Chee Siong Teh/iStock via Getty Images

Written by Sam Kovacs

Introduction

A year ago, we were asked whether we were bullish or bearish on US stocks in 2022.

I’ll quote the answer I wrote below. Our point was: we’re bullish on the right stocks.

Many will scratch their heads at this assertion, and claim that incoming rate hikes are bad for equities, and that a Shiller P/E of 39.4 indicates that the bull market must be coming to an end.

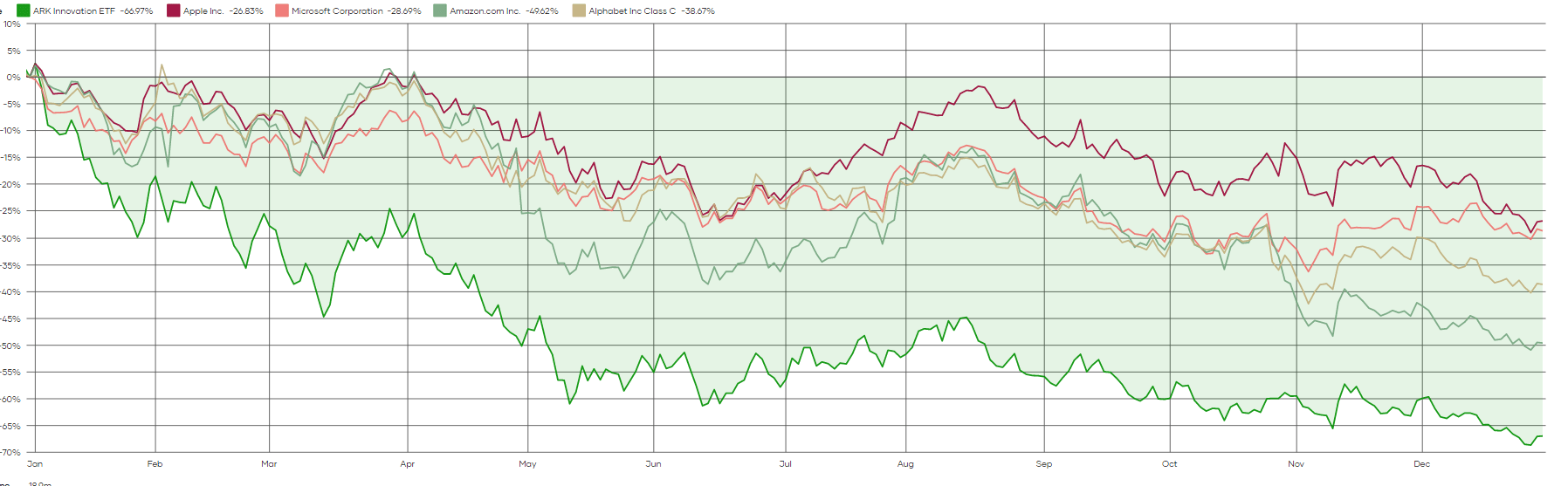

But I believe it is short sighted to look only at a market weighted index, which is increasingly concentrated. Today, 5 stocks –Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOG) (GOOGL), and Tesla (TSLA) — account for 20% of the index. Add the next 5, and you get 30% of the index.

It is not representative of the market. Financial services (XLF), and energy (XLE) are still mostly undervalued relative to the past decade, despite a great run.

So you have cheap stocks which are on the way up and still cheap. And expensive stocks which are on the way down and still expensive. In March we said we were bearish ARK Innovation (ARKK). The fund is down 20% since. Another 20% decline wouldn’t surprise me.

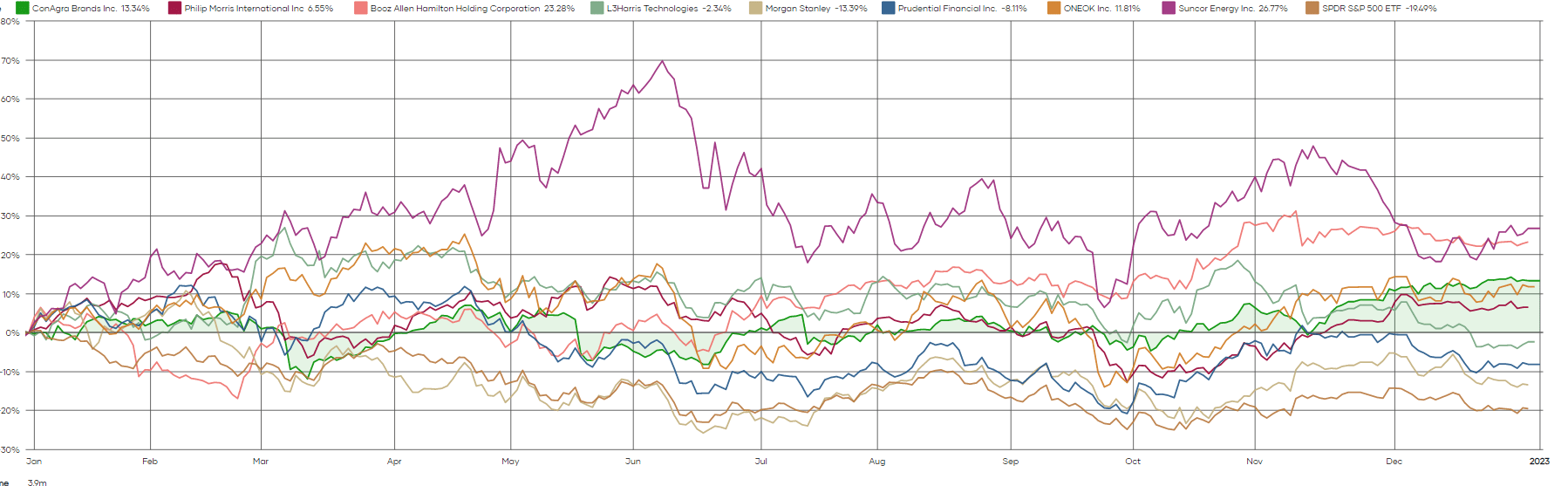

At the equity level, dividend investors can find undervalued names in every sector. Here are a few examples:

Looking back, it seems we were quite spot on.

The stocks I listed as being good value ALL beat the S&P 500 over the past year.

Dividend Freedom Tribe

The 5 tech stocks all did way worse than the S&P 500.

Dividend Freedom Tribe

The only mistake I made was not being bearish enough on ARKK. We said it was going down at least another 20%. It went down 66%.

Being exposed to the right sectors, and then picking the right stocks within those sectors led us to do much better than the index in 2022, after having already done so in 2021.

We’re on a mission to prove that dividend investing can do better than the index in all environments, if done right.

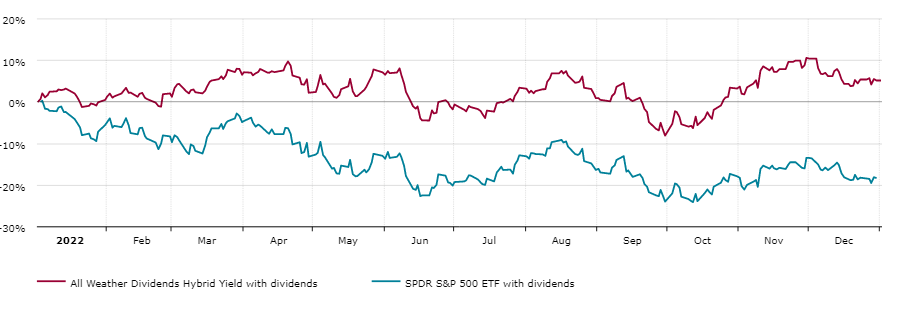

At the Dividend Freedom Tribe, we offer 3 model portfolios to offer insights on how we approach dividend investing.

We offer a low yield, a high yield, and a hybrid portfolio, which mixes both approaches.

The hybrid was the worst performing portfolio in 2022, up 5% including dividends. This was still 23% better than the index.

DFT Portfolio Performance (Dividend Freedom Tribe)

Being bullish on the right stocks

There is a certain arrogance to saying, “being bullish on the right stocks”.

Easy to do after the fact, once you’ve had a good year.

But this is not what I want to get to.

In the short term, say over a year or two, there are certain sectors or industries which will be in favor, and this will drive returns.

Among those sectors and industries, there are certain stocks which are undervalued. These stand to doubly well.

Obviously, energy stocks did well in 2022, as the only up sector. This has led to investors overcrowding the long energy position in Q4 2022. Both OKE and SU outperformed just because of this.

But Suncor provided 3x the returns OKE did, because it was particularly undervalued, because of the market discounting Canadian stocks beyond reason, because of a strong US dollar. This bias hasn’t yet been fully corrected.

Booz Allen Hamilton was in a similar position. Particularly undervalued and set to profit from increased cybersecurity threats to the federal agencies it works with. With a very likely 8% increase in the defense budget in 2023, it still has wind in its back, although it now trades at fair value.

Buffett and Munger are known for preferring great companies at good prices to good companies at great prices.

Our approach is quite straightforward: buy great companies at great prices.

It’s a market of stocks, not a stock market, and there is always something undervalued.

Sometimes you need patience. We accumulated energy stocks throughout the second half of 2020, and the first half of 2021, to then see exponential success in these positions in 2022.

In early 2021, we started building positions in defense companies, only to see them reap profits in 2022.

Some patience is required for the market to come to terms with its over exaggeration, course correct, and eventually becoming bullish again on the industry or sector.

Below is the performance of each sector in 2022, as well as the forward PE now and the previous year.

| Sector | 2022 % | Fwd PE | Fwd PE last year |

| Energy | 59.0% | 9.7 | 11.1 |

| Utilities | -1.4% | 18.9 | 20.4 |

| Consumer Staples | -3.2% | 21.0 | 21.8 |

| Health Care | -3.6% | 17.6 | 17.2 |

| Industrials | -7.1% | 18.3 | 20.8 |

| Financials | -12.4% | 11.9 | 14.6 |

| Materials | -14.1% | 15.8 | 16.6 |

| Real Estate | -28.4% | 16.5 | 24.2 |

| Information Technology | -28.9% | 20.1 | 28.1 |

| Consumer Discretionary | -37.6% | 21.3 | 33.2 |

| Communication Services | -40.4% | 14.3 | 20.8 |

| S&P 500 | -19.4% | 16.8 | 21.4 |

Among all the sectors, Energy and Financials remain the cheapest, and there are still some great opportunities in those sectors.

But tech, consumer discretionary, communications services, and real estate have seen their valuations decline the most in 2022.

These are the sectors where investors have likely thrown in the towel and thrown the baby out with the bathwater. (I don’t always get the opportunity to use two idioms in one sentence).

Within tech, semiconductors remains the industry of most interest to dividend investors, as I pointed out in a recent article within which I recommended Broadcom (AVGO) and Intel (INTC).

In this article, I’ll suggest a REIT stock which will provide good yield, downside protection, and opportunity for upside. I’ll offer one stock to sell that has none of these attributes.

Buy Digital Realty

Real estate stocks got beat up bad in 2022. Some stocks did alright. In January we suggested investors buy VICI Properties (VICI). The stock managed to squeeze out single digit growth this year.

Not all stocks did so well.

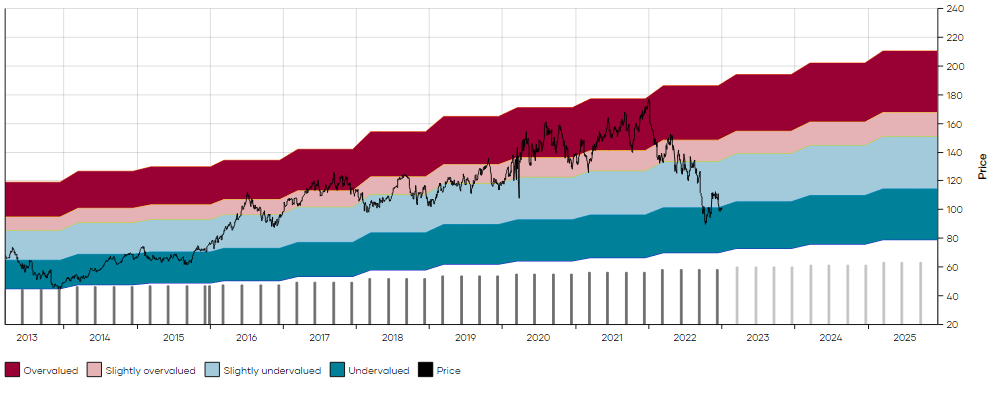

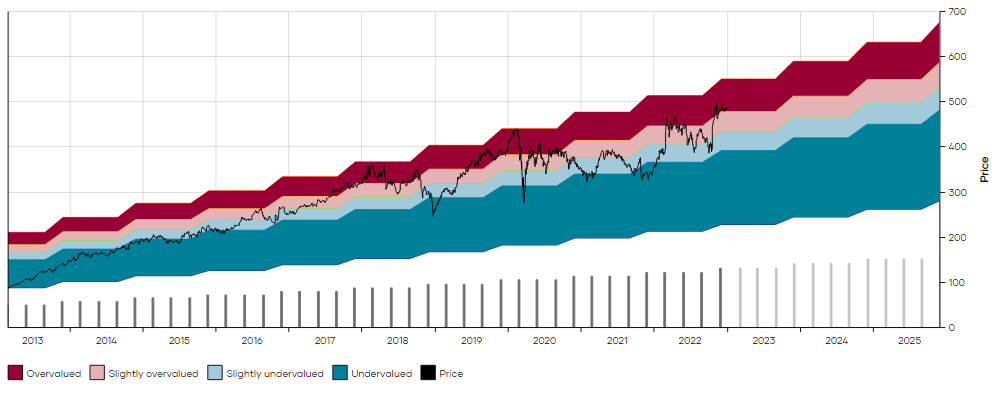

One which had an awful year, is Digital Realty (DLR), which was a darling during 2020 and 2021.

As you can see in the MAD Chart below, it stumbled hard in 2022. (Click here for more on MAD Charts)

DLR MAD Chart (Dividend Freedom Tribe)

DLR now trades at $100 and yields 4.87% which is significantly more than its 10 year median yield of 3.67%. The next dividend will be higher, so the forward yield is likely closer to 5.1%.

Given DLR’s dividend potential of 5% annual growth which is well supported by its fundamental growth, long term tailwinds in the data center space (although not as crazy as people had imagined in 2020 and 2021), the stock’s fair price is around a yield of 4%.

In the past decade, it has tended to be lower than that as investors projected higher growth than DLR could realistically deliver.

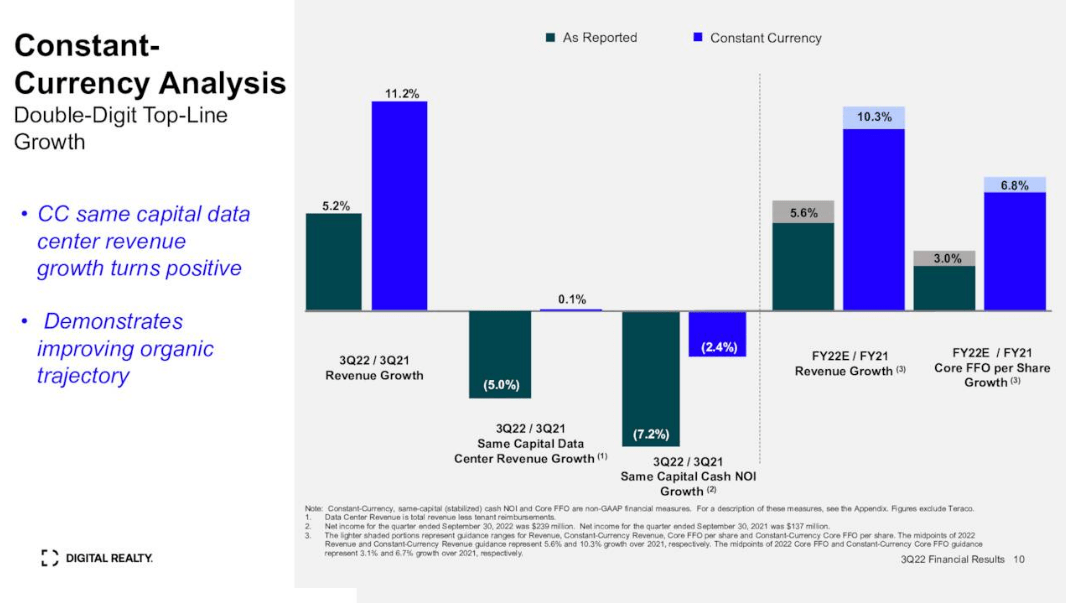

DLR’s bubble popped, and the market overreacted. It overreacted because DLR is still growing & it has a well laddered debt schedule which shelters it of interest rate sensitivity over the next year.

On a constant currency basis, top line revenue is forecasted up 10% and FFO up 6.8%.

DLR Investor Presentation

If we believe that currencies will gravitate towards PPP over the long term, with significant deviations in the short run, then we can view the strengthening of the dollar as a headwind to results which will revert in the future and produce the opposite effect, like an elastic band which is extended, and must contract at some point.

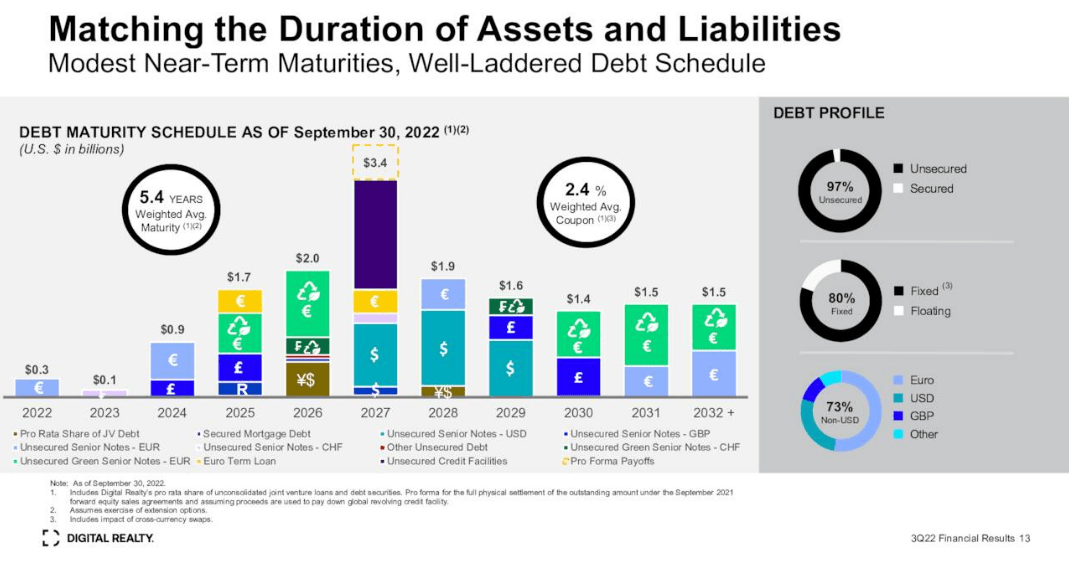

Furthermore it should be noted that for the most part, revenues and expenses, as well as assets and liabilities, are matched in their own currencies.

DLR Investor Presentation

This means that the only significant cashflows in USD which are a drag on profits would be any HQ expenses and the dividend.

Given that DLR currently pays out about 72% of its FFO, below the 75% to 85% range which is considered healthy for REITS, I wouldn’t be surprised to see them maintain their 5% dividend increase rate in March ’23 when they next increase the dividend.

DLR is a high quality company because of the quality of its operations, the tailwinds in the industry which should ensure stable 5% growth for years to come, and reasonable interest rate protection.

Sell Lockheed Martin

During the past decade, LMT has been quite erratic, going from undervalued to overvalued and back.

The stock now yields 2.47%, which is less than the 10 year median yield of 2.8%.

On the MAD Chart below, the red range marks yields between 2.2% and 2.5%.

LMT MAD Chart (Dividend Freedom Tribe)

As you can see above, during the past decade, anytime the stock has yielded within this range, it would have been a great time to sell.

The possibility for a mean reversal outweighs the possibility of squeezing out another 10% gains.

Exiting the position gradually is reasonable, and you can then reinvest the proceeds in something with better potential.

You can also see that the blue undervalued area in the MAD Chart is when LMT yielded more than 3.1%.

Whenever LMT yields above 3.1% it is a good buy. Whenever it yields less than 2.5% it is a good sell.

This isn’t function of what revenue or earnings or whatever will do for the next quarter. These are the short term events which produce a good price to buy, or a good price to sell.

The bullishness in the defense industry has bid stocks like LMT up. We bought when they were last beaten down a couple years ago and are now moving out.

Conclusions

By buying low, and selling high, you do well. Of course you don’t know when stocks will be low or high, so you have to adapt, and wait for the right opportunity.

Focusing on only high quality businesses and moving out before stocks get so overvalued that they crater by 50% is just common sense.

Having a long term view means you can actively move in and out of stocks, while growing your income and maximizing your retirement potential.

Be the first to comment