halbergman

While Rexford Industrial Realty (NYSE:REXR) shares have been hit hard (-31% total return in 2022), prospects for the company remain bright as vacancy is below 1% in core markets while the outlook for supply growth remains limited. This bodes well for future same-store rental and NOI growth.

While shares are not cheap on current numbers at 24x 2023e FFO/share and an implied cap rate of just 4%, looking out a few years NOI is poised for significant growth as leases are marked to market. Despite what appears a high valuation at first glance, I believe Rexford shares can deliver annualized returns of 12-15% per year over the next three years.

Overview

Rexford Industrial Realty is a leading owner, operator, and developer of industrial real estate in the U.S., with an operating footprint of nearly 42 million square feet and another 3 million square feet under development or repositioning. Rexford is unique amongst industrial REITs in that it is concentrated entirely in one market, the infill Southern California region, widely considered one of the largest and most valuable industrial markets in the United States. Southern California is home to America’s most important ports (40% on containerized imports come through the regions ports).

Rexford Overview (Investor Presentation)

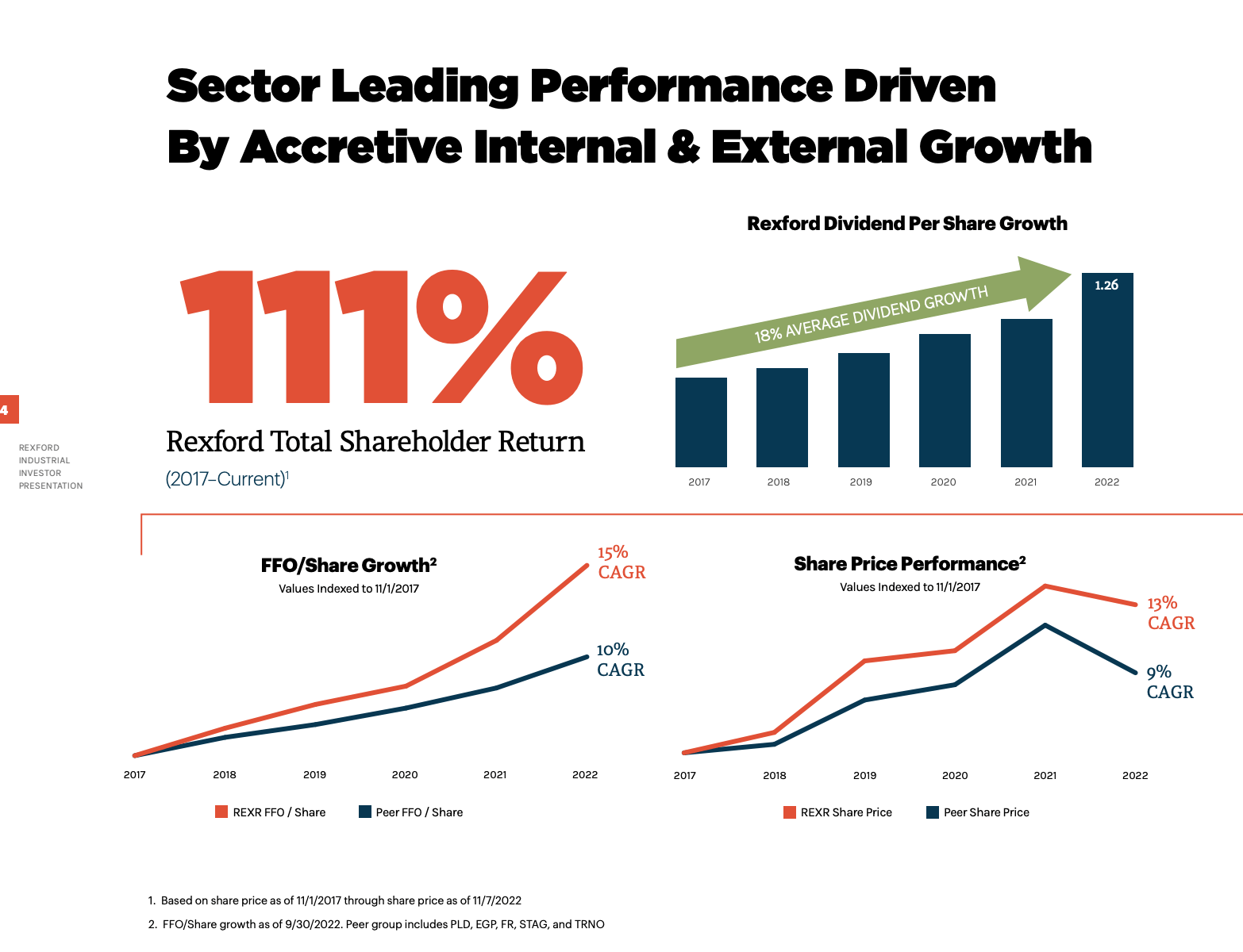

As shown below, Rexford has a phenomenal track record of creating value for shareholders with both same store and acquisitive growth driving shareholder returns.

Shareholder returns versus Peers (Investor Presentation)

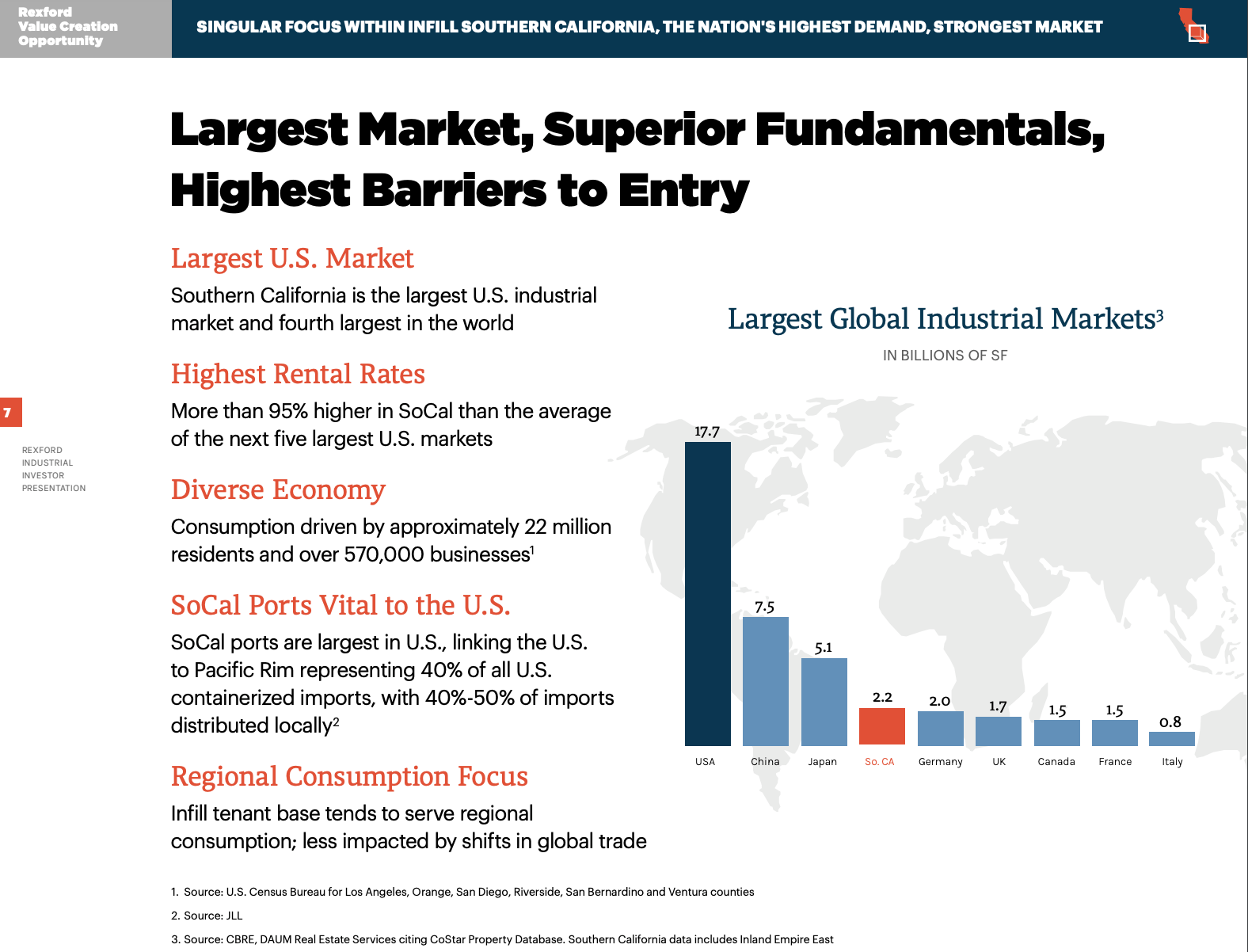

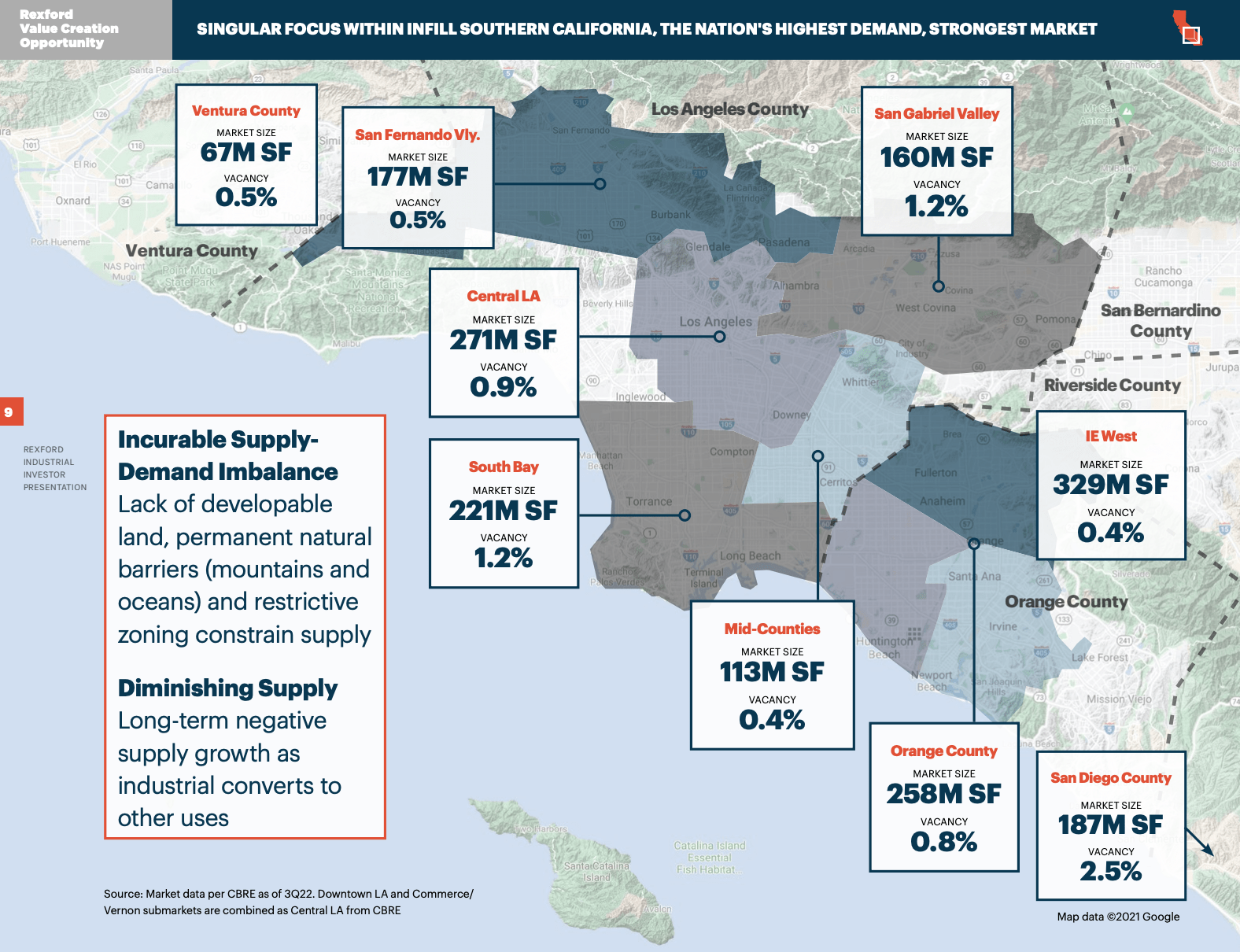

Supply – Very Favorable Dynamics

As you can see, there is very little vacancy across Rexford’s Southern California footprint. High property values, restrictive land use laws (zoning), and a history of industrial conversions to other uses have constrained industrial real estate supply in Southern California. This has led to sub 1% vacancy rates and soaring rental rates (year-over-year market rental rates have increased an astonishing 39%!).

Vacancy by Submarket (Investor Presentation)

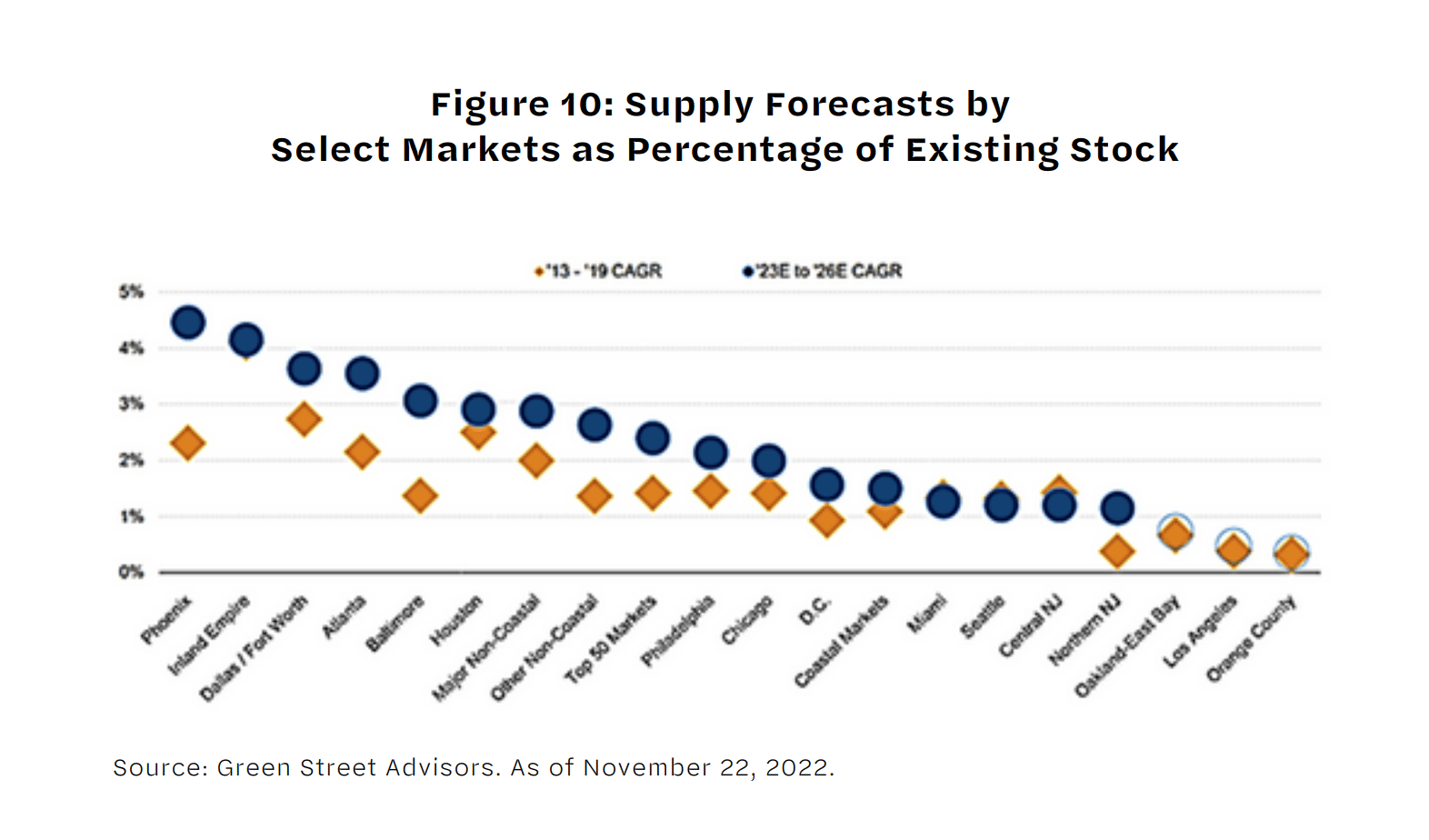

Under construction industrial real estate totals about 4% of the existing stock which (coupled with a weaker demand outlook) has caused some concern amongst investors in industrial real estate. However, as shown below, the outlook for supply growth in Rexford’s markets over the next three years is quite favorable with negligible new supply set to come online in Los Angeles and Orange County though further rent upside might face some pressure from new supply coming online in the Inland Empire.

Expected Supply Growth by Market 2023-26 (Green Street Advisors)

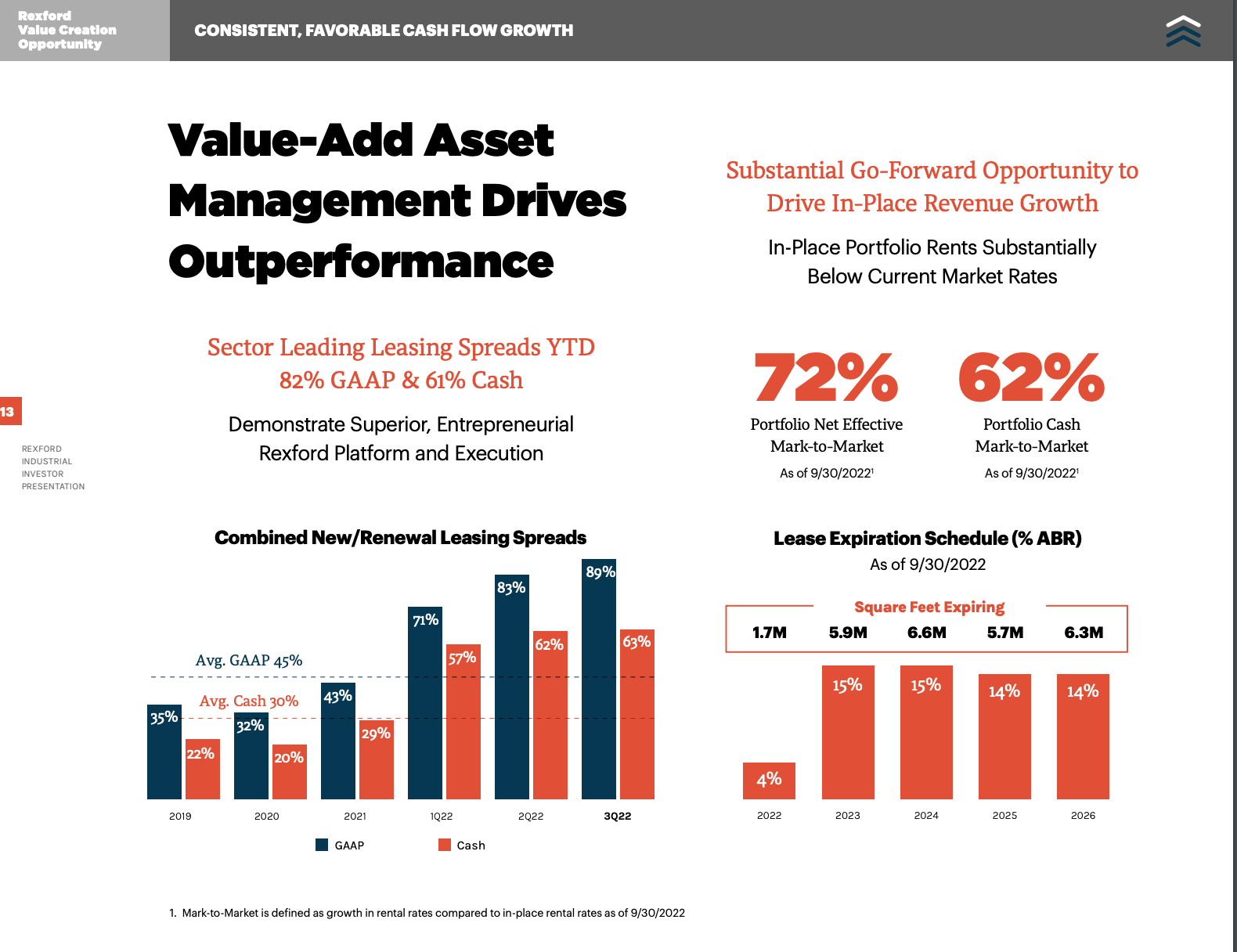

Significant Embedded NOI/FFO Growth

Leasing Spreads/ Lease Expiry Schedule (Investor Presentation)

As shown above, Rexford has seen gigantic increases in rental rates with blended cash leasing spreads of 60% thus far in 2022. With 14-15% of leases expiring annually for the next four years, Rexford will benefit as these leases are marked to market (portfolio-wide, Rexford estimates a cash mark-to-market of 62%, consistent with leasing spreads we’ve seen in 2022).

Portfolio-wide Cash Mark-to-Market (3Q22 Conf Call Transcript from Seeking Alpha)

Further, strong demand and limited supply have improved the terms of leases – in 3Q22, Rexford negotiated annual lease escalators of 4.4% (versus overall portfolio lease escalators of just over 3%).

Valuation and Expected Returns

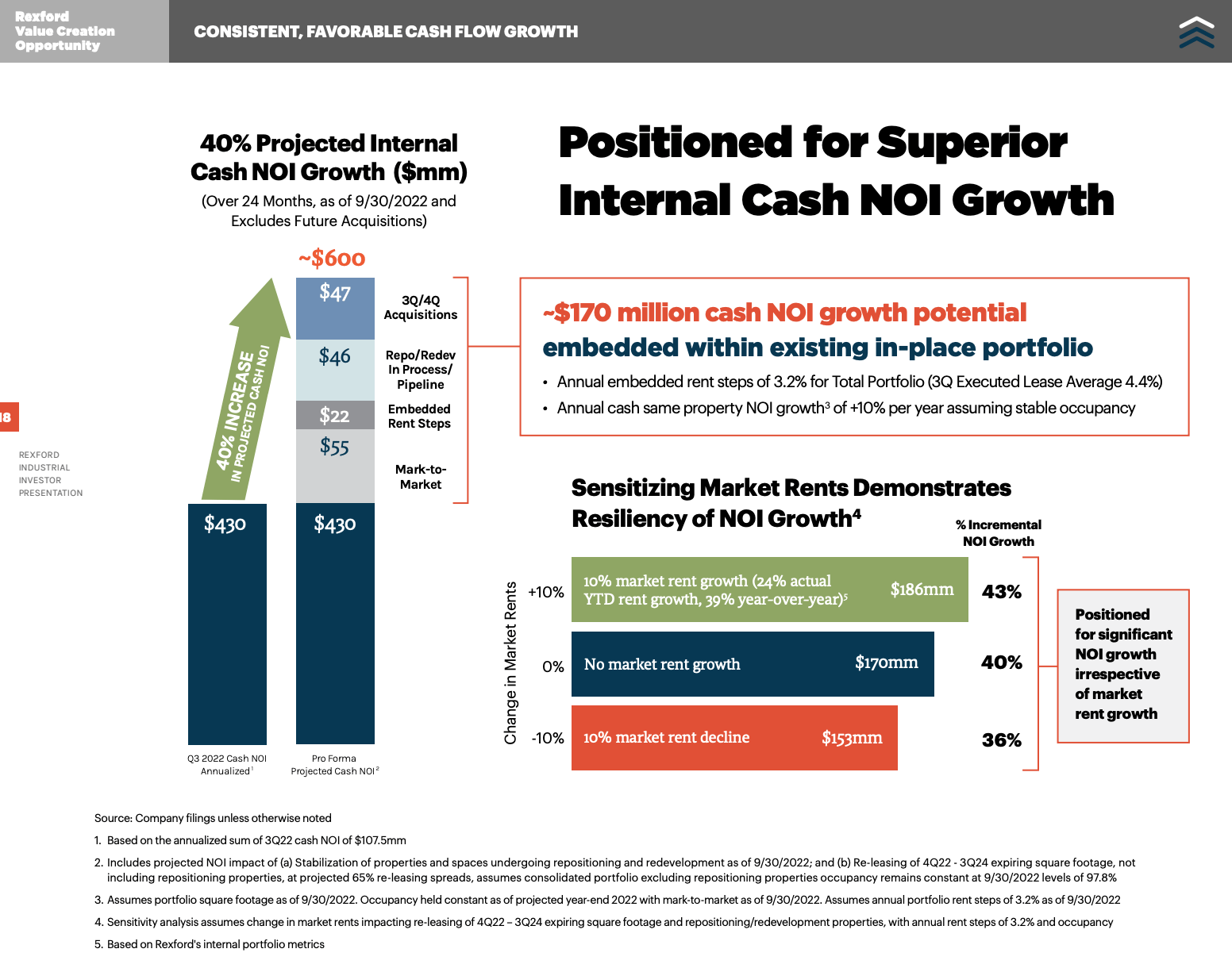

At $53.80, Rexford trades at a 4% implied cap rate on 2023 numbers which makes it one of the most expensive REITs around. However, Rexford is poised for exceptional growth between now and 2026. I expect the company will grow same store cash NOI by 13-14% per year from 2024-2026. To get to 13-14% NOI growth I simply assume 60% cash leasing spreads (marking them to current market rents) on the 14-15% of annual leases which expire annually and annual escalators on existing leases of ~3.5%. This high level of organic growth implies that Rexford’s NOI yield (implied cap rate) will approach 6% by 2026.

Expected Cash NOI Growth (Investor Presentation)

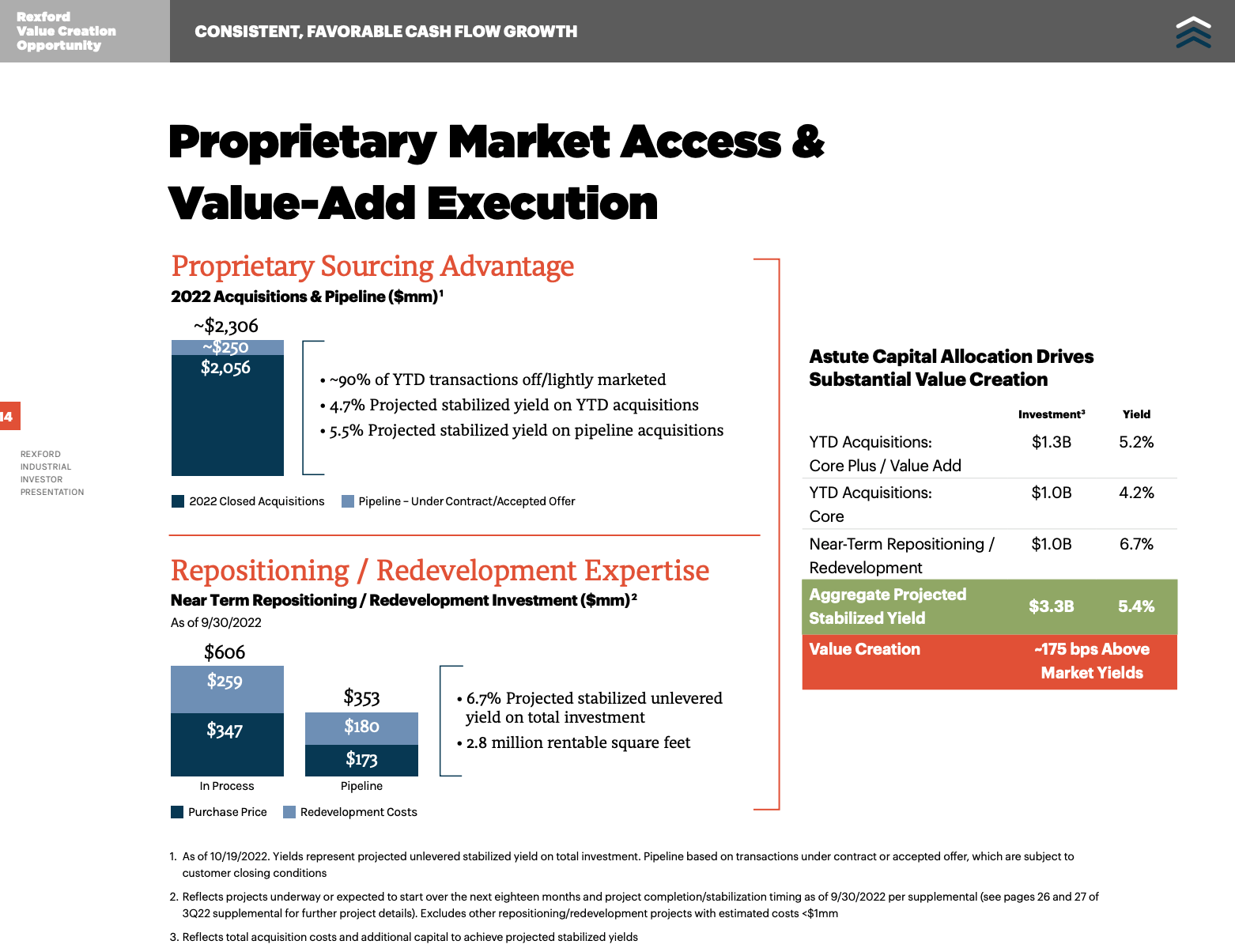

Should Southern California rental rates continue to grow, the company could do even better than what I outlined above. In addition to organic growth, Rexford will continue to acquire properties. As shown below, the company has historically created value through acquisitions and it is reasonable to expect this to continue going forward.

External Growth (Investor Presentation)

Looking out to 2026, it is likely that Rexford will see a significant slowdown in same store organic NOI growth. That said, I expect that beyond 2026 the company should still be a relatively fast grower, say 4-5% (escalators alone are trending towards this range). As such, it seems reasonable that Rexford should trade at an implied cap rate in the 4.5-5% range in 2026. And of course there is the external growth opportunity shown above.

Taken together, this suggests that Rexford shares could appreciate 30-40% over the next 3 years. Including its 2.3% dividend, this gets me to an expected annualized return of 12-15% per year.

Conclusion

While not dirt cheap, I believe Rexford can deliver 12-15% annualized returns to shareholders for the next several years. I consider this to be an attractive return given Rexford’s very low level of financial leverage (debt represents just 16% of total capital; debt to EBITDA is just 4.1x), high quality assets in a supply constrained market, top tier management and fantastic historical track record.

Be the first to comment