phaisarn2517

Since its spinoff from XPO and starting to trade as a standalone publicly-traded company on November 1, 2022, RXO Inc. (NYSE:RXO), which is a provider of full truckload freight transportation brokering services via its proprietary digital marketplace, has, after stripping away the first few days of trading which were typically volatile of a newly listed company, been trading in a fairly tight range.

After the first several days of trading it has found a bottom at approximately $16.00 per share, and a top of a little over $19.00 per share.

The company traded for a couple of weeks at $18.00 per share to $19.00 per share, before starting to pull back on December 2, 2022, eventually falling to slightly under $16.00 per share on December 22, 2022, before leveling off.

From that time to today it has once again been trading in a tight range, this time from approximately $16.50 to $17.50 per share.

My point in pointing out these details concerning its share price is, I think the price movement reflects the uncertainty of the impact of macro-economic conditions on the trucking industry in the near term, and by extension, on RXO. The long-term prospects for RXO look good, but in the near term, if the market turns against them, which is expected to in 2023, there would be a much more favorable entry point than where the stock is trading at today.

In this article we’ll look at some of its recent numbers, the near-term prospects of the company, and why it’s future looks bright.

TradingView

Some of the numbers

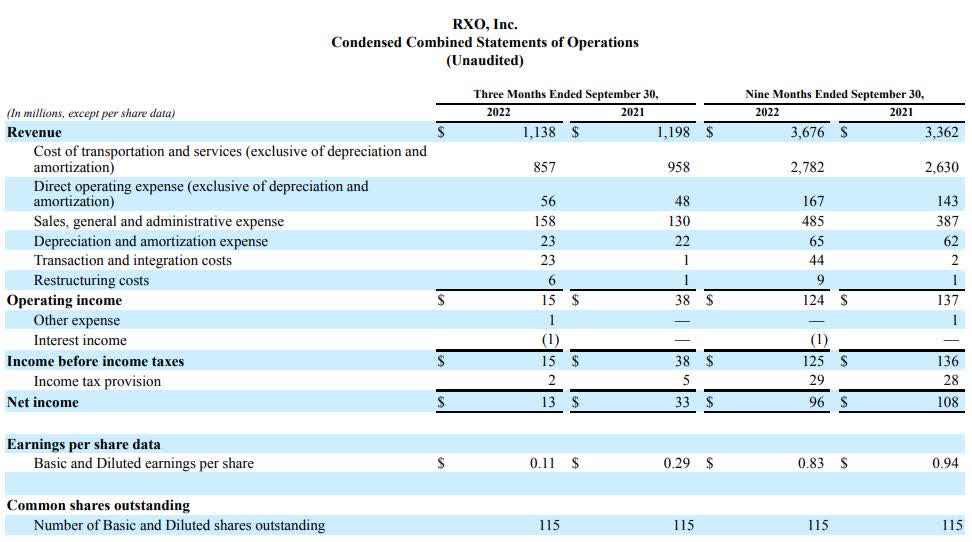

Revenue in the quarter ended September 30, 2022, was $1.14 billion, down from revenue of $1.2 million in the same quarter of 2021. Revenue in the first nine months of 2022 was $3.7 billion, compared to revenue of $3.4 billion in the first nine months of 2021.

Operating income in the quarter was $15.00 million, compared to operating income of $38.00 million year-over-year. Operating income in the first nine months of 2022 was $124.00 million, compared to operating income of $137.00 million in the first nine months of 2021.

Net income in the quarter was $13.00 million, or $0.11 per share, compared to net income of $33.00 million, or $0.29 per share in the same quarter of 2021. Net income in the first nine months of 2022 was $96.00 million, or $0.83 per share, compared to net income of $108.00 million, or $0.94 per share in the first nine months of 2021.

Cash and cash equivalents at the end of the quarter were $187.00 million, compared to cash and cash equivalents of $29.00 million at the end of calendar 2021.

Company Form 10-Q

Even though one quarter doesn’t a trend make, when combined with macro-economic concerns and freight issues, it could be pointing to a slowdown in the trucking industry that would have an impact on RXO’s short-term performance, by which I mean through most of 2023.

Its tech advantage

In an industry that has a growing demand for technology and data as supply chains get more complex, RXO stands out amongst its peers. The current fragmented nature of the trucking industry also lends itself to the need to streamline operations.

I believe the sector offers a long-term secular market opportunity, which RXO is uniquely positioned to take advantage of in the years ahead.

Included in the company’s proprietary technology, is AI, machine learning and pricing algorithms that generate faster execution and the optimization of prices.

As the company’s tech continues to improve, it’s going to be increasingly hard for most of its competitors to compete at that level.

In that regard, the company has enjoyed above-market growth and margins that are superior to its peers, which I believe is the direct result of its tech-enabled digital platform.

Headwinds

In the near term RXO faces similar headwinds other companies face at the macro level, including an economy under stress, rising interest rates, and lack of clarity as to the depth and length of the recession going forward.

As to industry-specific headwinds, they are reflected in cyclical freight pressure and weakness in truckload prices, which were down 2 percent in North America, to $686 million. This was the result of lower spot prices.

My opinion is spot prices are going to remain under pressure in the near term, which when combined with freight headwinds, is probably going to weigh on the performance of RXO, when combined with what appears to be a slowdown in revenue growth.

As mentioned above, the last quarter doesn’t mean a downward trend on the sales and earnings side has emerged, but when taken together with other weak metrics mentioned earlier, it definitely points to that being a strong probability.

A couple of things could offset some of the negative trends, including the fact that while spot prices were on the decline, trucking brokerage volume had increased. If spot prices rebound in 2023, and trucking brokerage volume were to continue to grow, then the company could surprise to the upside, performing contrary to my thesis that macro-economic and sector headwinds will determine its 2023 performance.

Another potential tailwind in these tough times could be its variable cost structure, which allows it to be flexible in response to changing market conditions.

Conclusion

I think the long-term future of RXO is going to be a good one, and should reward shareholders that hold on to their shares.

On the other hand, it’s my belief that macro-economic and sector headwinds are going to have more of an impact on the company than some of the tailwinds the company has at its back.

With the latest quarterly numbers pointing to weakening demand in revenue and earnings, it appears to me this is the first sign that company is going to participate in the down cycle that will last for most of 2023.

For that reason, I think there will be opportunities to find a superior entry point for those wanting to open a position in RXO. And for those already in the company, it should offer the chance to lower the cost basis in the quarters ahead.

Even though I’m more bearish in the short-term concerning RXO, there’s no denying it has the tech and digital platform to make a significant dent in the trucking industry, and for those wanting exposure to the sector, RXO offers a good chance at strong gains over the long term.

Be the first to comment