BeyondImages

After our Q1 production comment, today, Rio Tinto (NYSE:RIO, OTCPK:RTPPF, OTCPK:RTNTF) released the second quarter operational performance. After our initiation of coverage with a neutral rating, we recently decided to upgrade the mining company on the back of its simple structure and juicy dividend per share. The next catalyst is the full presentation and Q&A session (here is the link) that the company plans to report on the 22nd of July, but today we provide our first impression thanks to the Q2 production release.

Q2 Production Results

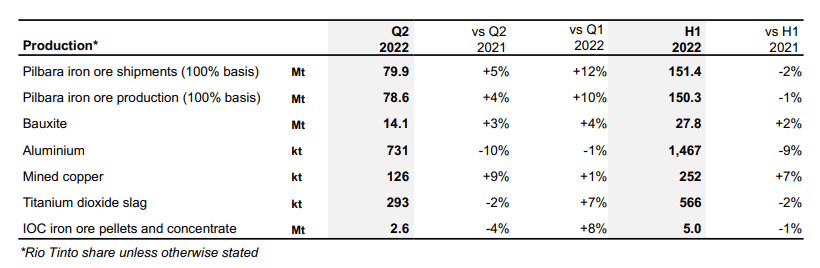

Rio Tinto’s production in Q2 was mixed with a slight decrease in commodities output. Looking at the Wall Street consensus estimate, the company’s output was in line with iron ore production, whereas Rio Tinto missed expectations on copper and aluminium.

Rio Tinto production results

Looking at the specific results, here below our key takeaway:

-

Iron ore production and shipments were ahead of the consensus, and Rio Tinto confirmed the iron ore 2022 outlook. This means that the company will deliver superior performance in the second half of the year. Indeed, the company is planning the next phase of Gudai-Darri and Robe Valley. This will be translated into higher volumes. Despite higher costs due to inflationary pressure, thanks to the weaker currency effect on AUD, the unit cost guidance was left unchanged.

-

Aluminium production missed consensus by 730kt. This was due to the late rump-up of Kitimat that was afflicted by a union strike. Also, Boyne production decreased due to COVID-19 outbreaks. Looking at the costs, we are forecasting significant headwinds. Thanks to the production report, our internal team is forecasting higher costs on the back of higher energy costs.

Rio Tinto higher costs

- As already explained, Copper production missed analyst consensus. The main cause was the labor shortages at the Kennecott facility. More importantly, due to the lower selling prices in the first half year, the company will most likely deliver a minus $140m provisional pricing effect.

-

Diamond production was lower due to Diavik site planned maintenance.

Conclusion and Valuation

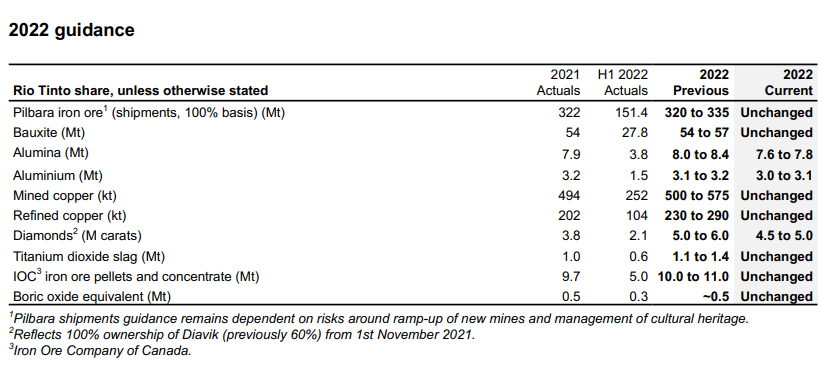

On the back of these results, Rio Tinto has decreased its forward guidance for diamond, alumina, and aluminium by 13%, 6%, and 3%, respectively.

Rio Tinto 2022 Guidance

We should note that Rio Tinto’s commodity mix at the EBITDA level is mostly based on iron ore results. Adjusting the new company guidance, we slightly lowered our target price to £58 per share due to higher costs resulting in a 5% EPS downgrade over our 10 years forecast period. Once again, we see no justification for a discount compared to BHP (BHP), Rio Tinto has a rock-solid balance sheet with a net cash position and also is currently yielding 13%. Indeed, Rio Tinto remains our top pick in the mining sector.

Mare Evidence Lab analysis

Be the first to comment