imaginima

All data are Canadian funds.

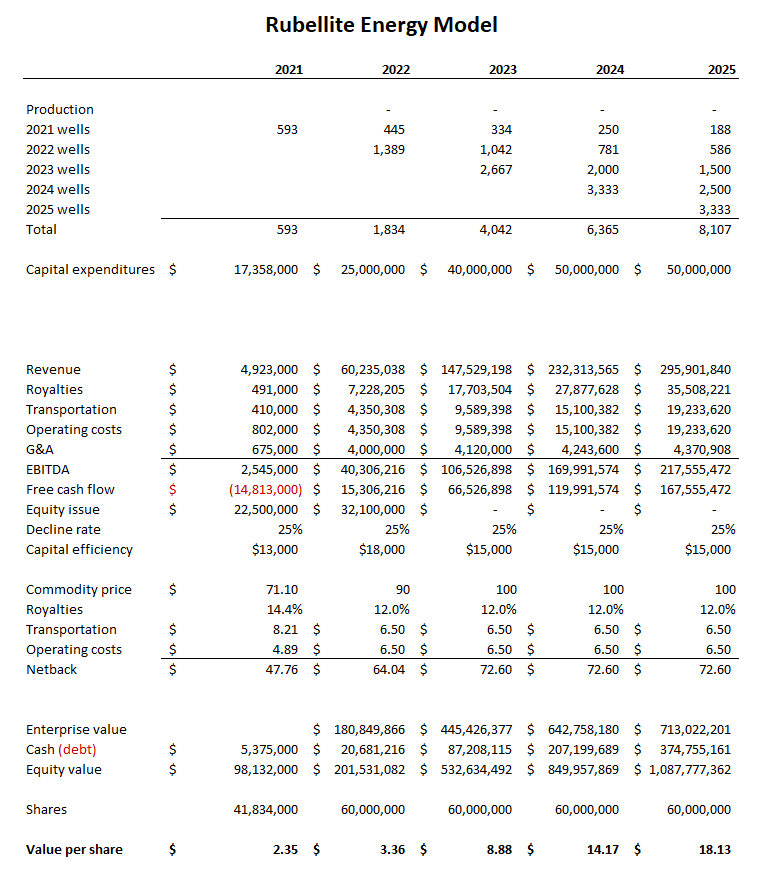

I was lucky enough to buy some shares of Rubellite Energy Inc. (OTCPK:RUBLF) at its original issue price of CAD$2.00 a share through a private placement. The company was a spin-off of Perpetual Energy, and I held some shares of that company which qualified me to participate in the Rubellite financing. I have long been an admirer of the late Clay Riddell, current CEO Sue Riddell Rose’s father, who was a legendary oil man in Canada’s Western Canadian Sedimentary Basin. Based on the limited disclosure at the time Rubellite was formed, I created a model of its outlook using both the company’s disclosed data and estimates based on Headwater Exploration’s operations in the Clearwater play. Here is that model:

Michael Blair analysis

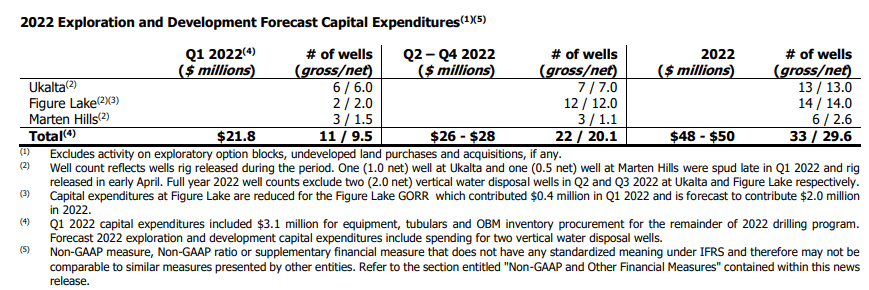

Rubellite reported Q1 2022 results which were in line with my model, with production reaching over 2,000 barrels a day by the end of Q1. The company completed a financing in early 2022 and amended its capital program, now planning to spend between $48 and $52 million, about double the amount I had modeled.

Rubellite disclosure documents

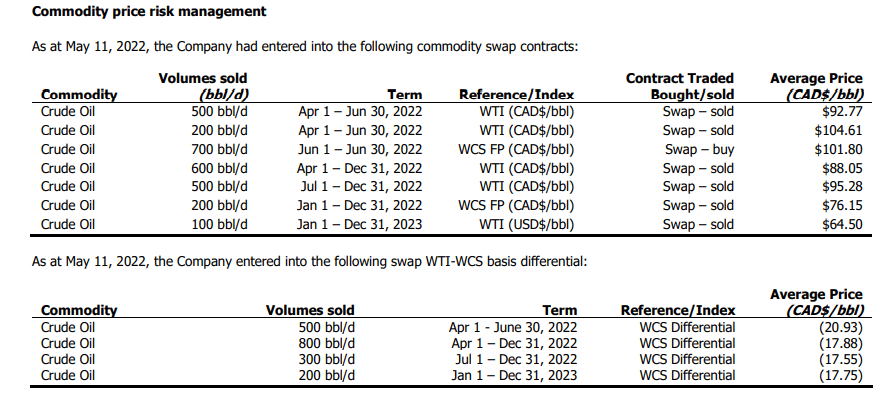

That accelerated plan puts the company ahead of my modeled results and with oil prices for Western Canadian Select heavy oil running at about CAD$100 a barrel, the operating economics should be robust. For a junior company with little operating history, investors should exercise caution with all of the number both from the company and my own estimates. Netbacks from the Clearwater play in Q1 2022 were $71.02 a barrel before “hedging” costs that reduced Rubellite’s realized netback by $29.02 a barrel to the reported $42.00 average for the quarter. The company continues to have a portion of its output “hedged” but at substantially higher prices than in Q1.

Rubellite disclosure documents

As a result, prices likely to be realized for the remainder of the year are higher than I had projected.

There is plenty of risk in a junior oil developer, and Rubellite is no exception. Oil prices are volatile, and the world’s economists are talking about a possible recession which could result in materially lower oil prices. But with a competent management team and the hedges in place, I don’t see a risk of failure for Rubellite and see the longer term prospects as positive.

I like the gamble and hold 40,000 shares.

Be the first to comment