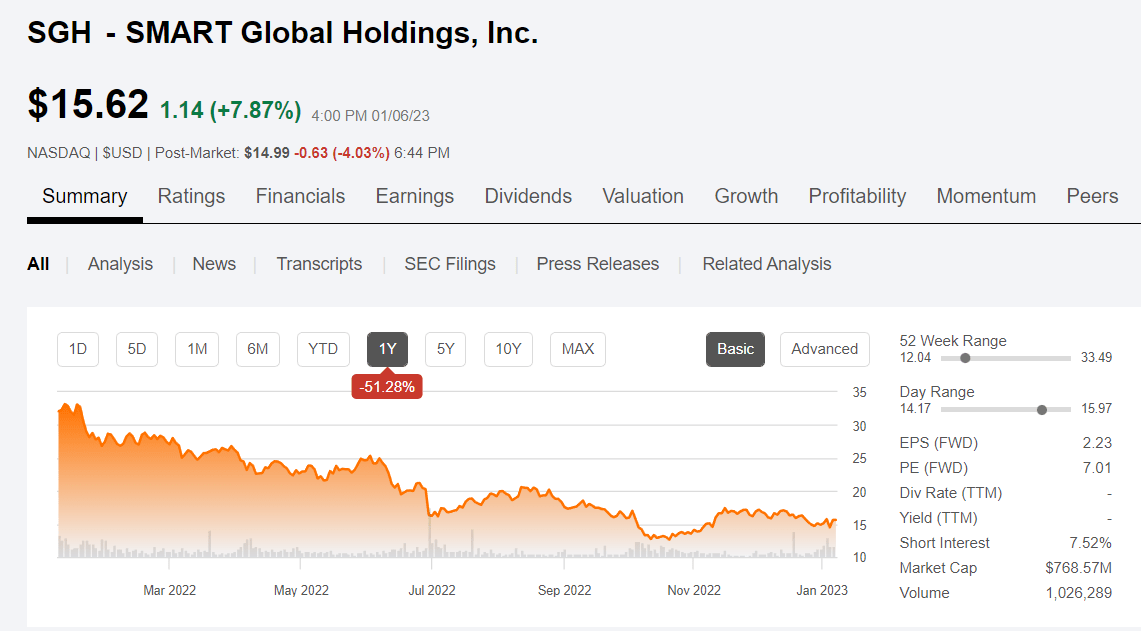

Nearly a year ago today, I covered SMART Global Holdings (NASDAQ:SGH), a reasonably priced technology company experiencing global growth in a variety of innovative technologies that offers potential for capital appreciation as the global economy continues the post-pandemic recovery that started in 2021. Unfortunately, some of the risks that I outlined in that analysis have since materialized driving down the price by more than 50% since that article was published.

Seeking Alpha

What I wrote back in early January of 2022 turned out to be even more prescient than I had imagined at the time.

There could also be general market trends continuing to discount high-growth technology stocks in favor of value stocks as the fear of rising interest rates continues to sway investor attitudes and preferences. The semiconductor industry in general has been in a downtrend since early November as evidenced by the drop in value of many NASDAQ stocks, as compared to the S&P 500 index.

Another risk is the overall economy moving into a recession due to rising inflation and/or interest rates rising too quickly, thus hurting demand for innovation and increasing the costs of production. This is a general risk to all growth stocks, but it does indicate that caution is advised.

Many technology growth stocks declined in price considerably since January 2022 due in large part to those concerns that I had voiced about SGH. For example, Advanced Micro Devices (AMD) is down -53% in the last year. Micron Technology (MU) has declined by more than 40% and Nvidia Corp (NVDA) is down by more than 47%.

Intelligent Platform Solutions

In my previous article from a year ago, I discussed the growth prospects for the IPS (Intelligent Platform Solutions) business in particular, which had experienced 80% YOY growth and with its advances into AI and HPC (high performance computing) offers continued substantial growth prospects into the future. As described in the most recent earnings report on January 3, 2023, the IPS division contributed $211 million in revenues, which accounted for about 45% of total quarterly revenues (total revenues reported were $465 million in the quarter) and represented another 78% YOY growth.

Q1 FY23 earnings call

Some of that growth was due to the acquisition of Stratus Technologies in August 2022. In addition, Penguin Computing, the primary IPS business unit of SGH, acquired the remote access software assets from Colorado Code Craft as explained in a news release from 11/16/22.

“The data volumes and compute-intensive use cases for HPC and AI increasingly lead to situations where data scientists and researchers are operating from locations far from the data center or cloud,” said Thierry Pellegrino, president of Penguin Solutions. “With the acquisition of Colorado Code Craft’s high-performance, browser-based remote display capabilities, we’re able to provide our customers with a secure way to deliver remote desktops and application streaming from any cloud or data center to any device, regardless of the network conditions. This agentless solution accelerates users’ work processes by enabling rapid access to in-place data on the HPC/AI cluster and operates without the need for application or user workstation modifications.”

Furthermore, the IPS business is expected to continue to experience strong demand in the first part of 2023 as explained by CEO Mark Adams on the earnings call.

As we’ve indicated on previous calls, we see the IPS business stronger in the first half of fiscal 2023, driven by large customer hardware installations. In particular, heading into our second fiscal quarter ending in February, we are seeing strong continued demand, driven primarily by installations at some of our hyperscale and federal customers. As you have been hearing from other technology companies of late though, overall visibility for demand out into calendar 2023 remains uncertain.

LED Solutions

The LED business, which was originated via the acquisition of Cree LED in October 2020, struggled in the quarter due to headwinds from China lockdowns and Covid-19 restrictions. Revenues for the quarter amounted to only $63 million compared to $112M in the same period last year. Near term challenges due to weakening demand and channel inventory reductions are likely to continue to impact the LED business in the first part of 2023.

Q1 FY23 earnings call

Despite the near term headwinds, the company expects to realize long-term value in the Cree LED brand and intellectual property that should result in increased revenues once the macroeconomic headwinds begin to recede. Meanwhile, cost containment and operational improvements will be the focus along with the pursuit of additional opportunities in specialty high-value applications such as entertainment and horticulture, outdoor and architectural lighting, and premium video applications.

If My Memory Serves Me

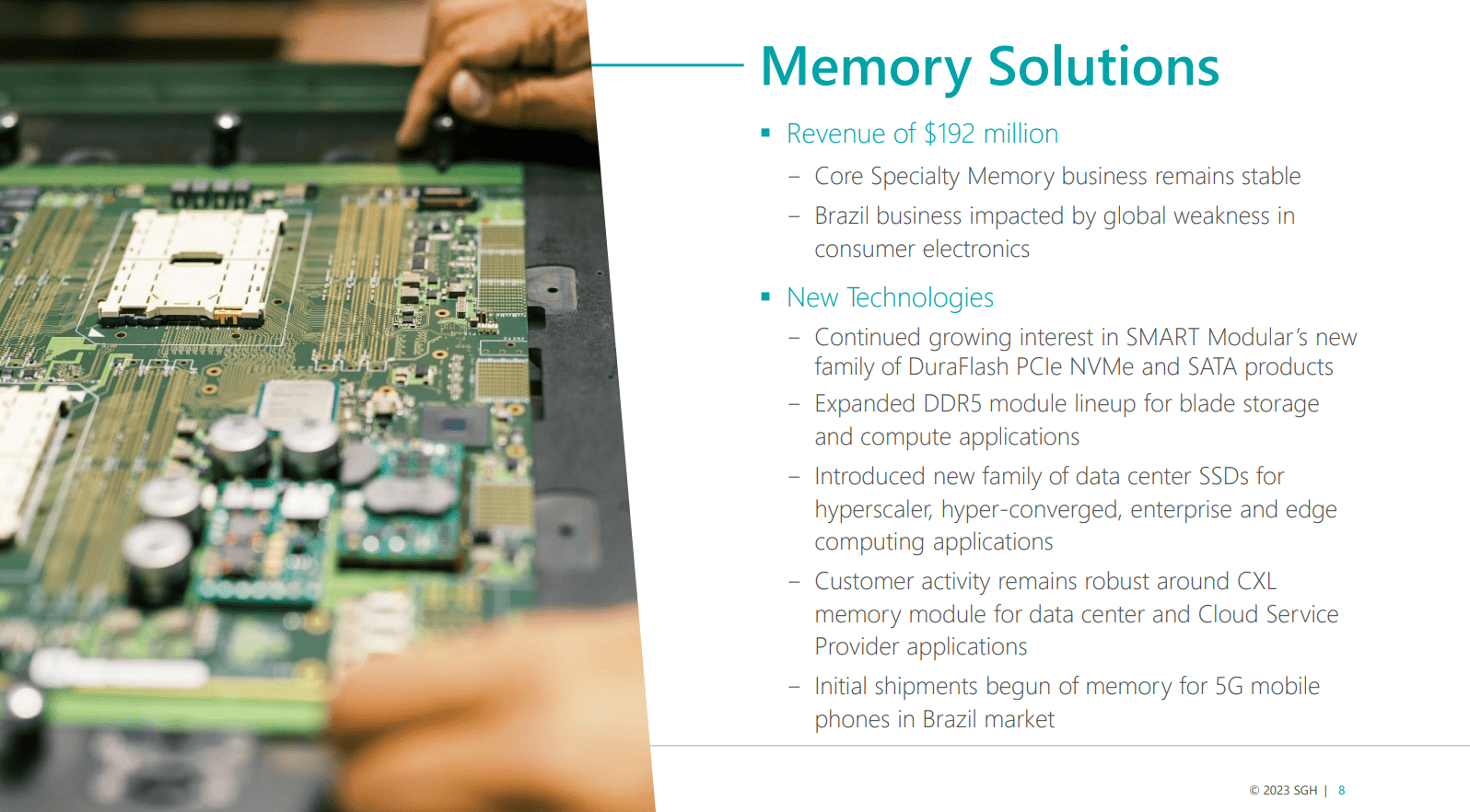

The Memory Solutions division brought in $192 million in revenue in the quarter representing 41% of total sales. Sales declined slightly from FY 2022 due to softening demand, and reductions in worldwide pricing of memory products. The core specialty memory business is focused on enterprise end markets and remained relatively stable.

Demand remained solid in the Telecom and Networking segments. The global weakness in laptops and mobile phones impacted the Brazil business. Initial shipments of 5G memory chips for mobile phones are starting to see increased demand with increasing adoption expected in 2023.

Q1 FY23 earnings call

Share Repurchases and Forward Guidance

According to CFO Ken Rizvi, the company repurchased up to $53 million in shares through the first quarter of 2023:

In the first quarter, we repurchased 182,000 shares spending $2.8 million during the quarter. In aggregate, we have spent approximately $53 million under our $75 million share repurchase authorization through the first quarter, repurchasing approximately 2.8 million shares.

Looking forward toward second quarter results, Rizvi mentioned that the net sales should be in the range of $410M to $460M with a midpoint target of $435M. Gross margins are expected to be 25% to 27%. GAAP diluted EPS expected to be roughly $0.13 in the 2nd quarter, plus or minus $0.15 (which sounds like a pretty wide spread to me). Despite all the difficulties in the quarter, the company realized record gross margins and appear well positioned to support future growth as the global economy recovers.

The CEO, Mark Adams, closed the earnings call with this optimistic view of 2023,

We remain very excited about the future of SGH. As we have mentioned, our fiscal ’23 is front-end loaded with some large IPS installations. And like many technology companies, we have limited visibility into the demand environment in the second half of our fiscal 2023. With that in mind, I want to reiterate our commitment to our shareholders that we will remain vigilant in how we operate the Company in the near term while investing for long-term success.

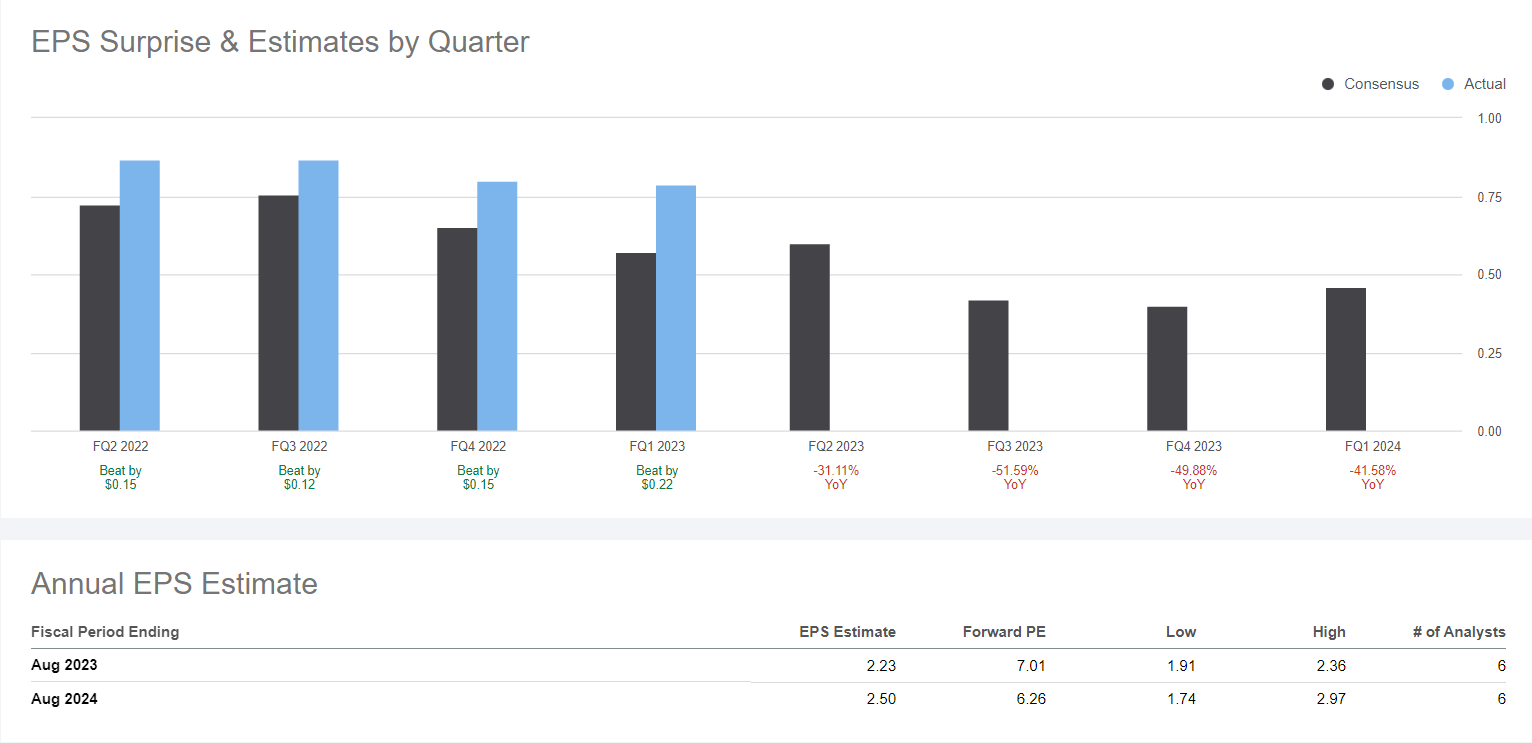

My take is that the global economy and macro environment are the primary cause of the slowdown in SGH growth in 2022 and early 2023. However, the recent past results indicate that earnings beats are pretty consistently occurring despite the headwinds the company has faced. This can be seen visually by looking at the earnings results on SA.

Seeking Alpha

Thus, while the momentum has slowed, and future revenue prospects appear less than encouraging from a growth investor standpoint, I believe that this is an excellent time to purchase inexpensive shares of the company at prices that could be near a bottom now. With a forward P/E of 7 and the possibility of future earnings coming in better than expected if the global economy does begin to recover from rising interest rates and out of control inflation, SGH offers a good value for long-term growth investors.

The stock price reached a 52-week low of $12.04 in October 2022, after reaching a high of $33.49 last January. Short interest stands at 7.5%. As of 1/6/23 the price was $15.62 but was trading below $15 after hours. In my opinion, the stock is a Buy for under $15. Based on an estimated 2024 EPS of $2.50 and a more reasonable multiple of 12x earnings, which is still low for a growth company, the share price could easily reach $30 again by 2024 if things begin to turn around. There is a possibility that weak earnings will continue to dog the company in the first half of 2023 if the fears of recession that many believe is likely to occur actually happens.

Seeking Alpha

The share price may continue to languish in the $15 range for another month or two, depending on what happens with the overall market, but if the market continues to rally like it did last Friday, then I think that the SGH share price could take off and quickly grow to $22 by the next earnings call as annual EPS for 2023 is expected to reach $2.23. At a share price of $22, that still represents an earnings multiple of less than 10 and does not factor in additional growth, which I expect is likely to occur.

Cautious investors may wish to hold off until we get a clearer picture of the market direction, however, the value price may not last long if things do improve quickly. I am personally still avoiding most technology growth stocks for now, but I am watching closely and if I had the cash ready for a speculative purchase, I would be a buyer of SGH at a price under $15.

Be the first to comment