Kiran Ridley/Getty Images News

Rheinmetall (OTCPK:RNMBF), Germany’s premier defense contractor, posted a preliminary update for FY22, with sales falling short of prior guidance but margins coming in stronger than expected. The headline numbers weren’t majorly surprising, though, given the technical issues reported with its Puma vehicles, and shouldn’t impact consensus expectations or the long-term outlook.

This is still a play on the secular rise in German defense spending (currently ~2% of GDP) and higher order flow to Rheinmetall over the coming years. The recent Expal acquisition is a step forward in building out its offerings – not only is the acquired portfolio complementary from a commercial standpoint, but it also allows Rheinmetall to diversify overseas (mainly Spain), helping to mitigate concerns around the sustainability of the German defense upturn. Valuation-wise, the stock isn’t expensive relative to its growth potential at ~13x FY24 P/E and could benefit from an index addition catalyst in the coming quarters as the DAX rebalances post-delisting of Linde (LIN).

Pre-Announced Revenue Falls Short, EBITA Better Than Expected

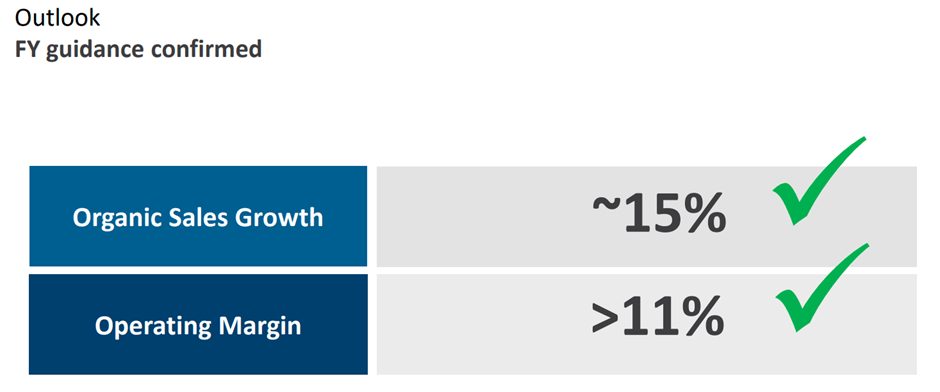

Earlier this month, Rheinmetall published an ad-hoc press release outlining its preliminary results for FY22 and its adjusted full-year guidance. At first glance, revenue numbers were disappointing at EUR6.4bn, with the implied organic growth of ~10% falling well short of guidance at ~15%. Much of the delta was due to timing issues related to defense-related contract bookings being delayed to early FY23 (vs. Q4 2022 prior). Fundamentally, a weaker-than-anticipated global auto recovery also contributed, though given the automotive segment’s limited P&L contribution, any impact is unlikely to be material. That said, profitability came in above expectations on a favorable mix shift, with the operating profit growth of >20% driving an “at least 11.5%” group operating margin profile (vs.>11% previously) or an implied EBITA of >EUR736m.

Rheinmetall

Somewhat disappointingly, the release offered little insight into the FY22 order book. Relative to the prior guidance for a ~EUR6bn order intake for the year, the actual result is likely to fall short, in my view. The recently reported technical issues of the Puma infantry fighting vehicles will be a key drag, as management had previously expressed hope for upgrade-related and new vehicle orders. While these issues have been reportedly fixed, I would wait and see before penciling in the incremental order flow (likely in FY23 vs. FY22, as previously anticipated). On the other hand, some of the Puma headwinds could well be offset by increased ammunition orders from the German government in December as it looks to address shortage concerns.

Driving Growth via Expal Systems Acquisition

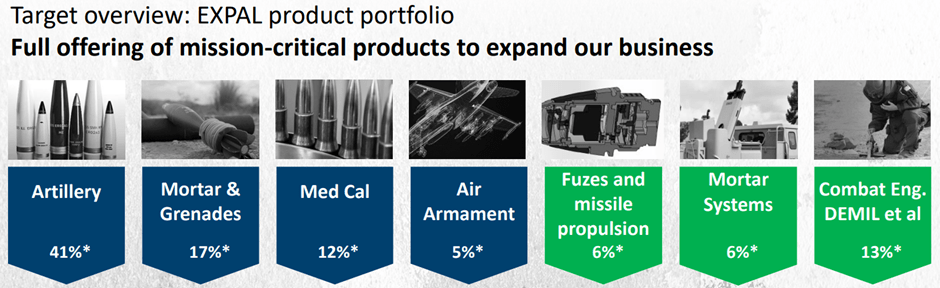

The announcement comes on the heels of Rheinmetall acquiring Spanish ammunition manufacturer Expal Systems. The acquisition helps fill a crucial gap on the artillery ammunition side, currently derived from South Africa, given Expal’s products are compatible with NATO hardware. Rheinmetall also currently lacks surplus artillery ammunition capacity, so the addition of Expal’s revenue base (>40% from large ammunition for artillery) is timely in the context of the increased demand in Germany. The synergies are mainly targeted to come from procurement, though I would note the upside from the complementary product portfolios, particularly in artillery and mortar ammunition. Finally, Expal grants geographic expansion optionality – with 10-20% of the sales contribution from Spain, leveraging the Expal know-how to diversify beyond Germany presents a compelling new growth driver.

Rheinmetall

While management is projecting Expal sales to almost double from the current ~EUR400m in FY22/23, this target may not be out of reach given its capacity supports annual sales potential of EUR700-800m. Plus, the ongoing shortage of ammunition inventory across NATO regions isn’t going away anytime soon, and the restocking cycle following the shipment of inventories to Ukraine should continue for a while. Depending on how long the Russia-Ukraine conflict stretches, this could last years, though Rheinmetall pegs the restocking process closer to a decade; either way, this deal allows the company to tap into a secular growth driver across NATO regions. Operating leverage is key – management projects margin expansion beyond Rheinmetall’s ~19% EBITA margins in the Weapons & Ammunition segment. Assuming management’s projections hold true and based on a low to mid-single-digit % cost of debt, EPS accretion is set to run up to an impressive 15% by FY24. The implied ~3x EV/Revenue price tag keeps me on the conservative side of potential accretion outcomes; at full capacity, though, the transaction multiple is a more reasonable ~1.5x (albeit still above where Rheinmetall trades).

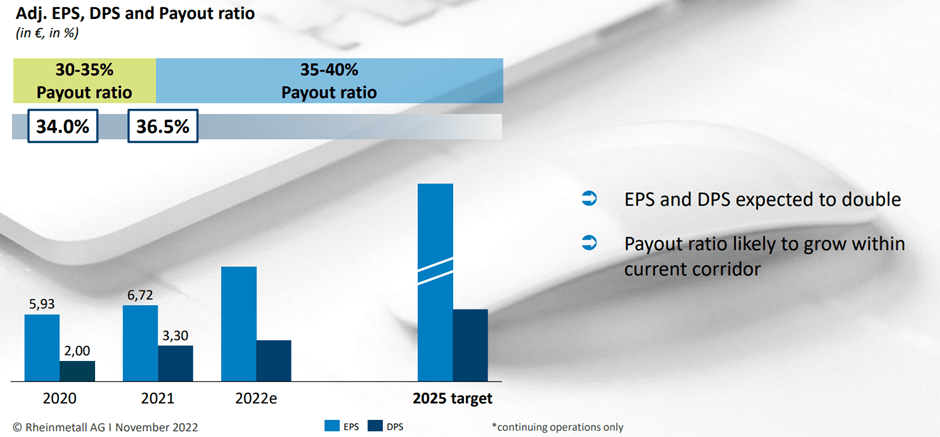

The pro-forma balance sheet should be fine as well – the pro-forma FY22 net debt/EBITDA would still be very manageable at ~1x, assuming an in-line EBITDA margin. With management also citing minimal investment needs at Expal, given its updated facilities, the company should retain capital allocation continuity. Recall from the last capital markets day presentation that the company was focused on capex through FY23 to support growth while also maintaining an investment-grade balance sheet. The target dividend payout at 35-40% also leaves ample balance sheet capacity, so Rheinmetall should be well-equipped to execute more M&A targets following the anticipated deal close sometime in Q2/Q3 2023.

Rheinmetall

Neutral Pre-Announcement as the Long-Term Thesis Remains Intact

Rheinmetall’s pre-announced result earlier this month isn’t a game changer but all else equal, the potential margin upside implied by the print is supportive for the stock. Over the mid to long term, the key driver remains the German government’s defense spending run-rate relative to the current ~2% of GDP, as the company stands to be a key beneficiary as the leading national defense contractor. Management has been making the right moves to capitalize – the recent Expal acquisition, for instance, adds a complementary portfolio while also diversifying beyond the German market.

The stock has re-rated over the last year amid the geopolitical uncertainty but still trades at an attractive ~12x fwd P/E, well below US contractors like Lockheed Martin (LMT) and Booz Allen (BAH), which tend to trade in the high teens. Going forward, all eyes will be on whether Rheinmetall makes it into the DAX following the Linde delisting; the incremental flow from a DAX inclusion presents re-rating potential.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment