Prostock-Studio/iStock via Getty Images

Shares in Sea Limited (NYSE:SE) have fallen more than 85% in the last year. Thanks to this slump, SE is trading at a historically low valuation right now. The company has a good balance sheet and operates in growing sectors. Over the next few years, Sea is expected to grow sales by more than 20%. But there are also risks to bear in mind. Overall, I think that investing in Sea brings with it a high risk, but also a high reward.

About Sea

Sea Limited’s mission is “to better the lives of consumers and small businesses with technology.” The company was founded in 2009 by Forrest Li, who is still CEO today and who owns 8.22% of the entire company. That’s something I’m glad to see since it’s in his personal interest that Sea will be successful in the long run.

Sea Limited has 3 business segments. E-commerce: Shopee, Digital Entertainment: Garena, Digital Financial Services: SeaMoney. Now let’s take a look at each one.

Shopee is southeast Asia’s leading online shopping platform, offering convenient shopping to users who want to shop anytime and anywhere. Shopee was founded in 2015 and is very similar to Amazon (AMZN) and eBay (EBAY).

Garena is a developer and publisher of online games. Garena has games such as Call Of Duty or Free Fire, which was the most downloaded mobile game in 2019 and had over 150 million daily active users in 2021. Garena was founded in 2009 and is a prime business segment of Sea.

SeaMoney is a leading and rapidly growing provider of digital payments and financial services in Southeast Asia. SeaMoney was founded in 2014 and is quite similar to PayPal (PYPL). These are Sea’s 3 business segments.

Why Is The Stock Down Over 85% In The Past Year

There are several reasons why SE shares have fallen so much. I’d like to introduce you to those now. The first is the fact that a year ago, the company’s stock was vastly overvalued. A year ago, the company traded for a Price/Sales of 20x over the current Price/Sales of 2.4x. Here you can see for yourself how quickly everything can turn in one year. Expectations were simply too high, and so were valuations, which is the first reason SE shares fell so much.

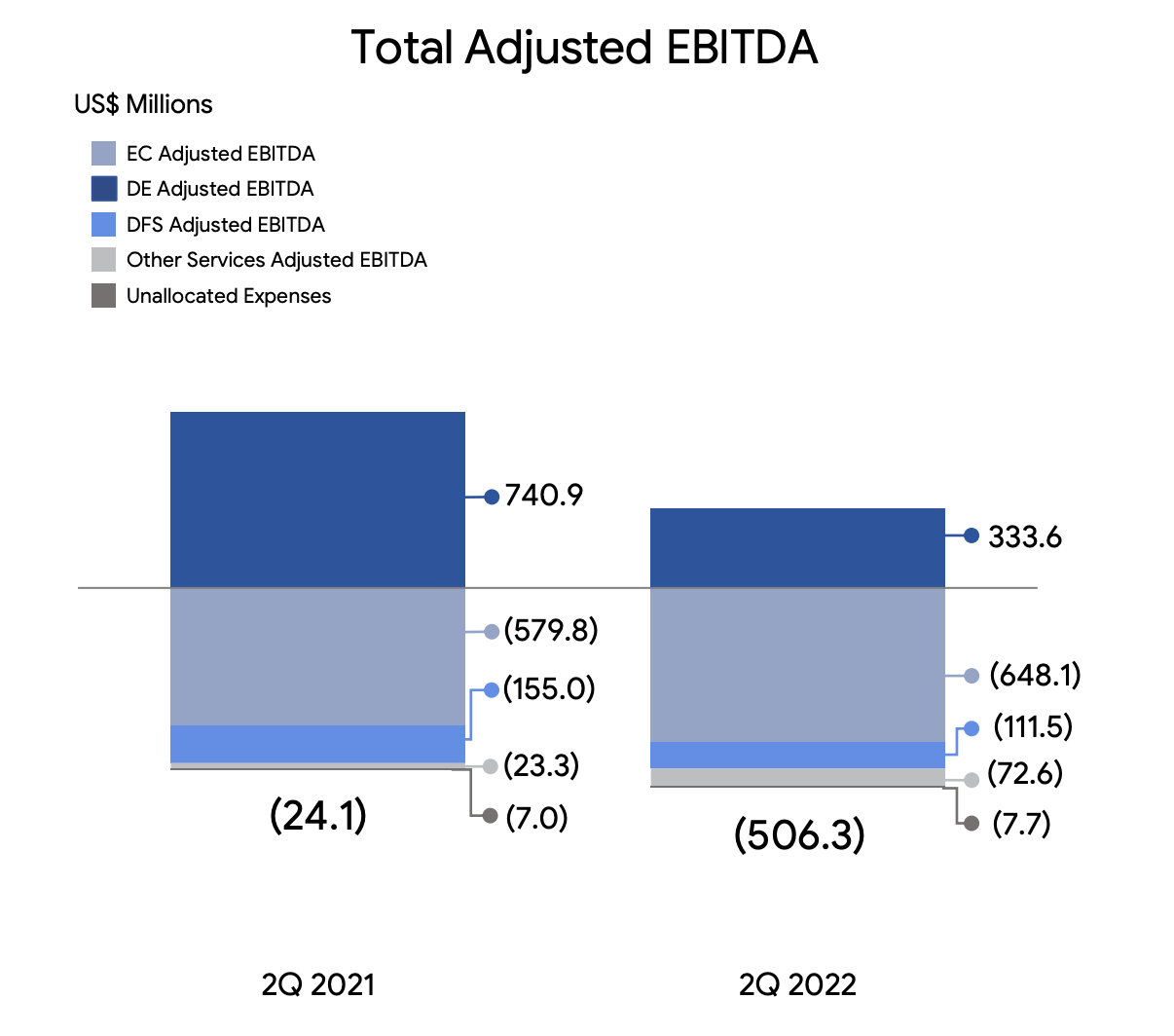

Another reason is that the macroeconomic situation is generally bad. This is not only bad in the US, but almost everywhere in the world. There is also high inflation in countries where SE operates. That’s why interest rates are going up there, too, and that’s definitely not good news for a still-for-profit business like Sea. As a final reason, there is Sea’s most profitable business segment yet, namely Garena. The fact that Garena is the most profitable business segment of the company so far is a very key sentence since Garena’s profitability over the last year, looking at Adj. EBITDA plummeted by more than 50%. And that’s a real problem for the company, since Garena is the most profitable segment of the company so far, helping to finance the growth of the nonprofit Shopee and SeaMoney. But what are the reasons for this big drop in Garena’s profitability?

The first is a ban on the most popular mobile game of Garena – Free Fire in India. India may not have been so important to Garena yet, but it could have been a country where the company could continue to grow. And the second reason is the trend that exists worldwide and that is the decline of gaming relative to the pandemic years 2020 and 2021. Because people don’t have to spend as much time at home anymore they, therefore, don’t have much time for gaming as they have in the last two years. This is why companies like Garena see much lower profitability figures this year than last year.

The biggest problem for Garena was the fact that quarterly active users were down -15% YoY and quarterly paying users were down -39% YoY in Q2 2022, which is really bad. That’s what made DE bookings down -39% YoY to only $717 million in Q2 2022. Those are really bad numbers, and probably the biggest reason SE shares have fallen so much in the last year.

Total Adjusted EBITDA SE (Q2 2022 Investor Presentation)

Future Growth Of Sea

Now let’s focus on the strategies that SE is likely to use for further growth. There really are plenty of opportunities for growth. The first one is more games in Garena. The company will continue to try to create some more popular games like Free Fire now. If they succeed, it may well support the company’s continued growth. Even though gaming hasn’t done as well this year as it has in the last two years. The gaming industry will continue to grow in the long run and SE with it.

Another opportunity for the company to grow is the launch of Shopee in more countries. Right now, Shopee is available in 13 countries. And Sea certainly plans to increase that number in the coming years. Shopee will then continue to grow in these countries and this, in my opinion, will greatly support the growth of the whole company.

Perhaps SeaMoney is the biggest current opportunity for Sea’s growth. SeaMoney has 52.7 million quarterly active users in Q2 2022. That number grew by a whopping 53% YoY. That’s really fast growth. The Total Payment Volume for Mobile Wallets was $5.7 billion in Q2 2022, an increase of 36% YoY. In my opinion, SeaMoney has enormous potential to become a large and highly profitable segment of the entire company.

These are some of the opportunities for growth that Sea currently has. It should be added that it is possible that in the future Sea may add some additional segments, as it has done in the past.

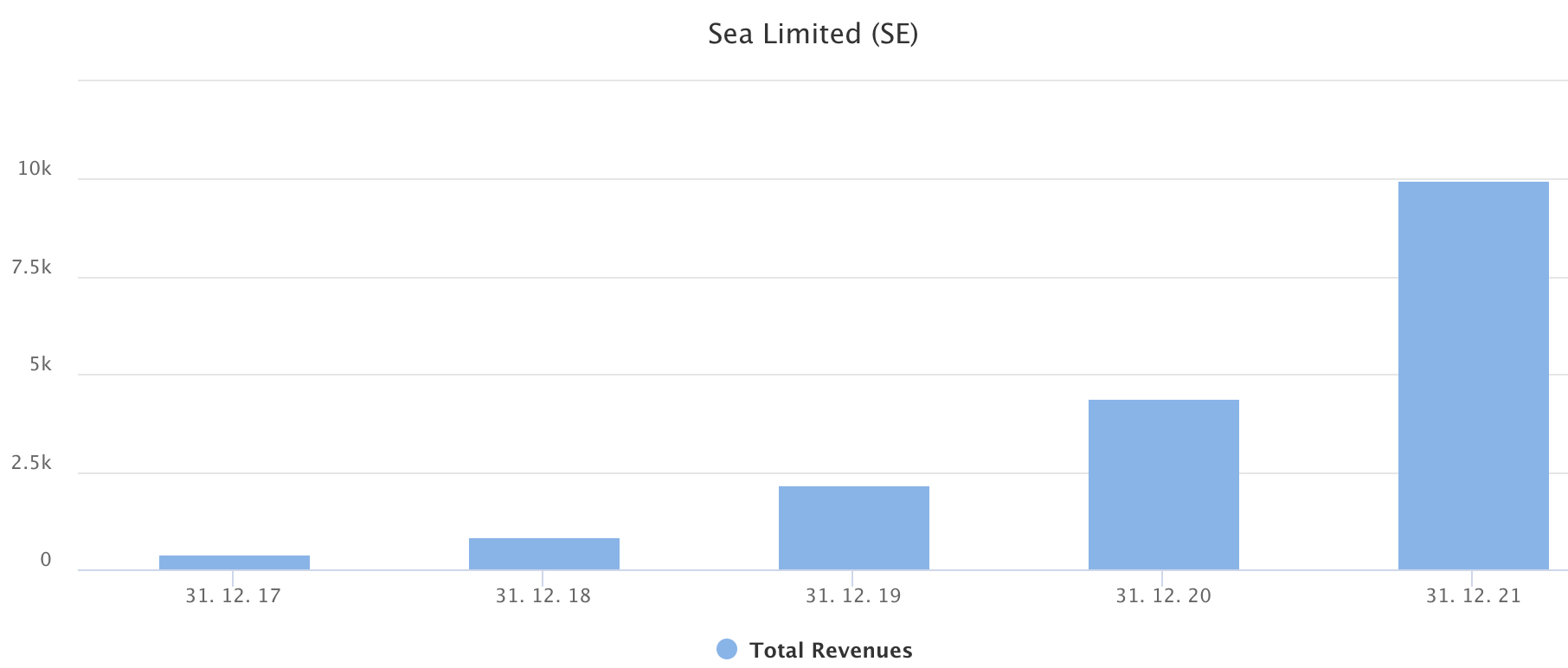

Revenue Growth Of Sea 2017-2021 (tikr)

Financials

Sea’s financials are currently in order, but it should be added that they are not as well off as they have been in the last two years. In Q2 2022, the company had revenue of $2.942 billion. That’s an increase of 29% YoY. Gross margins were 37% in Q2 2022. SE lost $931 million in net income in that quarter, more than double the loss from the same quarter last year. This was also one of the reasons why the company’s shares fell so much.

The balance sheet of the company remains ok. In Q2 2022, the company had $7.780 billion in cash and $17.467 billion in total assets. Right now, the company has $4.177 billion in long-term debt and $12 billion in total liabilities. As you can see for yourself, there is likely nothing to worry about when it comes to the balance sheet of Sea. The total equity of the company is currently $5.434 billion, therefore trading at a Price/Book of 5x, which is quite a bit lower than it was last year.

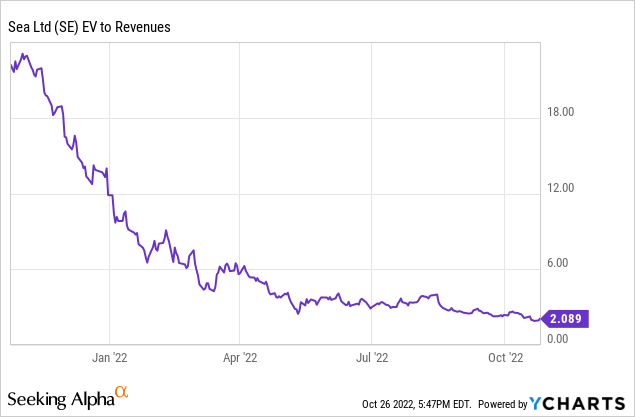

The Lowest Valuation Ever

SE is currently trading at the lowest valuation at which it has ever traded. The company’s current EV/Sales is 2x. That’s very low. EV/Gross Profit is now 5.5x. This is definitely not an expensive valuation in the long run. The problem is that SE is not currently profitable and this is not expected to change until 2025.

In 2025, analysts estimate that the company will be profitable. Analysts estimate the SE will have an EPS of $3.91 in 2025. So the company would now be trading for a forward 2025 PE of 13x. This seems cheap at first, but I personally take these estimates with a large margin for error, as it is highly likely that they will not materialize.

While valuation at first seems very cheap in the long run, we have to remember that the company is not profitable, and it is still estimated that it will not be for at least 3 years. This is something that should be kept in mind by the investor in the current macroeconomic situation.

Risks

Now, I’d like to tell you the main risks involved with investing in Sea. Perhaps the biggest risk Sea has now is competition. SE has plenty of competition in all three segments of the company. Shopee’s main competitors are Lazada (BABA), Akulaku, and Bukalapak. Garena’s main competitors are Xindong Network, Playrix, and IGG. SeaMoney’s main competitors are LianLian Pay, PayMe, and Paymark. As you can see, Sea has a lot of competition, and that’s a big risk the company currently has. Even though SE is currently the leader in its industry, there is a need to keep a close eye on the fact that it keeps improving its 3 business segments. This is the key to the long-term success of SE.

As an added risk there is no profitability for the company. This is certainly, in the current macroeconomic situation, a fact to consider. Over the next two years, analysts expect the company to have a loss of more than $1 billion. Yes, analyst expectations certainly need to be taken with a grain of salt, but it’s still something investors should consider. These are the two main risks associated with investing in SE.

Conclusion

Sea is a fast-growing company, which is unfortunately negatively affected by the current macroeconomic situation. The company has a balance sheet in perfect order and trades at a historically low valuation. However, it has risks that need to be carefully weighed before any investment is made. Personally, I think Sea is a company that can generate returns for long-term investors, even in the hundreds of percent if the management manages to turn this business around to profitability. But Sea is not without its big risks. That’s why I think Sea offers high risk and also high reward.

Be the first to comment