piola666

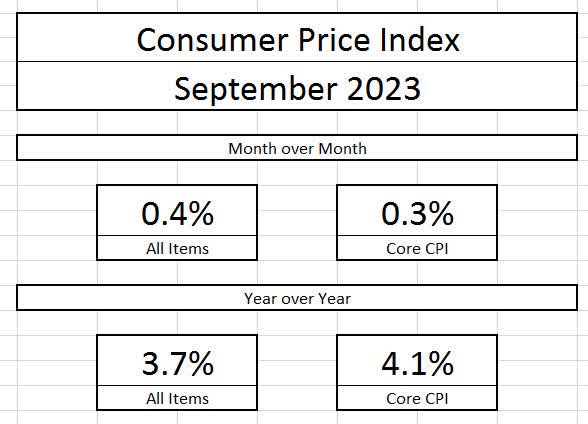

Earlier this morning, the Bureau of Labor Statistics released the Consumer Price Index for the month of September. On a year-over-year basis, inflation came in at 3.7%, while core inflation (which removes food and energy) came in at 4.1% year over year. While core inflation (on a year-over-year basis) is at its lowest level in two years, a deeper dive into the data is showing that the dis-inflationary trend has stalled, and the Fed may need to raise rates further.

Bureau of Labor Statistics Bureau of Labor Statistics

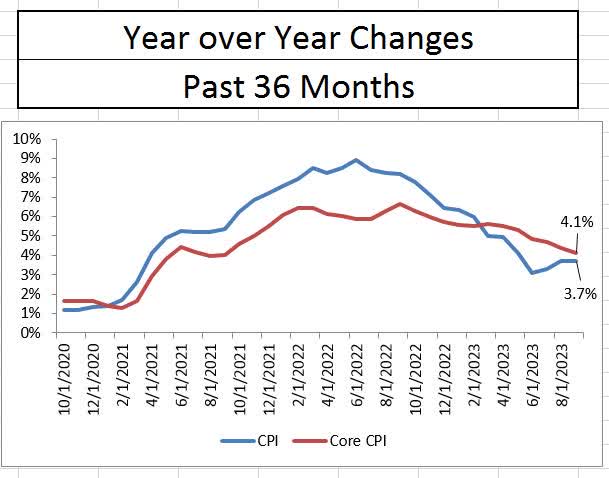

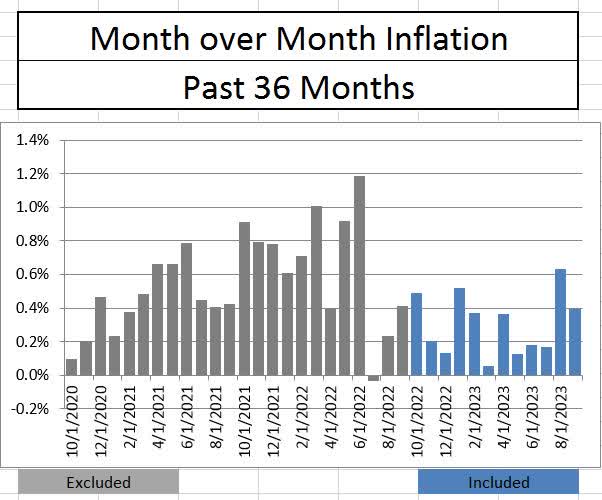

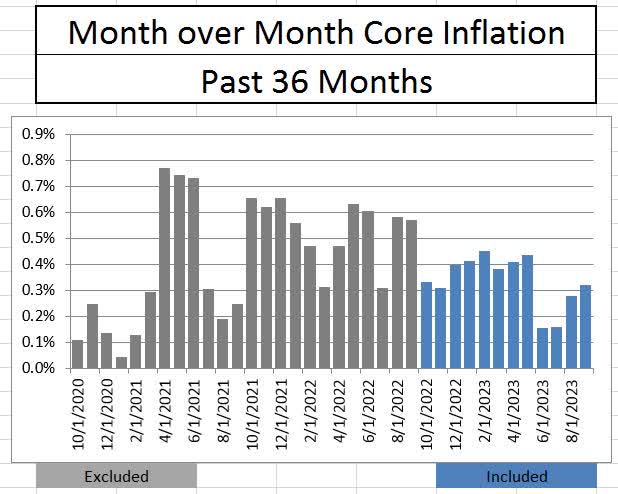

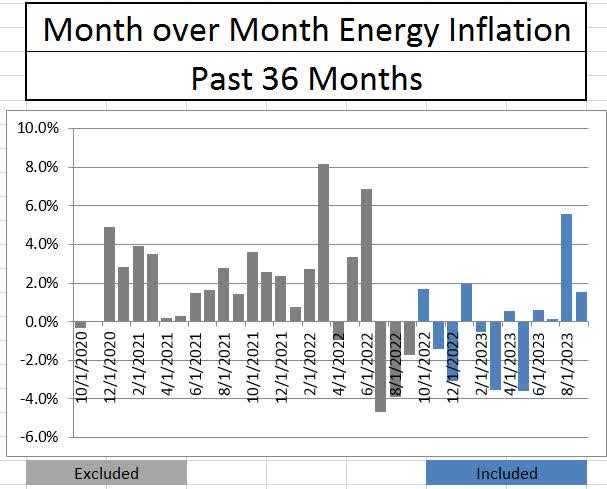

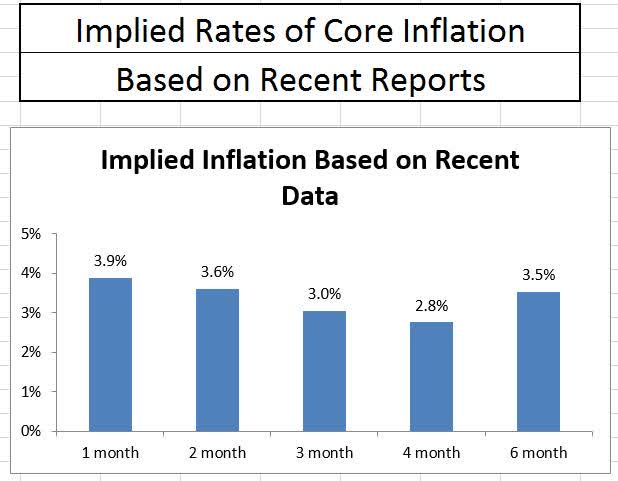

Analysts don’t need to go far to find the first signs of trouble. On a month over month basis, core inflation has continued to rise over the last two months with headline inflation also being elevated. While energy was a major influence in last month’s headline number, it was more subdued in September’s report. If we annualize the last two months of data, inflation is higher than the annualized total of the last four months. There appears to be a firm floor at 3.5% on a year-over-year basis, which may require higher interest rates to permeate through.

Bureau of Labor Statistics Bureau of Labor Statistics Bureau of Labor Statistics Bureau of Labor Statistics

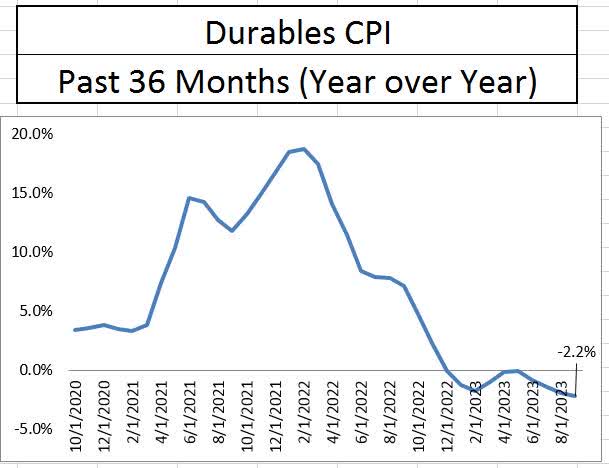

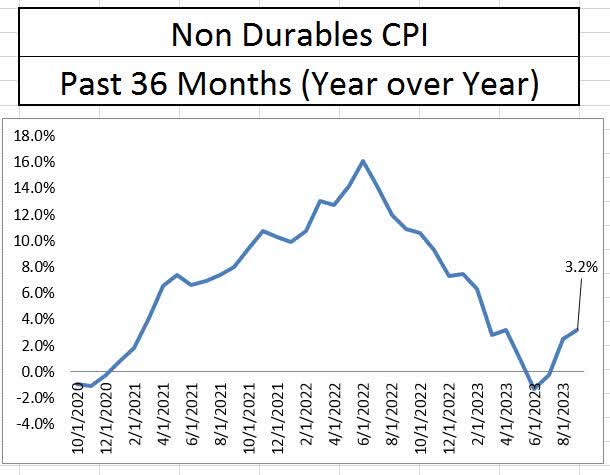

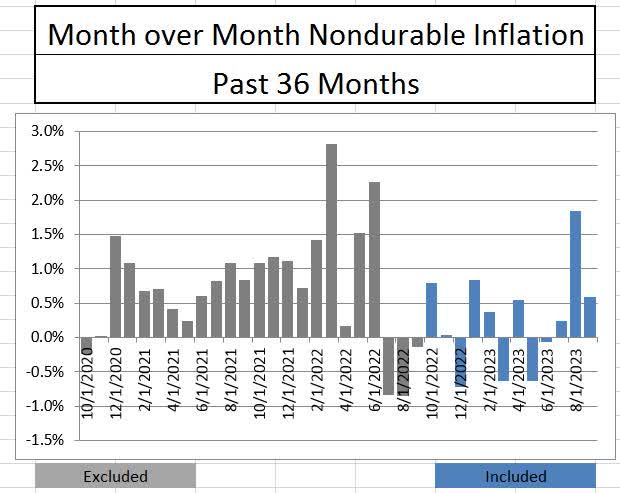

One silver lining to the report was in regard to durable goods inflation which continues to be deflationary (prices are decreasing), but the good fortunes of price stability stop there. Non-durable goods inflation has jumped in back-to-back months, strong enough to pull its year-over-year inflation from negative to 3.2%.

Bureau of Labor Statistics Bureau of Labor Statistics Bureau of Labor Statistics

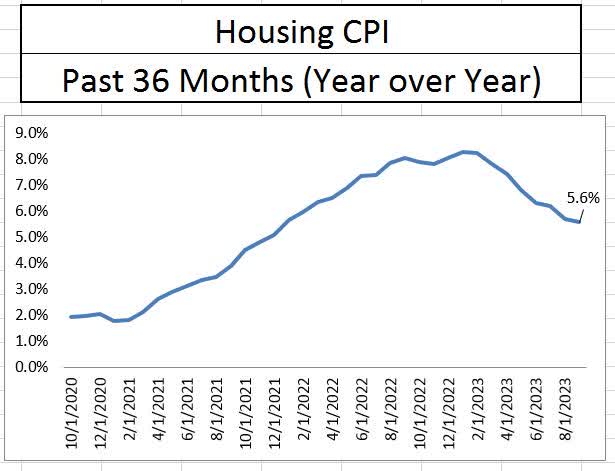

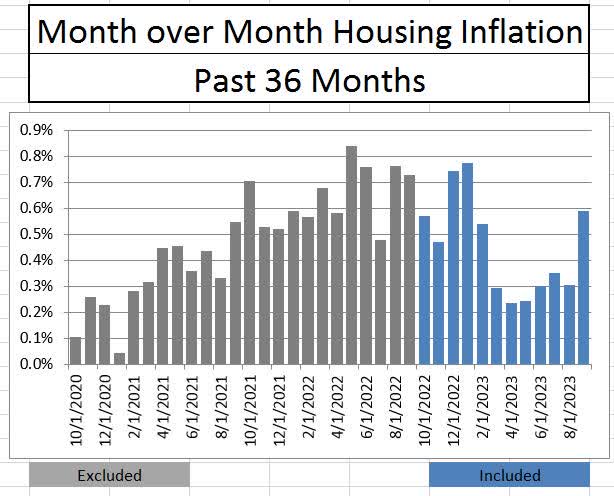

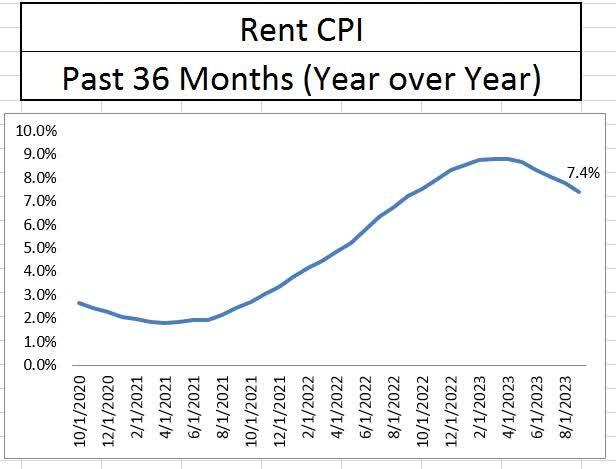

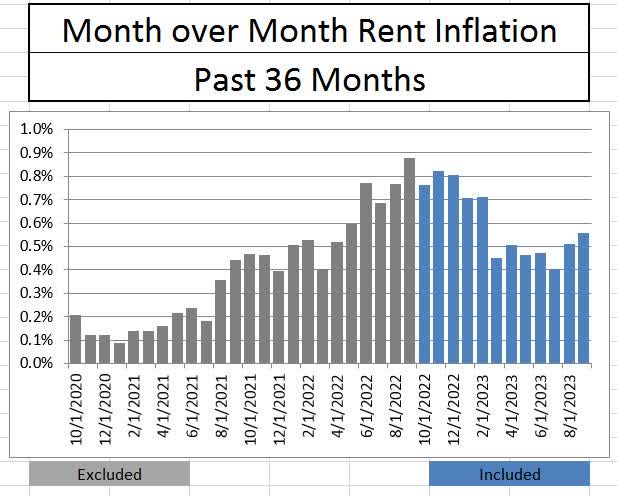

After goods, the “stickier” sectors of the economy also saw alarming price increases. Housing inflation slowed on a year-over-year basis for the eighth consecutive month, but on a month-over-month basis, housing inflation rose by 0.6%, the highest monthly reading since January. Rent pricing showed a similar trend to housing with year-over-year pricing slightly decelerating and the month-over-month increase rising at the fastest pace since February.

Bureau of Labor Statistics Bureau of Labor Statistics Bureau of Labor Statistics Bureau of Labor Statistics

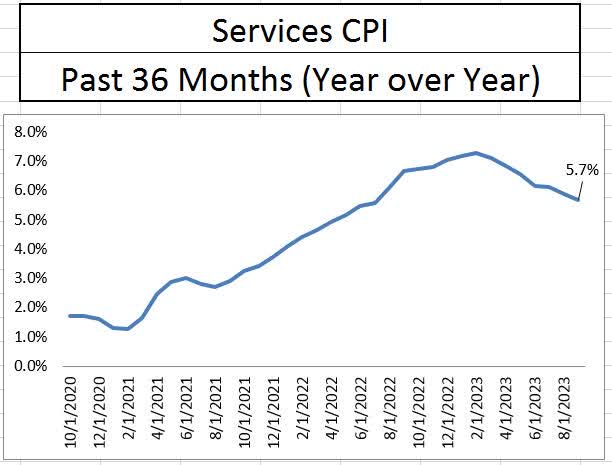

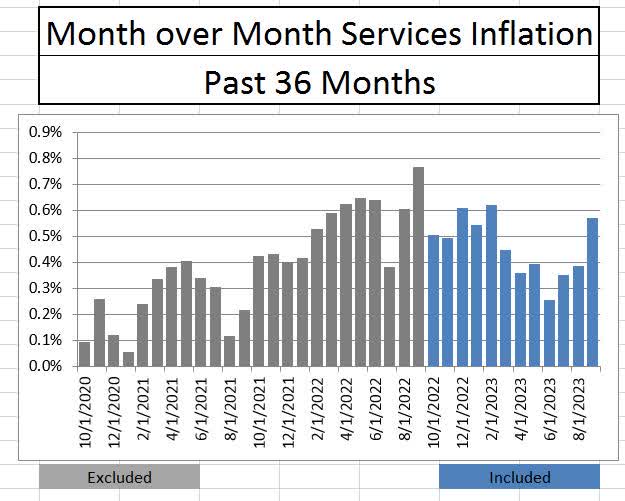

Services, which is considered one of the largest and most stubborn pricing metrics, also saw its pricing break the dis-inflationary trend in September. On a year-over-year basis, services pricing slowed to 5.7%, but on a month-over-month basis, prices rose by 0.6%, the highest month-over-month level since February. It’s important to note that services account for 45% of total GDP in the US economy, twice the size of goods.

Bureau of Labor Statistics Bureau of Labor Statistics

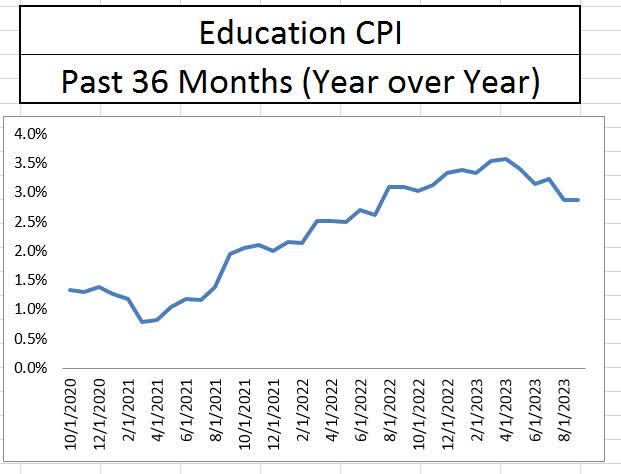

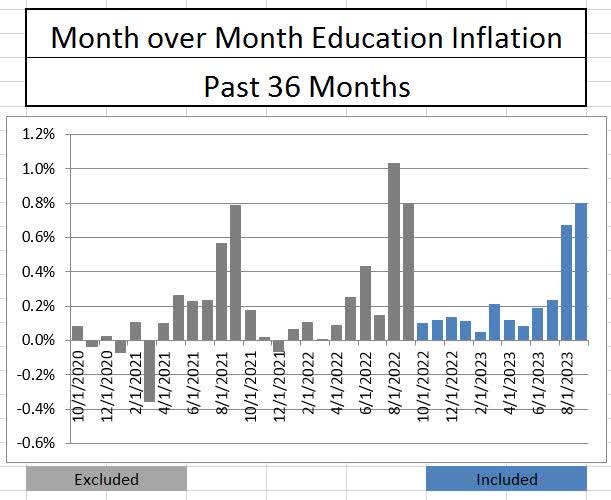

Even sectors of the economy that appeared immune from the pandemic era quantitative easing regime saw notable price increases in September. Education, which saw an inflation rate year-over-year peak at a modest 3.6% in April, has recorded month-over-month increases of 0.7% and 0.8% in the last two months, respectively. It is granted that August and September appear to be the catalyst months for full year pricing of education, but the last two monthly increases were above those of the same months of 2021.

Bureau of Labor Statistics Bureau of Labor Statistics

It is reassuring that the Fed has kept an additional hike in its back pocket, because it appears likely to get used in its November meeting. While there is hope that the 50 basis point increase in long term rates over the past few weeks may do the Fed’s work for it, I’m not sure the Fed is willing to sit back and wait for the data to worsen before acting.

Federal Reserve

At this point, I am expecting the Fed to act on its rate hike forecast in the November meeting. Service sector inflation, being such a large part of the economy, is running way too hot. Additionally, investors should brace themselves for the Fed to project a hold through 2024 or possibly another increase and hold when it meets and re-issues its forecasts in December. The implication of inflation once again picking up steam is going to continue to fuel higher interest rates in the debt markets and consequently, a possible increase in volatility for the equity markets.

Be the first to comment