Justin Sullivan

Bankrupt Revlon (OTCPK:REVRQ) finally filed their Ch.11 reorganization plan that wipes-out current REVRQ shareholders, but unsecured noteholders are being “gifted”, subject to certain conditions, 5-year warrants or cash, which is a pleasant surprise. There still is the possibility of an alternative plan that would sell all the assets. Because not all the major stakeholders support the plan and there is continued litigation over the 2020 refinancing transaction, I seriously doubt they will be able to meet the April 17 milestone to have their plan declared effective. This proposed plan also completely wipes-out Ron Perelman’s billions invested in Revlon.

Outrageous Legal/Professional Fees

Usually, I make comments about legal/professionals fees near the end of an article, which often means that readers don’t see the comments because many don’t read the entire article, but I feel it is appropriate to put this discussion at the top of this time. According to Revlon’s business plan that was filed as an 8-K on December 19, the total estimated professional fees are a staggering $279 million (page 23). Jaw-dropping, in my opinion. To put this number in some perspective it works out to be about $5.14 per REVRQ share. Just for the sake of discussion, the $279 million would result in a 63% cash recovery for unsecured noteholders, assuming all the money went to the noteholders. This is close to the total fees for the former bankrupt Sears Holdings Corp. (formerly SHLDQ). That case lasted over four years and was extremely complex. Some shareholders may think that this high figure is insulting, especially since one of the major objections to having an official equity committee appointed was that it would be costly because of legal/professional fees billed to the equity committee.

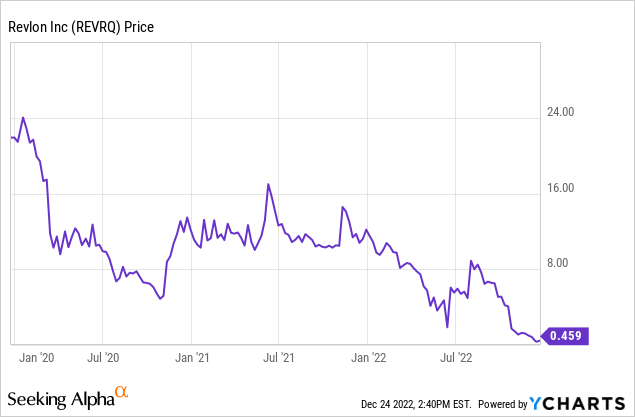

Revlon Stock Price – Three Years

Ch.11 Reorganization Plan and Disclosure Statement

Under the original DIP milestones, the Ch.11 reorganization plan was supposed to be filed by November 15, but a negotiated modification allowed the plan (docket 1253) and disclosure statement (docket 1254) to be filed by December 22. The restructuring support agreement (docket 1216) was filed on December 19. Under the terms of the plan, there is going to be a rights offer to raise up to $650 million in new cash and a total debt reduction, including DIP financing, of approximately $2.7 billion.

Sorry, but I have very serious doubts about this plan. This is one of the worst plans and disclosure statements I have ever seen, and I have been in this business for many years. It looks like they just combined a large number of ideas and tossed them together. There are so many “either this or that” conditions to make it almost meaningless/useless, in my opinion. Plus, many critical words used are not even defined or not defined sufficiently to give them proper meaning.

The disclosure statement mentioned that the Official Unsecured Creditor Committee and the Ad Hoc Group of BrandCo Lenders (to see members of this group and what Revlon loans/notes they own read docket 1115) support the plan, but I did not see any mention that OpCo term loan holders are supporting the plan. Since OpCo term loan lenders are getting 50% of the equity in the new Revlon company and 50% of the equity subscription rights as recovery it may result in an objection because you really can’t force secured lenders to accept equity under the Bankruptcy Code. They have the right to make a credit bid for the assets/collateral securing their loan under section 363(k), but there has been some case law that tossed out this as an absolute right. (The legal details of the 363(k) issue are beyond the scope of this article.) There is currently litigation (No. 22-01167, AIMCO CLO 10, Ltd., et al v. Revlon, Inc., et al) over what collateral actually secures OpCo term loans and what secures BrandCo loans. Until this litigation is settled either via negotiation or a trial, I just don’t see how a plan can be confirmed by the court. There was a status conference set for December 21 on this litigation, but it was cancelled. (Note: the Citibank transfer “error” has been finally settled.)

In theory, you only need one class to vote to accept (2/3 dollar amount of the class’ claim and a majority of claimholders with that class) a Ch.11 reorganization plan for the court to confirm a plan, but the plan still must conform to section 1129 of the Bankruptcy Code. The OpCo term loan holders are being led by the Ad Hoc Group of 2016 Term Loan Lenders (to see members of this group and what Revlon loans/notes they own read docket 789).

The plan raises $650 million new cash via a rights offer that is priced at a 30% discount to the plan equity value. Those backstopping the rights offer get 30% and the remaining 70% is split 50/50 between the OpCo term loan holders and 2lien BrandCo claim holders. These two claim holder classes are also splitting the new equity. (All of which are subject to certain conditions.) While the plan does reduce much of their debt there is still way too much debt after they emerge from bankruptcy, in my opinion. There will be $1.419 billion “take-back” term loans issued to replace some current term loans and a $308 million ABL, which is expected to already be drawn by $119 million on the emergence date. I think they should increase the rights offer amount and sell some underperforming assets/brands to raise more cash.

There might be two reasons why they even filed such a problematic Ch.11 reorganization plan and disclosure statement. First to use it as a negotiating tool with OpCo term loan lenders. Second, and perhaps most importantly, to reassure vendors that they are in fact getting recoveries. The administrative claim holders are getting full recoveries and general unsecured claim holders are getting a significant recovery. This reassurance may encourage vendors to deal with financially weak Revlon going forward.

The proposed plan allows for an alternative plan that would sell Revlon’s assets. For the sake of simplicity, I will only cover the difference in recoveries for REVRQ shareholders and unsecured noteholders.

Revlon Shareholder Recovery

REVRQ shareholders are getting no recovery, and this would include Ron Perelman who owns 85.2% of the stock, which will become completely worthless on the plan’s effective date. Some were hoping that Perelman would be able to negotiate a deal so REVRQ shareholders could at least be able to participate in a rights offer. There is a rights offer, but shareholders can’t participate in the rights offer.

The Revlon shareholders are called holders of interest in the disclosure statement and are put into Class 12 – the lowest class. REVRQ shareholders’ treatment is:

Holders of Interests… shall receive no recovery or distribution on account of such Interests. On the Effective Date, all Interests …will be canceled, released extinguished, and discharged, and will be of no further force or effect.

Repeat – no recovery and shares will be cancelled. The REVRQ shares should continue to trade until the plan is effective, which means that the stock will trade for many more months. I would not be surprised if there still could be some very irrational meme trading spikes until it is finally cancelled. There was some reaction to a completely incomprehensible docket (docket 1217) filing on December 19 about some “reverse takeover” written by what looks to be a Canadian individual who has zero understanding of our laws. Things like this could cause additional irrational trading.

Unsecured Noteholder Recovery

The recovery for the 6.25%’24 unsecured notes (CUSIP 761519BF3) is rather complex. Noteholders are being “gifted” 5-year warrants. This recovery is considered a gift because, under the absolute priority rule (section 1129(b)1), they should get nothing because some higher priority classes are not getting full recovery.

This recovery is subject to a number of conditions, such as the court not ruling against this gift. If a higher priority claim holder files an objection to the gifting, the court could rule against the gift. Second, the “Creditors’ Committee Settlement” must be satisfied, but the filed documents do not completely define the terms related to this specific settlement. Third, noteholders would not get warrants if an alternative plan selling the assets is eventually confirmed. They would instead get cash for the theoretical value of the warrants. Since warrants almost always trade much higher than fair value, noteholders, in my opinion, would be much better off under the current plan instead of the alternative plan that sells the assets. Last, if noteholders as a class (Class 8) vote to reject the plan, they get no recovery at all.

RSA Milestones

*February 6 – Court order approving the disclosure statement

*February 14 – Court order approving the backstop motion

*February 20 – Solicitation of votes to accept or reject the plan begins

*April 3 – Bankruptcy court confirms the plan

*April 17 – Plan effective date

All of these dates could be amended.

Business Plan

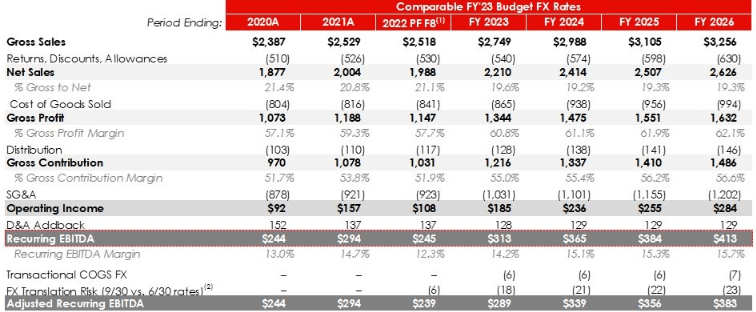

Revlon finally filed their business plan on December 19. The projections are not that encouraging. The projections are based on a 1.0% GDP increase in the U.S. in 2023, 0.5% increase in Europe/Middle East/Africa, and 4.9% increase in Asia/Pacific.

Profit/Loss Annual Projections

sec.gov

Revlon will eventually file an amended disclosure statement at some point that includes a valuation analysis under the proposed plan and financial projections. Sorry to say, but these numbers don’t really impact current REVRQ shareholders because their stock is being cancelled. The numbers do, however, impact current unsecured noteholders who are trying to estimate a value for their 5-year warrants.

Conclusion

While some were hoping that Perelman would negotiate some deal for REVRQ shareholders, it is not a complete surprise to most that shareholders are getting no recovery and shares will be worthless on the plan effective date. Unsecured noteholders were somewhat surprised that they are getting any recovery via a “gift” of 5-year warrants.

I expect that the Revlon bankruptcy case will drag on for a long time and the litigation over the 2020 financing deal will have to be settled before a Ch.11 plan is likely to be confirmed by the court. The current plan and disclosure statements are most likely going to be amended multiple times over the next few months.

I continue to rate REVRQ shares a sell and the unsecured notes as a hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment