JHVEPhoto/iStock Editorial via Getty Images

Here at the Lab, we have a good grip on mining companies. In 2022, we initiated Rio Tinto (NYSE:RIO, OTCPK:RTPPF, OTCPK:RTNTF) with a neutral rating, and then we decided to move our target to overweight. Since our Q2 release update, Rio Tinto’s total return including its generous dividend payment was 34.54% compared to the S&P 500 which delivered a minus 2.07%. Our buy case recap was based on:

- A compelling valuation versus BHP.

- A tasty dividend yield that provides a good margin of safety.

- M&A optionality.

- A solid balance sheet coupled with positive quarterly results (we commented on Q1, Q2, and Q3 production reports).

Mare Evidence Lab’s previous publication

Starting with the positive news, Rio Tinto completed the Turquoise Hill Resources acquisition. This is a supportive and positive catalyst in our view, given the fact that Rio Tinto’s commodity exposure was skewed versus the iron ore production. In the special meeting, almost 90% of TRQ stockholders and 60.5% of TRQ minority stockholders positively voted in favor of Rio Tinto’s Scheme of Arrangement. As already mentioned, the company’s equity stake was already at 50.79%, and with this move, the new shareholder’s structure of the Oyu Tolgoi mining will be 66% in Rio Tinto’s hands and 34% equity to the Mongolia Government. Financially speaking, Rio Tinto paid approximately $3.1 billion, and TRQ shareholders will receive 80% of the AuD $43 per share in cash. To add some color, the mining company will boost copper production by 43%.

Mare Evidence Lab’s previous publication

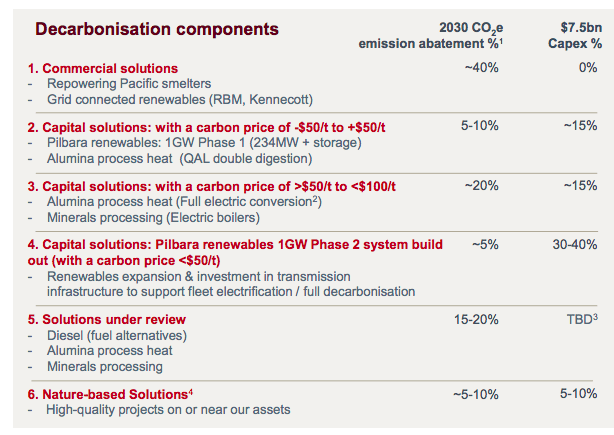

In the meantime, Rio Tinto hosted an investor seminar. There are a few interesting facts to report. First of all, Fiscal Year 2023 production guidance were below Wall Street’s average consensus. However, we do believe that this is a management strategy to be conservative and most likely will result in what we call underpromising to reach an overperformance (and consequently beat equity research analysts’ expectations). Here at the Lab, we positively view the cultural improvements that Rio Tinto is currently doing. The new agreements with local owners are leading to concrete changes in the way that projects are completed, and this is supportive post-Juukan Gorge ESG story recovery. Management also provided a better view of CAPEX expenditure with two new decarbonization projects. In addition, approximately 50% of the $7.5 billion total investments are expected to be used as follows:

Rio Tinto CAPEX plan (Rio Tinto Investor Seminar)

In our risks section, we always emphasize Rio Tinto’s EBITDA risk (3/4 of the total group EBITDA comes from iron ore) and its Chinese dependency. In the first nine months of 2022, both stainless steel and carbon steel production fell at the same negative rate. In detail, the former was down by 4.9% on a yearly basis and the latter reported a minus 5.3% in the same period. We should recall that stainless steel grew by 10.6% in 2021 and is on track to exceed 55 million tons by 2022 end. Looking at the Chinese region, stainless steel output decreased by 5.2% and showed how Beijing is less resilient than the rest of the world and how COVID-19 is still impacting its economy. However, it is important to mention that Indonesia is experiencing an important step-up. Indonesia’s stainless steel output is rising and production increased by 8% year-on-year. As a reminder, the region is now the second-largest producer of stainless steel. In 2021, it accounted for 8.5% of the world market share, and looking at the numbers, in Q2 and Q3 of 2022, this value approached 10%. This should be very supportive of Rio Tinto’s future accounts and decrease Chinese dependence.

Conclusion and Valuation

Here at the Lab, we positively view the company’s latest achievements (TRQ acquisition and lower iron ore dependency, better relationships with traditional communities, Indonesia growth, and Rio Tinto CAPEX details). For this reason, we decided to maintain our overweight rating (the company is still trading at a 30% discount compared to BHP; however, our internal team sees the Fiscal Year 2023 iron ore outlook as achievable. The next catalyst that we will comment on will be the company’s Q4 production report expected to be released in mid-January. Mare Evidence Lab’s main risk remains the commodity price evolution.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment