Spencer Platt

Introduction

We liked some of the items Robinhood (NASDAQ:HOOD) reported out of Q4 ‘22 earnings but expect negatives to outweigh positives near-term. We want to emphasize that the company is making a fine gesture to shareholders by announcing a buyback of the FTX-Founder shares related to SBF (Sam Bankman-Fried) which amounts to 7.6% of the shares outstanding, the stock initially bounced by +5% following the announcement of earnings on Wednesday, February 8th, 2023 reaching $11.04 the following trading session on Thursday. HOOD fell below $10 to then close the week at $9.98 by Friday, February 10th, 2023. The negatives outweigh the good, even if management plans on retiring $500 million in share based compensation for co-founder Vlad Tenev, and Baiju Bhat. The company’s fundamentals remain weak, and it’s why we reassert our strong sell recommendation on Robinhood.

HOOD’s on-going cryptocurrency winter keeps the stock suppressed near-term. We’re bullish on Bitcoin (BTC-USD) long-term and anticipate the price of Bitcoin to eventually recover over the next 12-months as presented by our report on Bitcoin where we forecast the price of BTC to reach $33,000 to $45,000 over the course of 2024. We expect HOOD’s business to be responsive to a Bitcoin rally, but remain overpriced when making a valuation estimate using conventional multiples.

Given HOOD’s overwhelming mix towards retail clients currently, and low net interest margins on brokerage accounts, we expect poor operating performance drives the stock price lower. A strong balance sheet with $6+ billion in cash certainly keeps a floor underneath the price, but the need to spend money on growth, while also needing to retire FTX related shares keeps bears in control of the stock as near-term operating metrics aren’t going to improve by much. Furthermore, modest improvements to adjusted EBITDA metrics over the course of 2023 might move the needle, but absent a sensational rally in cryptocurrency prices, we think the brokerage is doomed on near-term weakness tied to crypto-weighted brokerage accounts.

Limited profit contribution from higher interest rates, which is expected to contribute $20 million in net interest revenue to the broker, given the +25 bps Federal Reserve hike. HOOD management mentions the reason for the limited revenue contribution even with interest rates set at 4.5%-4.75% by the Federal Reserve is due to their narrow net interest margin. This is because their net spread on Robinhood Gold is limited to 50 basis points, as they pay their customers approximately 4.15% out of 4.65% leaving them with 0.5% on $18 billion in interest earning assets. When doing the math, HOOD generates about $90 million on 0.5% profit margins on $18 billion in client assets, and unless the interest rate margin widens, the broker is unlikely to generate much of a surprise from interest related income tied to savings accounts.

We revise our estimates in response to the quarter

Robinhood Q4 GAAP EPS $0.19 missed consensus expectation by $-.07 whereas revenue of $380 million missed consensus expectation by -$15.16 million despite sales growing +4.7% y/y.

We raise our price target on Robinhood from our prior report on Robinhood, mainly due to adjustments on the amount of share count for both FY ‘23, and FY’24. We cut back our estimated shares from 982 million to 892 million for FY ‘23 tied to the $500 million in founder share authorization retirements. We also reduced our share count estimate for FY ‘24 from 1,082 million shares to 837 million shares tied to the eventual removal of SBF and FTX related contagion amounting to a total -245 million shares in total outstanding being subtracted to the stock over the next couple years based on our forecast, which moves our $3.44 price target up to $4.89. Even with the price target increase on HOOD, it doesn’t take away the justification of our sell rating on the stock.

In terms of our bottom line estimates, we still anticipate really slim profitability on an eventual recovery in crypto-related recovery in the market, as we forecast $2.691 billion, and $0.26 dil. EPS for FY ‘24, which compares to consensus estimates of $2.05 billion and $-0.19 GAAP dil. EPS.

Consensus analyst estimate don’t anticipate or factor in Bitcoin performing much better following block halving in 2024. We tend to differ, thus our more aggressive estimate on revenue, as we expect HOOD revenue to accelerate by +60% in 2024. This hinges primarily on cryptocurrency market fundamentals improving, and trading revenue on the cryptocurrency side of the business also correspondingly improving over the next 24-months. HOOD currently trades at around $10, but even with a bunch of aggressive growth inputs embedded into our financial model, which is well above consensus estimates, we yield a -50% price target assumption anyways.

We find ourselves valuing the stock at a -50% discount from where the stock is currently trading, and cannot seem to argue a solid enough margin narrative even at optimal profit margins to justify the businesses valuation until we get past a number of years of 50%+ sales growth, which is highly unlikely, as cryptocurrency bullish cycles tend to last for a limited amount of time, or roughly 18-months maybe 2-years at most. For now, HOOD will feel like an early-stage shareholder financed stock, which is broadly frowned upon in the current market environment by public investors given the heightened fears of a recession, and dilution risk keeping shareholders paranoid.

Why we remain bears on Robinhood

We don’t find ourselves compelled to change our rating on the stock even with a number of shareholder friendly moves until they address all three of their other strategic priorities, 1) increase retirement account assets 2) increase the number of services to more advanced traders. 3) Provide and attract more international brokerage customers with the necessary foreign securities and provide those foreign securities to domestic U.S. HOOD brokerage accounts.

Assuming they can provide more services to foreign accounts, and also provide domestic traders access to foreign securities, the perception of being a dumbed-down retail product could be mitigated, as they position towards a more advanced and deeper-pocketed pool of high net worth accounts. We hope Robinhood rapidly executes, and transitions towards becoming a top-tier brokerage product known for broadness of asset selection, and availability of options for saving and investing money with some help in the form of analytics and tools for tracking and managing money.

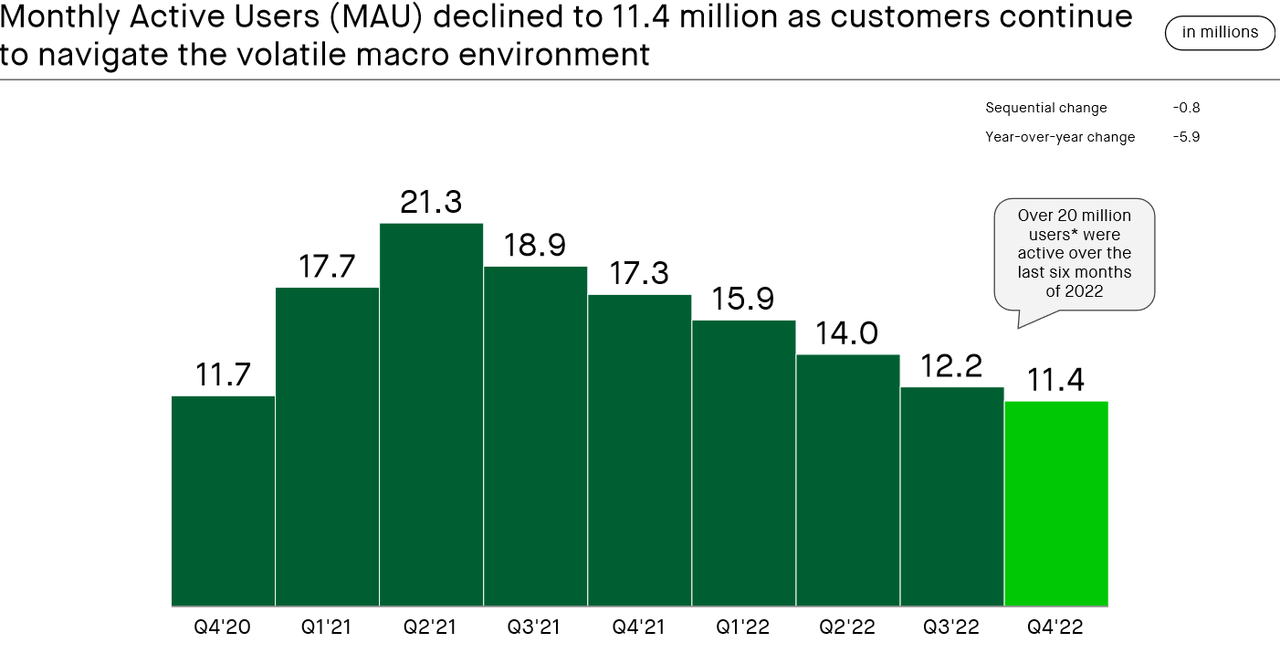

Figure 1. Robinhood MAU Figures Trending Lower Still

Robinhood Q4 ‘22 Earnings Presentation (Robinhood)

Number of MAUs declined sequentially from 12.2 million to 11.4 million, we think management downplayed the weakness tied to macro and layoffs. However, we think the weakness tied to registered and active accounts has to do with the negative experiences people broadly report on video logs, and various other forms of media tied to the company. Negatives tied to the cryptocurrency FTX contagion also reflects on the attrition in brokerage accounts in Q4’22. Reasserting the weakness in user trends for 7 consecutive quarters from 21.3 million MAUs down to the present 11.4 million MAUs.

Even with the late addition of retirement related accounts, and long-term savings accounts in Q4 ‘22, we anticipate that sentiment around the stock won’t improve by much. Modest improvement on ARPU from $64 Q4’21 to $66 in Q4 ‘22 (representing a $2 improvement on account level monetization) also really weak, and counter to our thesis that eventually the price of BTC-USD will recover thus causing the fundamentals of Robinhood to improve at some point.

We think Robinhood does have a compelling use case for some retail investors who prefer a simpler brokerage, but we don’t anticipate the stock price to improve meaningfully given the worsening profitability following the negative profit miss. The overwhelming dependence on BTC-USD to turn the corner financially, means investors might be better off investing in Bitcoin. A classic example of where it makes more sense to buy the commodity and not the miner, or in this case the exchange/brokerage service provider.

Assuming the Bitcoin market does turn the corner, so should Robinhood, but even in the most optimal of scenarios, we expect the stock’s financial results to perform really poorly over the next couple quarters, as growing internationally, and providing more advanced services for advanced traders is very costly and will require a number of strategic investments in areas of the business that will make a 10% adjusted net profit margin difficult to achieve, as we forecast in our financial model in FY ‘24. Assuming we are wrong, and volume doesn’t translate to the heightened margins we expect, we might have to cut back on our own expectations on net profits 12 months from now.

We maintain the bias that Bitcoin outperforms dragging HOOD revenue’s, trading commissions, and its margins higher over the course of 2024. But, we also expect a sequence of earnings misses tied to profitability and investments in 2023 to push the stock price lower. We anticipate Robinhood will invest and use cash ahead of anticipated Block halving.

We have an optimistic bias on the quality of the trading service going forward, because we think HOOD is intentional about improving the value of its brokerage offering over time – we advocate for smaller retail investors getting access to better brokerage services. Even if HOOD is the means to achieving such an outcome, we think retail investors will be appreciative of foreign securities, and foreign investors getting access to a simple brokerage and cryptocurrency interface for the very first time. HOOD’s mobile app may soon offset the -10 million in MAUs lost from the prior cryptocurrency peak with international MAUs over the next two to three years.

Financial model overview

What we find missing in the stock’s narrative is the valuation. Even in the most optimal of scenarios the stock would be trading at a very inflated multiple, and it’s not clear when management will exit the phase of shareholder financed growth. The overwhelming dependence on the existing cash pile to fend off bears as opposed to compelling growth metrics in conjunction with improving margins also keeps us bearish on the stock.

Currently the stock has a 7% short interest. But, given the negatives tied to Bitcoin prices lately, we wouldn’t be surprised if bears went short as the broker continues to under-perform on earnings results.

Bitcoin could continue to appreciate on limited supply growth due to block halving by the end of 2024. At least, that’s what our crystal ball seems to be suggesting, but because technology moves so fast, we’d be hopeful that there will be time to accumulate a position in an eventual reversal in both HOOD and Bitcoin, though we’re not certain when it makes sense unless if HOOD were trading closer to a fair value like $5 as our model implies.

HOOD doesn’t trade at a compelling valuation, and because the business is burning cash – we find it hard to stomach the business, and don’t own the stock currently. Stock is expensive even with optimal margins and sales at an inflated exit valuation. It’s why we argue that it’s still not worthwhile to own HOOD when owning Bitcoin carries similar downside risk near-term, but carries more upside (+50% upside) assuming BTC reaches the $33,000 price target, versus -50% downside in Robinhood at a $5.00 price target.

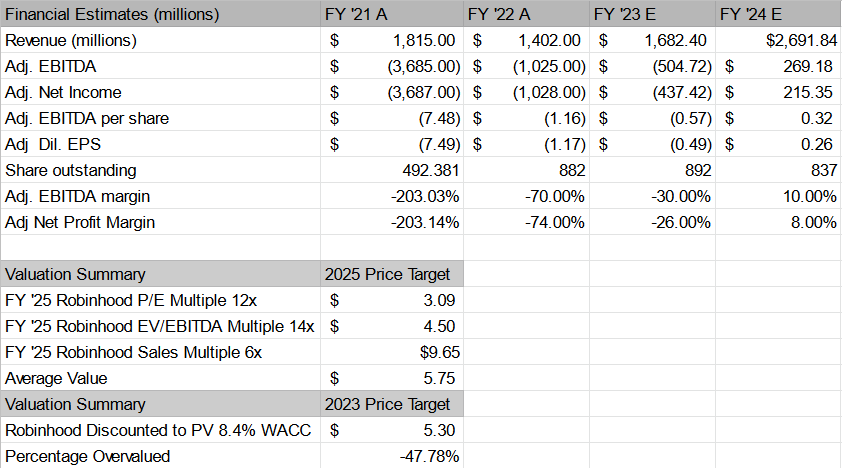

Figure 2. Financial Model 2023-2024 Robinhood

Robinhood Financial Forecast 2023-2024 (Trade Theory)

Not much has changed, aside from adjusting our full-year FY’22 estimates to actual results, and reducing the share count in our financial model considerably, as discussed earlier in the report. We adjusted our price target up from $3.44 to $5.30, or when rounded from $3.50 to $5.00 basically. We value the business the same exact way at FY ’24 12x P/E, 14x EV/EBITDA, and 6x Forward Sales to arrive at our revised price target of $5.30 upon discounting the firm by 8.4% (WACC by a single year).

We also adjust the share count in our estimates lower to account for the retirement of $500 million worth in shares and the eventual buyback of an additional $500 million worth in shares translating to approximately 100 million share count reduction even if employee stock options and grants continue to trend higher, which is something we also factor into our total share outstanding figure, but not as much growth in total share count.

In terms of profit margins, we still value the business like a low margin high volume broker, where we anticipate the company will report optimally 10% net profit margins on heightened trading volumes, and heightened brokerage account activity with block halving contributing to a re-surging Bitcoin price in 2024. Even with BTC positives and HOOD sales growing by 60%+ factoring a normalized growth trend from the prior BTC peak, we find the stock heavily overvalued, and would avoid the stock at all cost in the present environment. This is given the overwhelming likelihood of missing on bottom line metrics as we progress through FY ‘23, and loss of MAUs implying weak metrics on a qualitative basis as well.

As such, we estimate that Robinhood will report -$504 million adjusted EBITDA in FY ‘23 versus our prior estimate of adjusted EBITDA loss of -$497 million representing an -$8 million increase in adjusted EBITDA loss. We adjusted our revenue up from $1.657 billion FY’ 23 estimate to $1.682 billion FY’23.

Robinhood final conclusions on the quarter

Even with some minor adjustments to our model we find ourselves negative on the stock as nothing has structurally changed about the thesis aside from corporate level buyback activity, and some adjustments to the brokerage product to include a cash savings account, and the announcement of retirement related investment and savings accounts. We like the effort HOOD put into retirement savings accounts, which may have a positive impact on account retention and MAU figures. But, likely too little too late for HOOD, given the onset of the on-going cryptocurrency winter.

We hope the narrative improves, but absent a meaningful turnaround effort on profits and user metrics, we expect other large cap technology stocks such as Alphabet (GOOG) (GOOGL) and Meta Platforms (META) to offer more upside with less risk in this environment.

Furthermore, we’re fundamentally permanent bulls on Bitcoin, and anticipate that as opposed to buying HOOD, it’s more opportunistic to buy BTC-USD right now. This is given the poor fundamentals of a low-margin, cash burning brokerage, that continues to miss on earnings results. The bar has been reset multiple times, over the course of the entire year, and likely trends lower through 2023 driving the stock price lower.

We expect that unless the price of BTC-USD recovers, HOOD is likely trending below $10, and could reach $5 over the next 12-months implying -50% downside even with the included impact of all the announced share buybacks over the next 24-month period. We also anticipate that even with the price of BTC recovering and sales, brokerage commission volumes recovering at HOOD, the stock is still heavily overvalued even if profit margins improve to a +10% level.

No analyst is willing to be that optimistic, and every analyst anticipates the stock deserves to be priced higher at the same time. The truth is probably somewhere in the middle, which is why we’re more optimistic on fundamentals, and bearish on price over the next 12-months when compared to consensus estimates. We wouldn’t recommend HOOD to our readers at the present time and continue to reiterate our strong sell recommendation on HOOD stock.

Be the first to comment