Roberto/iStock via Getty Images

Sibanye Stillwater (NYSE:SBSW) is an interesting topic going into 2023. The company suffered from an array of abnormal events in 2022, and its stock got caught up in the middle of a bear market, which didn’t find a liking to cyclical assets. With a potential stock market pivot in mind, we decided to assess Sibanye’s operational prospects going into the new year.

Furthermore, we considered the company’s future residual income and placed a valuation on the stock, providing a valuable juxtaposition.

Operational Update

It’s anticipated that Sibanye Stillwater’s prospects will improve in 2023 after a torrid 2022, which saw the company experience various externally induced events, namely labor disputes, floods, and electricity stoppages due to Eskom’s crisis.

However, let’s look at what this year holds for Sibanye.

Starting with the firm’s PGM endeavors in the U.S., Sibanye’s operations are back online after a seven-week delay midway through 2022. The company mines nearly 17% of its PGMs in the U.S. via its Stillwater mine and East Boulder. Additionally, the company operates a significant recycling business in the region, which adds value to its corporate portfolio via economies of scope.

Macroeconomic challenges and input cost pressures in the region remain. Nonetheless, a production ramp-up in 2023 is highly possible, which could outweigh any systemic challenges.

We anticipate Sibanye to focus on mining its existing U.S. capacity in 2023; however, expansion projects are likely to be delayed amid unwanted convergence between PGM prices and input costs.

Furthermore, the company is making significant strides in other jurisdictions. It recently raised its stake in the Keliber lithium project (Finland) to 85%. Additionally, its acquisition of Sandouville provides it with midstream Nickel interests in France, providing it with supply routes into Europe.

The company’s South African operations are at an inflection point. Starting off with a few risks, Sibanye has agreed to a wage agreement with AMCU. However, NUMSA (a more hostile labor union) is looking to exploit new territories, which remains a threat to the firm.

Furthermore, Sibanye’s disposal of its Beatrix and Kloof assets is proving a challenge, as South African deep Gold mines are less popular than they once were. Nonetheless, the firm’s exit strategy from high-cost assets is encouraging to see.

The good news for investors is that Sibanye’s South African PGM operations are incredibly well-located and provide a tremendously respectable return on capital invested. With proliferating EBITDA, it’s likely that Sibanye’s regional exposure to mines, such as Kroondal, Marikana, Mimosa (in Zimbabwe), and Rustenburg, will provide it with a competitive advantage over companies in higher-cost, lower throughput jurisdictions.

Yes, Eskom’s disruptions will likely compress the company’s margins, and the energy crisis is no longer an abnormal event (meaning current costs are the new base level). However, Sibanye has plenty of margin to work with and a substantial amount of capital to invest in self-generation.

Sibanye-Stillwater

Valuation

Residual Income Valuation Model

Model Output

As a natural resources company, Sibanye’s book value and cyclical cash flows should be emphasized from a valuation perspective. Thus, we used a residual income model to value its stock.

According to our model, Sibanye is fairly valued at an intrinsic value of $9.93, which is more or less in line with its current stock price ($10 handle). Moreover, a 10% margin of safety suggests that upper and lower valuation bounds aren’t outliers.

Author’s Calculations

Input Variables

The model was fitted with the following input variables.

The stock’s price was divided by its price-to-book ratio to discover a benchmark book value per share. Furthermore, Seeking Alpha’s database provided helpful earnings-per-share estimates; notice that the model’s 2026’s terminal EPS is a normalized average of the prior year’s inputs, reflecting the business’ short-term operating cycle.

EPS Estimates (Seeking Alpha)

As with EPS estimates, Seeking Alpha’s database was utilized to extract dividend per share estimates. The database didn’t provide an estimate for 2025; therefore, the company’s retrospective 5-y CAGR was applied for 2025; again, 2026’s dividend estimate was achieved by a normalized average.

Dividend Estimates (Seeking Alpha)

The “equity charge” was calculated by deducting the investors’ required return (CAPM) from earnings per share. The CAPM was converted into an absolute number by multiplying the percentage by the “beginning book value” of each year.

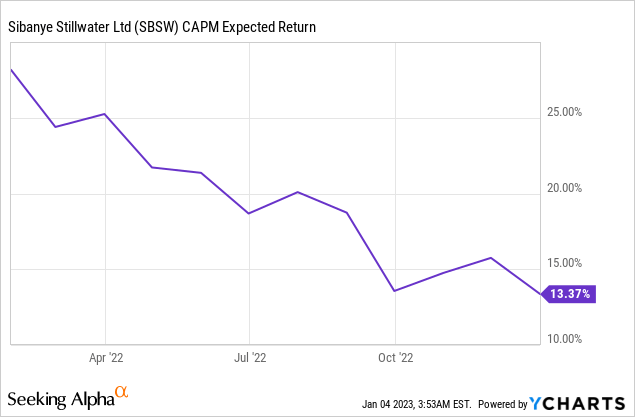

The incremental residual income was adjusted for the “time value of money” by discounting each ‘cash flow’ by its time-adjusted CAPM. As part of the valuation, 2023 to 2025’s residual values were considered at face value. However, 2026’s line item had to be adjusted to reflect a terminal value.

A persistence factor of 0.7 was phased into the CAPM for 2026, which increases intrinsic value based on our belief that the company’s long-term earnings will be resilient and remain above industry standard. After phasing in the factor, the number was discounted back to 2023 with a regular time-adjusted CAPM.

Lastly, the stock’s intrinsic value was derived by adding the firm’s current book value to its succeeding incremental residual income and the terminal value. Readers should keep in mind that any valuation model is subject to an analyst’s own vantage point and provides no guarantee.

Dividend Prospects

A big draw to Sibanye is its dividend profile. The stock’s dividend yield of 7.56% comes after a period of stable financial results, which occurred due to abnormal events. If Sibanye ramps-up production, its dividend could proliferate to a “best-in-class” level.

Furthermore, the firm’s dividend policy seems sustainable as it hosts an attractive dividend coverage ratio of 3.24, accompanied by an interest coverage ratio of 18.31.

Seeking Alpha

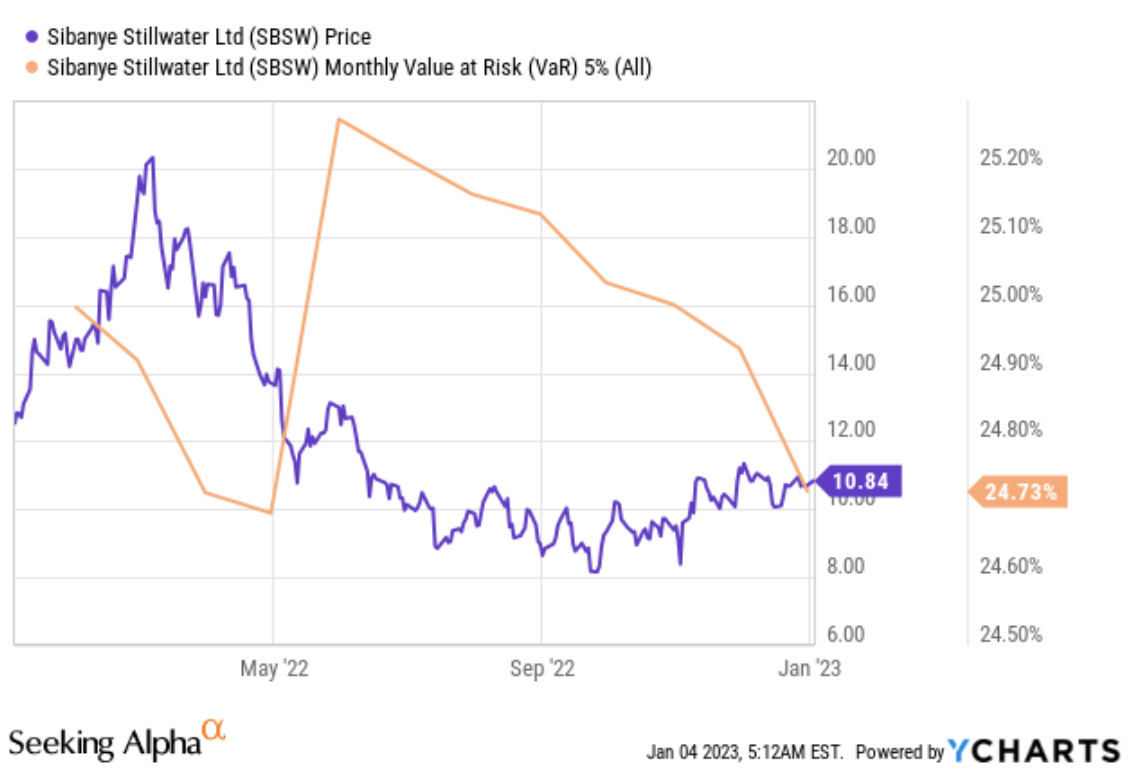

Despite its solid dividend profile, Sibanye hosts substantial value-at-risk, which could overrun its dividend payouts if the company (and the broader market) follows the same fortunes as in 2022.

Value-at-Risk (Seeking Alpha)

Conclusion – Hold Rating Maintained

Sibanye Stillwater will likely ramp up production in 2023 as key wage deals were settled in 2022. Furthermore, U.S. PGM operations are set to recover after an abnormal event, and vital renewable assets could come into play.

Despite the company’s improved prospects, its stock is fairly valued, and its extensive value-at-risk could overshadow its dividend distributions amid an uncertain macroeconomy.

We maintain our hold rating until further notice.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment