PeopleImages/iStock via Getty Images

You must not fight too often with one enemy, or you will teach him all your art of war.”― Napoléon Bonaparte

Today, we look at a fairly well-known name that came public with much fanfare. Unfortunately, like most companies that debuted via a SPAC in 2021, the shares have not fared well since coming public. The large pullback in the equity has brought in a large recent purchase by the company’s CEO, however. The stock has also behaved better over the past month. An analysis follows below.

Seeking Alpha

Company Overview:

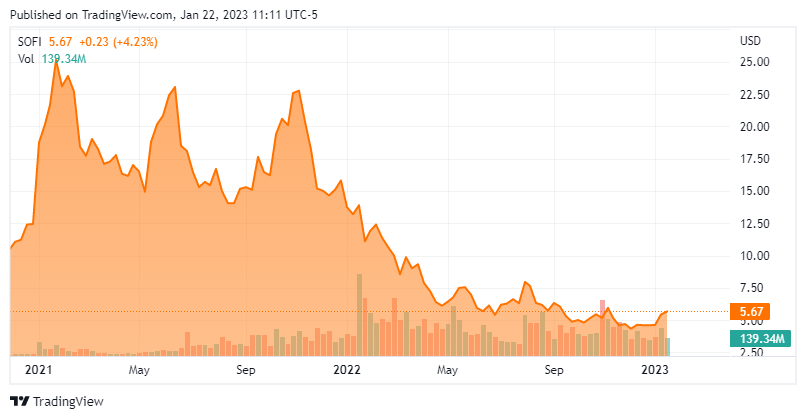

SoFi (‘Social Finance’) Technologies, Inc. (NASDAQ:SOFI) is a San Francisco based self-described “one-stop shop for financial services,” operating a branchless bank from a digital platform that features a ‘super app’. It offers student and personal loans, mortgages, credit cards, as well as savings, banking, investment, and wealth management services to a ‘membership’ that has cumulatively reached 4.7 million with more than $5 billion in deposits. SoFi was founded in 2011 to offer loans to Stanford University students and became a bank holding company in February 2022, subsequent to its public debut on June 1, 2021 when it merged into special purpose acquisition company (SPAC) Social Capital Hedosophia Holdings Corp. V. Initial news of the proposed merger (in January 2021) sent the SPAC soaring 58% to $19.14 a share with SoFi’s opening trade later transacted at $21.97. This fintech currently trades just above $5.50 a share, equating to a market cap slightly over $5.2 billion.

Operating Segments

Although the company views itself as a full-service bank operating through an app, it is first and foremost a lender. It has three operating segments: Lending; Technology Platform; and Financial Services.

Lending. SoFi primarily provides three types of loans: Student; Personal; and Home. Even though the lender now has a bank charter, permitting it to hold its originations as long as it pleases, these loans are not held to maturity but rather held for sale and sold (typically) for a gain into whole loan or securitization channels. As such, the fintech does not provision for loan losses (save credit cards) as part of its financial statement algebra. However, the bank charter does provide it with incredible flexibility, including the advantage to fund its loans from its deposits, allowing it to offer higher rates on said deposits versus other non-chartered fintechs.

Its student lending operation is primarily refinances that target super-prime graduate school loans. However, this business line has been in a state of limbo since monthly payments of principal and interest were suspended on most student loans when the CARES Act was passed in response to the pandemic in March 2020. Executive actions by both the Trump and Biden administrations have extended the moratorium through June 30, 2023. Add in the August 2022 measure permitting the forgiveness of $10,000 of student debt for those earning less than $125,000 – blocked by a federal appeals court and awaiting a Supreme Court verdict (likely June 2023) – it’s not hard to envision the adverse impact to SoFi’s business model as loan wholesalers discount what they pay for any of its originations. Case in point: the fintech went from originating $2.4 billion of volume during 4Q19 (fed funds 1.65%) to originating less than $400 million in 3Q22 (fed funds currently 4.38%). It should be noted that if payments [EVER] resume, management believes that origination (even in this rate environment) will jump back to ~$2 billion per quarter.

That drop in student loans has been more than covered by SoFi’s uptick in personal loans, which are primarily for debt consolidation and home improvement purposes. After originating personal loans totaling $2.6 billion in FY20 and $5.4 billion in FY21, the bank originated $9.0 billion in the last 12 months ending September 30, 2022 (TTM22), benefitting from increased demand for debt consolidation products in a rising interest rate environment.

The bank also originates mortgages, although this business has been negatively impacted by those same rising interest rates that have lowered overall home loan demand and dried up the refinancing market, which is where SoFi predominantly operates. After originating home loans totaling $2.2 billion and $3.0 billion in FY20 and FY21 (respectively), SoFi saw that metric drop to $1.5 billion in TTM22. It is not strong in the purchase market – so look for that decline to continue.

Overall, Lending has generated 1.28 million loans in TTM22, resulting in a contribution (Adj. net revenue minus directly attributable expenses) of $560.3 million on Adj. net revenue of $1.0 billion, or 71% of SoFi’s total ($1.41 billion).

Technology Platform. The bank’s technology platform consists of Galileo, which provides card activation, authorizations, and processing, as well as card loads – and is primarily offered as a third-party service. It also manages debit and credit card programs issued by banks; thus, earning fees from the payment network. Although small, Galileo is a fast-growing segment, with a 40% jump in the number of accounts open (to 124.3 million) from September 30, 2021 to the same date in 2022. It generated a contribution of $79.6 million on revenue of $282.8 million (20% of total) in TTM22, after contributing $64.4 million on revenue of $194.9 million in FY21.

Financial Services. SoFi’s Financial Services segment provides mobile savings and checking accounts, digital brokerage services, and credit card offerings, collecting fees for brokerage, underwriting, payment network, and referral fees inter alia. Like Technology Platform, Financial Services is a fast grower but a very unprofitable one. It contributed a loss of $132.1 million on net revenue of $11.9 million in FY20 and a loss of $134.9 million on net revenue of $58.1 million in FY21. In TTM22, it has lost $191.0 million on net revenue of $124.8 million (9% of total).

Stock Price Performance

Selling the public on its vision of becoming a one-stop shop for financial services, SoFi generated significant investor interest before going public. However, after achieving an all-time high of $24.95 a share in its second day of trading, its stock has fallen by over 75% since – in the process, making it a battleground name within the investment community.

The reasons for the fall (and the debate) are manifold.

First and foremost, high-growth, no-or-low-profitability stocks suffer in an inflationary environment as higher interest rates significantly erode the net present value calculations of outer year cash flows: precisely the time when these stocks are going to ramp up their bottom lines. Curiously, the company does not provide an outlook for non-GAAP earnings, only Adj. EBITDA. With extremely high share-based compensation expenses ($0.26 a share in the first nine months of FY22), SoFi has lost $0.35 a share YTD22 on a GAAP basis. Put another way, share-based compensation was 21% of revenue for YTD22. Either way, with only about one-third of it rolling off in 1Q24, Street analysts don’t see the fin-bank reaching GAAP profitability until FY25, projecting it to lose $0.43 a share (GAAP) in FY22, followed by a loss of $0.26 a share (GAAP) in FY23 – not a great look in a risk-off environment.

Second, like so many SPAC-sponsored companies, SoFi management overpromised and underdelivered on its road show, projecting base case FY22 Adj. EBITDA of $254 million and $447 million if it were to attain a bank charter (achieved). On its 3Q22 conference call, the company is now calling for FY22 Adj. EBITDA between $115 million and $120 million. It goes without saying that this updated outlook obviously puts its original FY25 Adj. EBITDA forecast of $1.48 billion on revenue of $3.7 billion in jeopardy.

That said, management’s road show FY22 top-line forecast of $1.5 billion will likely be achieved with the bank now expecting Adj. revenue of $1.52 billion. However, with most Street economists calling for a recession as part of their FY23 forecasts, delinquencies on these loans could rise, either leaving SoFi with non-performing loans or at the very least commanding a much lower sales price to wholesalers, which will impact margins – or worse, generate losses on their sales. It is unclear if this scenario will play out and SoFi does have minimum purchase agreements in place with its wholesalers, but the perception that these loans could impact performance in FY23 creates multiple compression for the entire industry. Its internet consumer lending peers such as Ally Bank (ALLY) (FY22E non-GAAP EPS $5.99; FY23E $4.39), Axos Bank (AX) ($4.61; $5.03), and First Internet Bancorp (INBK) ($3.76; $2.24) are already profitable and have taken it on the chin, with all down substantially from their 52-week highs. Ally Financial did see its stock rally some 20% on Friday after posting better than expected fourth quarter results. However, a big part of that was improvement from the company’s insurance division.

Fourth, the bank has been hurt by the aforementioned student loan moratorium, rumors of accounting issues, and – since its members can invest in some digital assets – the FTX debacle. That said, management provided Congress with a breakdown of its de minimis exposure to cryptocurrency – $132.5 million of crypto-assets held by third-party custodians on behalf of its members – and zero to FTX in November 2022.

That leaves a would-be investor with an unprofitable company (on a GAAP basis) in a macro backdrop that should create headwinds to growth and profitability in FY23. However, with borrowers’ overall average FICO score 746, SoFi offers fintech and consumer finance exposure sans subprime risk. With its bank charter keeping funding costs low and its digital platform acting as a consumer funnel, it should benefit from the best of both worlds. In a brutal environment, the fin-bank has achieved six record revenue quarters in a row with eight consecutive quarters of positive Adj. EBITDA.

Balance Sheet & Analyst Commentary:

All that said, SoFi held unrestricted cash and investments of $1.13 billion against corporate debt (excluding warehouse and securitization facilities) of $1.69 billion as of September 30, 2022, for net leverage of 4.8 based on its forecasted FY22 Adj. EBITDA of $117.5 million.

The fin-bank is in solid shape regarding its Tier-1 capital ratios with SoFi Bank at 16.4% and SoFi Technologies at 24.2% (minimum requirement: 8.5%) on September 30, 2022. However, these ratios are down notably from 23.9% and 30.2% (respectively) on June 30, 2022. As such, it is worth keeping an eye on the retained earnings (or in the case of SoFi, “accumulated deficit”) line item each quarter. If it shrinks (or the accumulated deficit line grows), it will lower the Tier-1 capital ratios. Even if it stays at breakeven, without additional equity capital, a stagnant equity capital metric – the numerator in Tier-1 capital ratios – will eventually put a lid on how much SoFi can lend (the denominator).

Although there have been a couple of upgrades and Street sentiment is positive for the bank with six buy and three outperform ratings against five holds, no one offering commentary in the past six months has assigned a price target above $9 with a median price target of just over seven bucks. In addition to their forecasts for GAAP losses of $0.43 a share and $0.26 a share in FY22 and FY23 (respectively), they anticipate SoFi generating revenue of $1.53 billion in FY22, followed by $2.03 billion in FY23, representing a 33% improvement.

With uncertainty continuing to swirl about the fintech – even after its placative response to Congress – the recent $5 million investment by CEO Anthony Noto, consisting of just over 1.6 million shares from December 9th-16th, provided some confidence/relief for investors.

Verdict:

With no prospects for profitability on a GAAP basis until FY25 and an uncertain macro backdrop, there is not a lot to get excited about regarding this consumer financial technology concern, except for the fact that it possesses a nearly a complete solution set. Its stock has moved up off its all-time low (of $4.24) over the past month. Currently valued at an EV/FY22E Adj. EBITDA of approximately 50, the stock is still very expensive, the CEO’s significant insider purchase notwithstanding. There is significant premium in the very liquid option market, so if I was ever tempted to take a small position in this name in would be via covered call orders for downside mitigation purposes.

Countries that are defeated by their enemies often rebuild. But the countries that are destroyed from within—that’s really the end of the line.”― Stephen Kotkin

Be the first to comment