BlackJack3D/iStock via Getty Images

After benefiting consistently since the summer bear market rally, shares of SentinelOne, Inc. (NYSE:S) are now trading basically at an all-time low, which might constitute an opportunity for long-term shareholders. After hitting around $20 per share on May 11, the stock performed quite well until early October, up about 40% since the previous low. After that, however, the shares only went down, until today’s price of about $13.28 for a market capitalization of $3.7 billion. Having come to the market in the second half of 2021, basically, anyone that ever purchased shares of S in the public market is probably now in the red; as demoralizing as it is for current shareholders, that seemed a good starting point to review the cybersecurity provider. Despite promising a lot, investing today is inherently risky due to the company’s unprofitable state.

Third Quarter 2023 overview

SentinelOne operates in the increasingly interesting field of cybersecurity, arguably a sub-sector of IT that should in theory suffer less in a recessionary environment. When tightening the belt, it is easy to imagine that many companies might decide to cut budgets devoted to marketing or research, however, protecting their systems from cyberattacks is rapidly becoming a systemic necessity for all sorts of businesses. Thanks to this, SentinelOne continues to grow at an impressive scale even when many other IT businesses are not only slowing down but are also shredding their workforce to operate more nimbly.

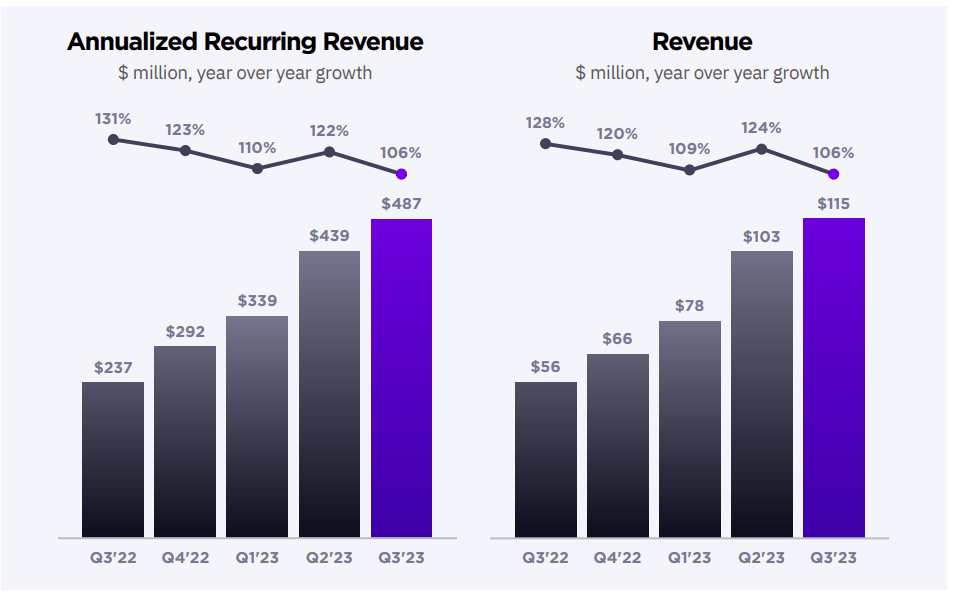

SentinelOne published the results of its third quarter 2023 on December 6: headline numbers were quite impressive, with Revenue increasing 106% year-over-year to $115.3 million and total customer count up 55% to over 9,250 customers. Even more impressive is that the big-spending cohort grew much faster than the rest: customers spending over $100,000 annually doubled from a year ago to 827, while those spending more than 1$ million grew even faster, although no precise figures were provided by management. Put in perspective, the latest quarter was the seventh consecutive quarter of topline triple-digit growth, helped by a very high Dollar Based Net Retention Rate (“DBNRR”) of 134%, meaning that existing customers spent on average 34% more during the quarter compared to the past.

SentinelOne Shareholder Letter Q3 2023

As clearly visible from the slide above shared by management in the latest Shareholder Letter, the growth rate of both Annualized Recurring Revenue and GAAP Revenue is quite clearly slowing but remained extremely elevated nevertheless.

Management has highlighted how SentinelOne is not immune to the broader economic sentiment, despite operating in the resilient cybersecurity sector. In particular, sales cycles are much longer than in the past as customers are much more prudent and nimble when allocating their IT budgets. Management still believes that SentinelOne’s Singularity platform is addressing one of the biggest needs of enterprise customers, which is to have a single cost-effective product addressing the need to endpoint security, identity security, and cloud security. I believe that revenue growth and high DBNRR are definitely indicative of how mission-critical SentinelOne’s products are, and how much value they add to their customers.

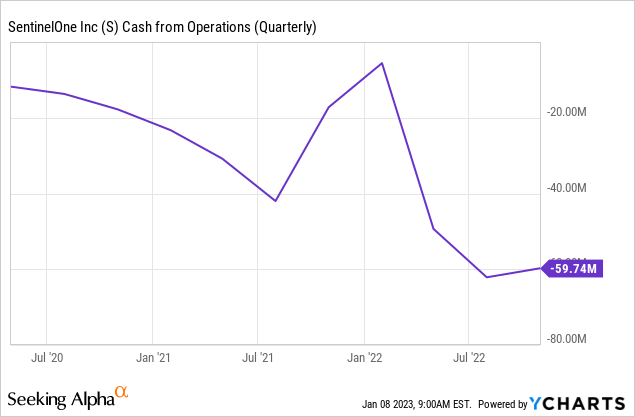

On the cash flow side, SentinelOne is still generating negative cash from operations quarter over quarter, with losses increasing quite consistently over time. The latest quarter saw the business losing about $60 million from operations, down from negative $17.2 million a year ago. This goes a bit in contrast to what management has highlighted during the call in relation to the path to profitability: when answering questions from analysts, management explained that they expect to generate positive Free Cash Flow somewhere around the end of Fiscal Year 2024 (which is calendar year 2023), just about 4 quarters from now. I like the idea of seeing the business start to generate positive free cash flow soon, however, unless the trend of accelerating cash flow losses will revert quite quickly I don’t see how this target can be met. Definitely, something to monitor closely for next quarters, to gauge how effective management is to predict how the business can leverage its scale.

Seeking Alpha – YCharts

Path to profitability

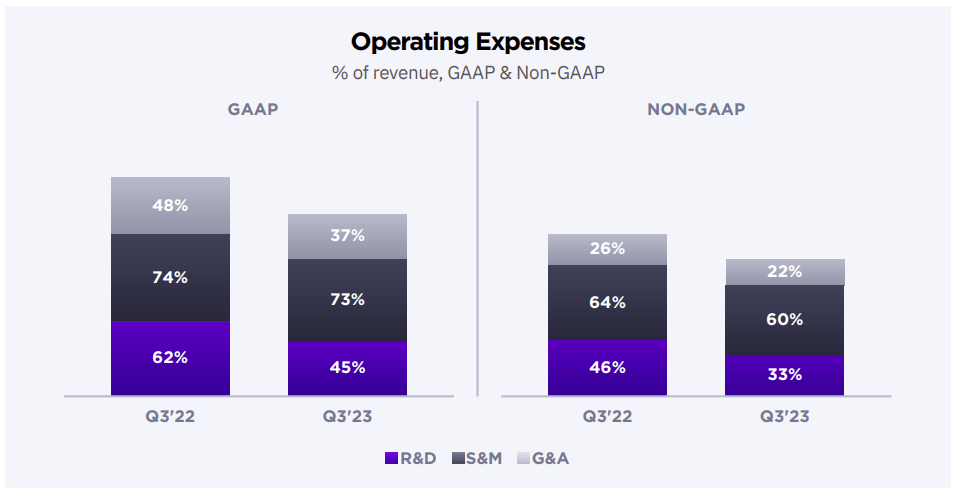

In the Shareholder Letter for Q3 2023, management has provided some information on the company’s path to profitability. If guidance will be met for the next quarter, the 4Q 2023 will be the sixth consecutive quarter of at least 25% improvement in non-GAAP operating margin, which is definitely welcomed news. On a GAAP basis, the latest quarter saw gross margin improving only 0.7 YoY (while on a Non-GAAP basis, the improvement was much higher, about 5%); however, GAAP operating margin still expanded 30% year over year, hinting at some operating leverage taking shape. Total operating expenses in the latest quarter (including Stock-Based Compensation) were $178 million, up 73% YoY, which is much less than revenue. The reasons for the increase are largely due to an increase in headcount, up 75% YoY: SentinelOne is obviously in growth mode, and with such a high growth rate and an expanding total addressable market, it is hard to blame the management for trying to capture a large share of it as fast as possible.

SentinelOne Shareholder Letter Q3 2023

I see a lot of positive early signs that have to be monitored over time. The business operates on extremely low CapEx needs, which means that SentinelOne will start to generate Free Cash Flow consistently as soon as cash from operations turn positive. Management seems very focused on reaching their target of FCF by FY2024, and operational break even in FY2025. However, investors have to take into consideration dilution: as seemingly every growth company in the IT sector, SentinelOne relies extensively on Stock-Based Compensation (“SBC”) to remunerate its growing employees. This directly translates to shares dilution: SBC grew 67% in the latest quarter to $45.7 million (39.6% of total Revenue), while Total Shares Outstanding grew almost 6% YoY, which is relatively high and is actively working against shareholders’ returns.

One reason why shares are down so much in the past few months could be related to a comment made by management during the call in relation to guidance for next year. Annual Recurring Revenue is expected to grow around 50% YoY, which is basically half of the current rate. Revenue should also follow suit as in SentinelOne’s case the two metrics go pretty much hand in hand. Clearly, no company can grow at over 100% forever, however, that is quite a fast deceleration that might have spooked some investors.

Valuation and key takeaways

As it’s the case of any unprofitable growth stock, attempting to value the company can be extremely tricky. In absence of earnings or free cash flow, investors have a lot of promises to work with while real data is lacking. Granted, in SentinelOne’s case the promises appear quite enticing: with a fortress balance sheet of $1.2 billion of liquidity and triple-digit growth rate (albeit slowing), the company seems really well positioned to come out very strong from the potential recession that everyone is expecting.

Currently, shares are trading at Enterprise Value to Sales (TTM) of 8.52, which is not cheap but does not seem excessive to me for a business growing this fast. Wedbush analyst Taz Koujalgi published a note on December 15 valuing the company at an estimated FY2025 EV/Sales of 4, which roughly means that ARR is expected to double from the current $500 million to about $1 billion. That does not seem too far-fetched, but SentinelOne’s valuation will still depend largely on market sentiment, and there is no guarantee that it will change any time soon.

In my opinion, SentinelOne is a great promise and could very well grow to be a great company in the future. I don’t see anything wrong in even initiating a very small position at today’s price based on how great its potential is; however, a lot can go wrong when relying solely on promises, and for this reason, I don’t feel comfortable investing in the company yet. However, I believe the next few quarters will say a lot: if operating cash flow will quickly move towards parity and if operating expenses will still grow slower than revenue, I will re-consider and potentially invest. It will also depend on the price at the time, of course.

Be the first to comment