Onfokus

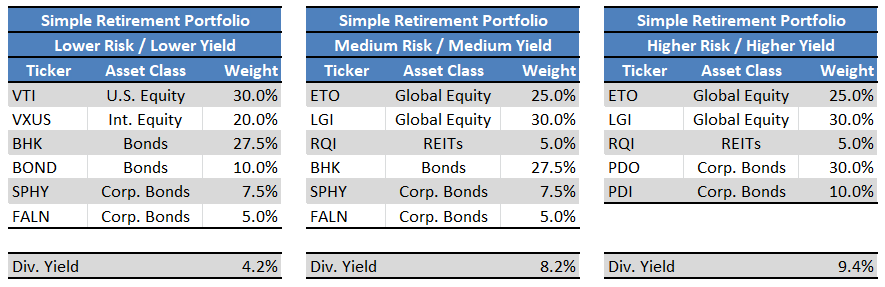

I introduced the Simple Retirement Portfolios more than two years ago. Portfolios are meant to provide retirees with a simple, yet effective way to invest their retirement savings, with varying levels of risk, yield, and passive / active exposure. Portfolios hold a diversified set of equity and fixed income funds, with diversified exposure to most relevant asset classes. Portfolios are as follows.

SeekingAlpha – Chart by author

I’m doing semi-regular updates on these portfolios and their performance. The following article is the (belated) update for 2022.

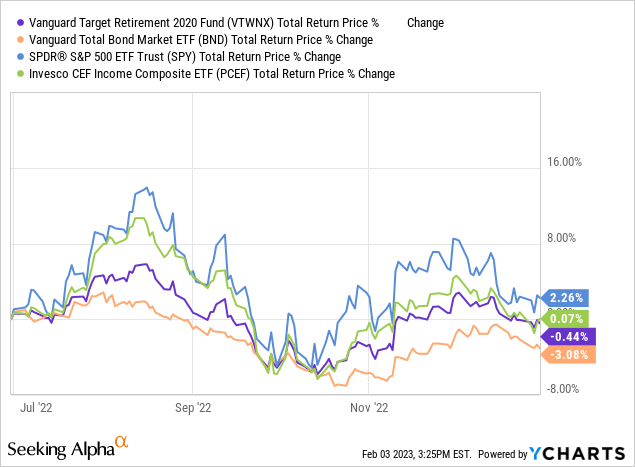

Most asset classes and investment funds were down in 2022, and these portfolios, and their underlying funds, were no exception. All portfolios were down double-digits, as were most funds. All portfolios moderately underperformed their benchmark on a price basis, slightly underperformed on a NAV basis. Underperformance was due to leverage, greater exposure to underperforming international and European equities, lower exposure to energy and other inflation-hedge assets, and widening discounts to NAV.

On a more positive note, all portfolios have outperformed their benchmark since inception, due to savvy selection of funds and greater exposure to high-yield corporate bonds.

SeekingAlpha – Chart by Author

In general terms, results are consistent with recent market conditions and events. More or less everything was down in 2022, including most lower-risk asset classes like treasuries. Unless you went cash, playing it safe meant significant capital losses during the year without significant dividends or strong (prior) returns to compensate. Focusing on riskier, higher yielding investments has been the right call for a few years, including for these portfolios.

In my opinion, the risk-return profile of the medium risk and higher risk portfolios is quite strong, and very compelling. Both have significantly outperformed their benchmark since inception, with only a moderate increase in losses during this most recent downturn. Long-term income investors could even ignore these losses, and focus on distributions and long-term capital appreciation and total returns. On the other hand, the risk-return profile of the lower risk portfolio looks quite weak, as risks are moderately higher than average, while returns are only very marginally higher.

Simple Retirement Portfolios – Overview and Analysis

I’ll start with a brief overview of the construction and rationale behind the portfolios. Feel free to skip this section if you’ve read my previous articles on the subject.

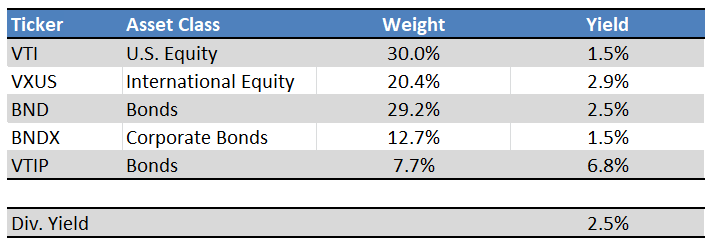

The Simple Retirement Portfolios are based on the Vanguard Target Retirement 2020 Fund (VTWNX). VTWNX invests in a diversified portfolio of low-cost fixed income and equity index funds and is aimed towards recent retirees. Asset allocations change every quarter to reduce risk as retirees age.

Balanced funds, including VTWNX, generally provide retirees with superior returns than equity index funds. This includes those indexed to the S&P 500, as the said index is simply too volatile to fund the monthly income needs of the average retiree. I’ve done the math on this here.

VTWNX seemed like a perfect low-risk fund for retirees, so I used it as the basis for my model portfolios. The portfolios used VTWNX’s holdings in May 2020 as a starting point. Current holdings are only marginally different. These were as follows:

Vanguard Corporate Website To construct the portfolios, I simply swapped some of VTWNX’s holdings for stronger, higher-yielding alternatives with the potential for market-beating returns.

I created three portfolios, some more closely tracking their benchmark than others.

A lower-risk portfolio with few changes meant to closely track VTWNX but with the possibility of some excess returns and income.

A medium-risk portfolio with some more changes, somewhat tracking VTWNX, and with the possibility of excess returns and income.

A higher-risk portfolio with significant changes, less concerned with tracking VTWNX, and with the possibility of substantial excess returns and income.

The resultant portfolios were as follows.

SeekingAlpha – Chart by author

Simple Retirement Portfolios – 2022 Performance Analysis

I wrote about these portfolios and their performance in mid-2022, and nothing much has changed since, as most asset classes have been flat these past few months. Equities saw meager gains, bonds some losses, with most balanced funds and income-producing CEFs flat for the year.

I’ll be going through their performance once again, but bear in mind, not much has changed since.

Lower Risk / Yield Portfolio

The lower risk / yield portfolio moderately underperformed its benchmark in 2022, with price losses of -20.9% versus -14.2%.

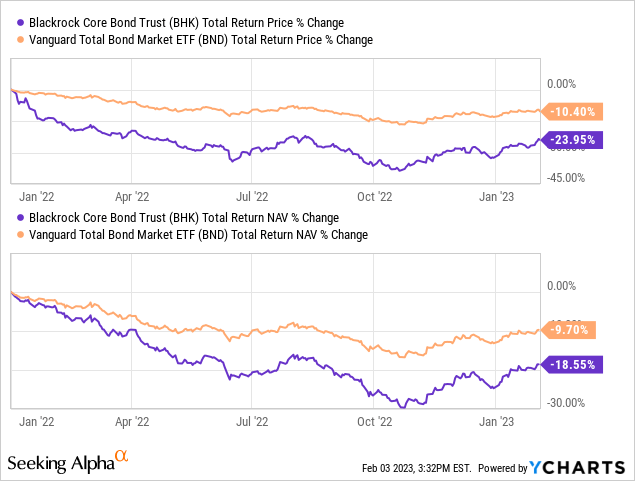

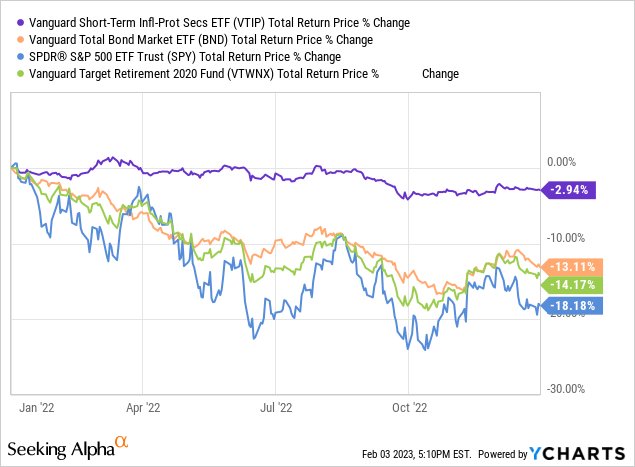

Losses were driven by BHK underperformance and lack of exposure to inflation-hedge investments like the Vanguard Short-Term Inflation-Protected Securities ETF (VTIP).

BHK significantly underperformed its benchmark due to narrowing discounts, use of leverage, and overexposure to underperforming long-maturity investment-grade corporate bonds. BHK had seen lower losses and underperformance during prior periods of rising rates, due to savvy positioning and market timing. It seems conditions in 2022 caught them off-guard, as was the case for many fund managers.

Vanguard Target Retirement Funds include sizable investments in short-term inflation-protected securities, or TIPs, through an investment in VTIP. Said investment serves to partially hedge these portfolios against inflation, as well as reduce their overall risk profile (short-term TIPs are incredibly safe securities). VTIP generally yields very little, and has extremely low long-term expected and realized returns, so including the fund serves to lower long-term returns.

My portfolios don’t include VTIP or similar funds, as I thought that their low long-term expected returns outweighted their inflation-hedge characteristics and low level of risk. VTIP performed quite well in 2022, for obvious reasons, so excluding the fund led to underperformance during said year, and was definitely the wrong call during said year. VTIP’s long-term returns are still extremely low, so excluding the fund makes a bit more sense overall / long-term.

In general terms, the risk-return profile of the lower risk portfolio is quite mediocre. Returns are functionally identical to those of its benchmark, while risks are moderately higher. Returns were also significantly below the other two portfolios, while risks / losses were only slightly lower. Results are consistent with recent market conditions and events, as most lower-risk assets have performed in a similar manner.

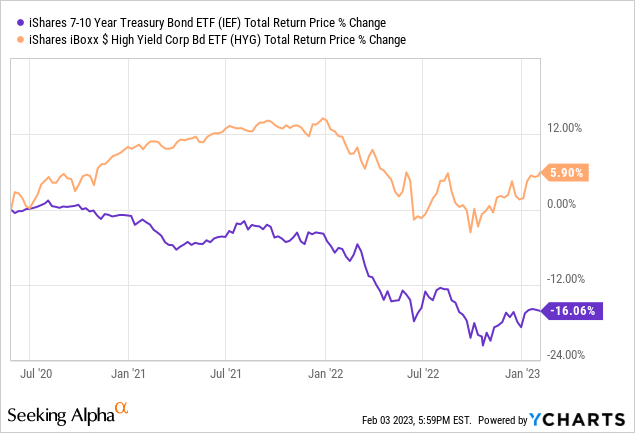

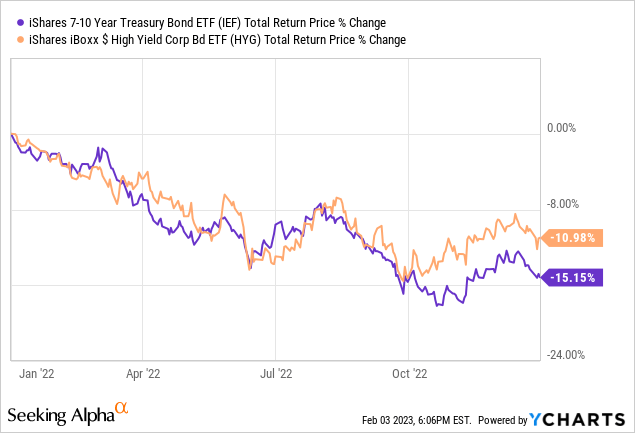

As an example, high-yield corporate bond returns have vastly outpaced treasury returns since the creation of these portfolios.

High-yield corporate bonds suffered lower losses in 2022 as well.

Lower-risk assets have generally performed disastrously these past few years, with weak returns, above-average risk, and mediocre risk-return profiles. Funds and portfolios focusing or overweighting these assets have performed quite badly too, including my own lower risk portfolio. Cash has been one of the few exceptions to this trend, but these portfolios don’t hold cash or cash-like investments.

Medium Risk / Yield Portfolio

The medium risk / yield portfolio significantly underperformed its benchmark in 2022, with price losses of -25.6% versus -14.2%.

Losses were driven by the aforementioned BHK underperformance, lack of exposure to inflation-hedge investments and asset classes, widening discounts to NAV, and CEF leverage.

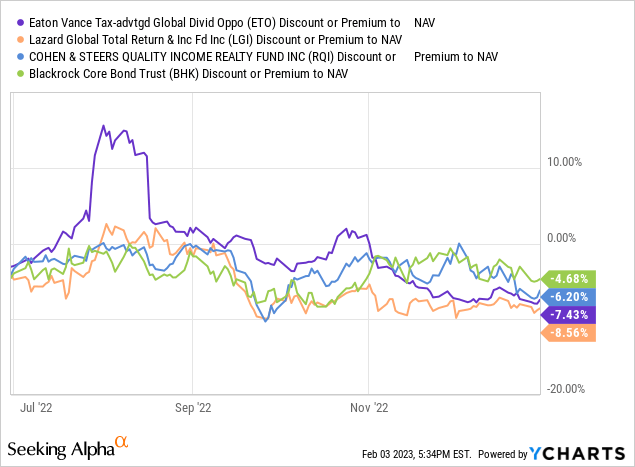

Discounts were key, and responsible for around half of all underperformance.

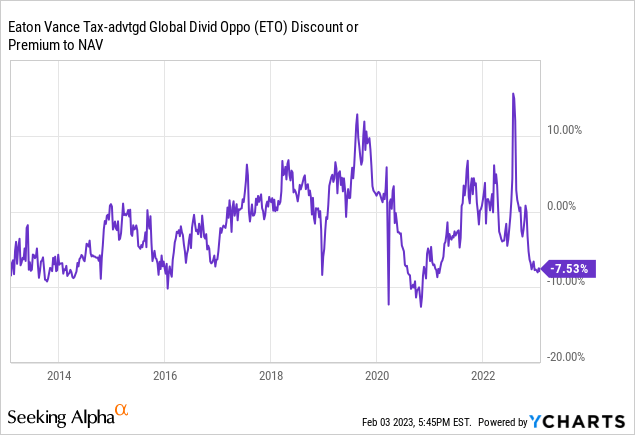

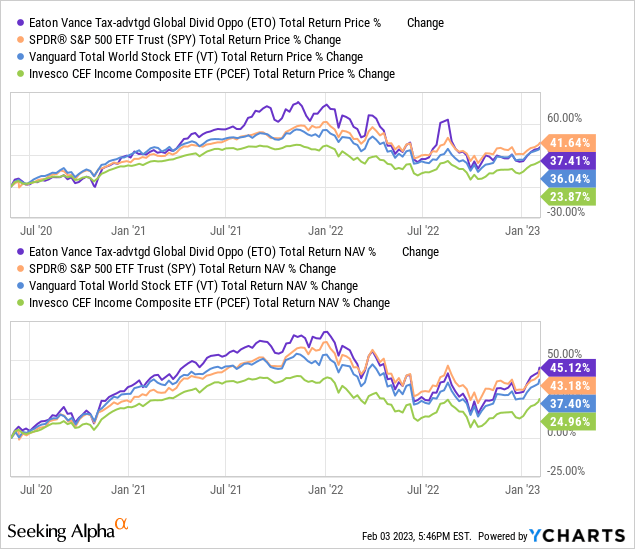

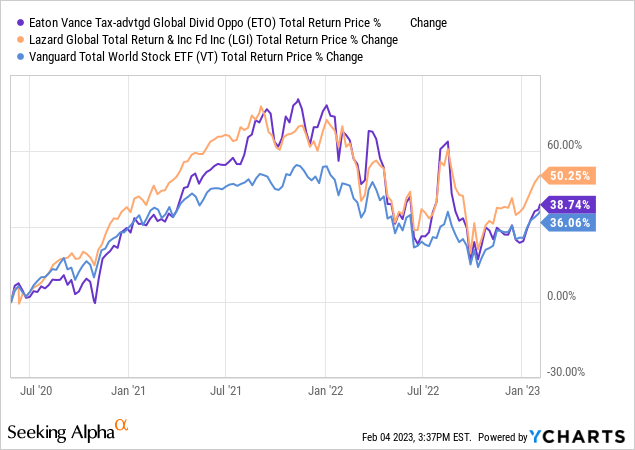

Although widening discounts were a detriment to investors in the past, they are something of an opportunity for prospective investors. The CEFs above all have outstanding performance track-records and are currently trading with decent, if not huge, discounts. The Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund (ETO) looks particularly attractive right now, with the widest discount in close to a decade.

ETO has outperformed U.S. equities, global equities, and the average income-producing CEF on a NAV basis since including the fund in these portfolios. ETO has outperformed these same asset classes, except U.S. equities, since the same. ETO is an outstanding fund, and is currently trading with a reasonably good price.

I last covered ETO here.

In general terms, the overall risk-return profile of the medium risk / yield portfolio is quite strong. Said portfolio has achieved annualized returns almost twice those of its benchmark, 4.9% versus 2.6%. Risks and volatility are higher too, but long-term investors can generally ignore short-term fluctuations in CEF discounts, and income investors might choose to focus on distributions over capital levels (at least in the short-term).

Higher Risk – Higher Yield

The medium risk / yield portfolio significantly underperformed its benchmark in 2022, with price losses of -25.9% versus -14.2%.

Losses were driven by CEF leverage, widening discounts to NAV, and lack of exposure to inflation-hedge investments and asset classes. The same reasons as for the medium risk portfolio.

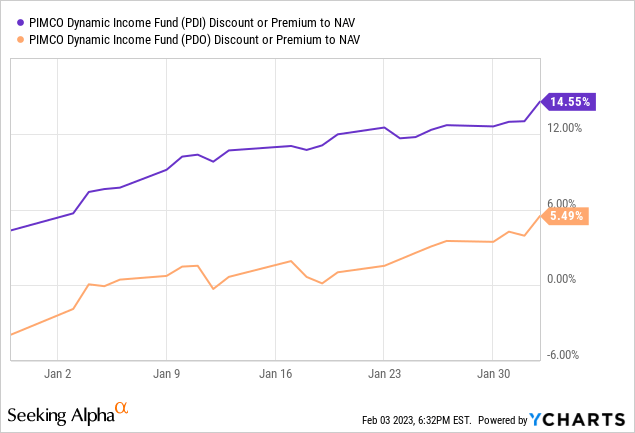

Two portfolio funds, the PIMCO Dynamic Income Opportunities Fund (PDO) and the PIMCO Dynamic Income Fund (PDI) have seen significant increases in their premiums these past few weeks. Current premiums are quite elevated, elevated enough that I would not be a buyer at these levels.

As with the medium risk / yield portfolio, the overall risk-return profile of the higher risk / yield portfolio is quite strong. Said portfolio has achieved annualized returns since inception more than twice that of its benchmark, 6.5% versus 2.6%. Risks were higher too, but as with the medium risk portfolio, income investors can focus on distributions, while long-term investors might focus on long-term capital appreciation and returns.

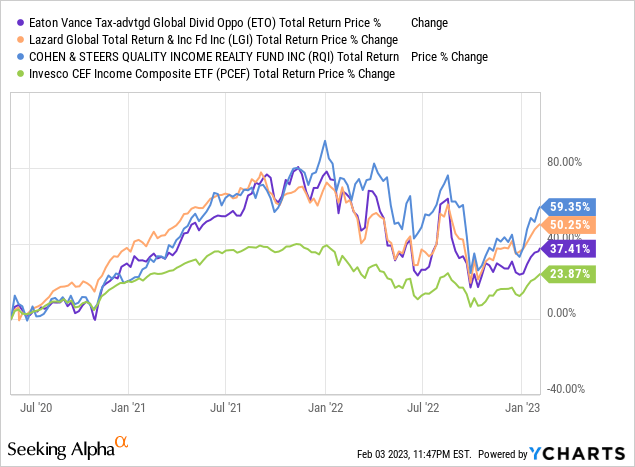

As a final point, this portfolio exclusively consists of CEFs:

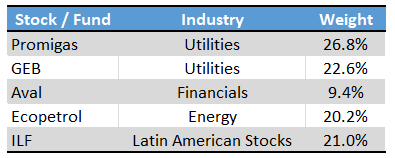

Juan’s Portfolio

Long-time readers know I’m rarely invested in the funds I cover. This is mostly because I focus on funds and investments for income investors and retirees, and I’m still decades away from retirement. I have shared my personal portfolio a few times in the past. This centers on Colombian stocks and a Latin American index ETF, on valuation grounds. Portfolio and performance is as follows.

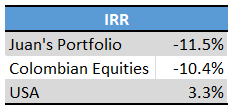

Chart by author Chart by Author

As can be seen above, my personal portfolio has significantly underperformed the S&P 500. Underperformance was almost entirely due to Colombian / Latin American underperformance. Fundamentals remain strong, so I’m confident performance will improve moving forward, although I’ve said and thought this for a while.

Besides issues of valuation and fundamentals, the portfolio above makes sense given my personal circumstances. Thought to share these with (interested) readers. These might not be all that relevant for those looking for retirement funds or portfolios, but they might help explain why I made these portfolios, why I rarely invest in the funds I cover, and why I’m focusing on Colombian stocks.

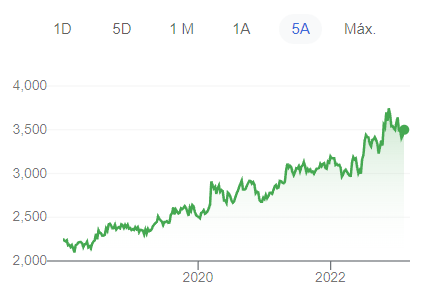

I was born and raised in Colombia, but I’ve lived abroad for most of my adult life. Lived and studied in Guatemala, Spain, Canada and, well, Colombia, obviously. Started writing for SeekingAlpha in Canada six years ago, although feels like it was yesterday. I always imagined I would settle down in Canada, and that was the plan, but I missed my family, and then this happened:

Google

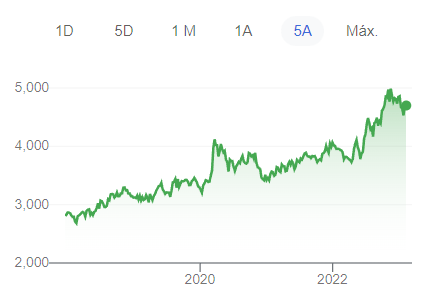

That graph is CAD to COP and shows the Colombian peso losing a lot of ground these past few years. USD to COP shows the same thing.

Google

With that in mind, I decided to move back to Colombia. Barranquilla specifically. I had some savings and some income from SeekingAlpha, and although it wasn’t a lot of money, the exchange rate was very favorable, and it was more than enough to live comfortably over there, and perhaps buy my own place. Being completely honest, I wasn’t sure it was the right choice at the time, but I definitely think so today.

So, moved back to Colombia, continued writing for SeekingAlpha, and started doing some consulting with a local company. Bought an apartment in 2021, for less than a downpayment for a house in Vancouver, or any other large North American city. A couple of pics, looks (and is) much larger in person.

Juan Juan

About a year later, heard about a new construction project nearby. It seemed very interesting, and as my income continued to grow I could afford a larger, newer apartment. Signed the papers on that one last year, they’ll start construction next month. No pictures of this one although I do have the floor plan.

Juan

In between moving to and from Canada, buying an apartment in Colombia and paying for a second apartment here, I’ve rarely had the spare cash to invest heavily in stocks. Besides an investment in the iShares Latin America 40 ETF (ILF), most excess cash remains here or is converted into pesos, as the exchange rate is very favorable right now, and as I’d rather avoid foreign currency fluctuations with money earmarked for the apartment. I’ll probably sell my investment portfolio in 2024, to minimize any future mortgage (rates are +15% here right now). Although these investment decisions do take into consideration market fundamentals, personal circumstances and other factors predominate.

As should be clear from the above, my personal circumstances, and hence investment decisions, are very different to those of the average SeekingAlpha subscriber. Due to this, I rarely write about my own investments and investment decisions, as these would be of little interest or use to most of my readers here. Instead, I focus on topics and investments which are of greater interest and value to readers. I have lots to say about, say, the impact of rising rates on bond ETF dividends, and I think my readers find topics like that important and interesting, as do I.

Notwithstanding the above, I wanted a clear track-record of my performance, hence the Simple Retirement Portfolios. A bit silly, but I do think these are strong portfolios, and I do think that there is some value in having a clear, explicit performance track-record. Investors know that my top equity picks have outperformed their benchmark:

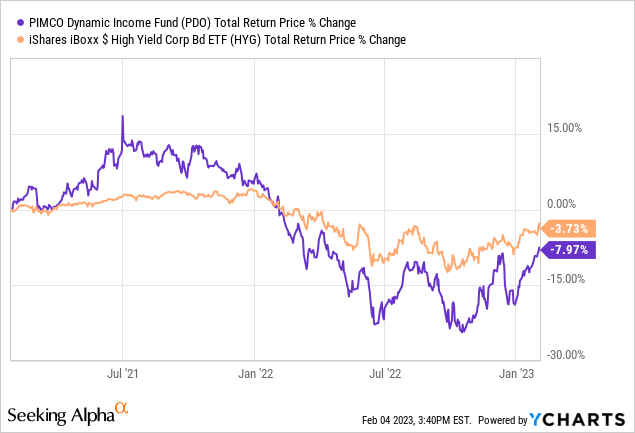

while my top high-yield corporate bond pick has not (so far!):

I will keep writing these portfolio articles so as to have a clear performance track-record for investors, and for myself. Hopefully I get to invest in some of these next year (or buy a third, larger apartment next).

Conclusion

The Simple Retirement Portfolios provide retirees with a simple way to invest and save during their retirement, and have generally performed well in the past. I believe that the funds selected and portfolios created will outperform in the coming years. Hopefully, the information here was of use and interest to readers and investors.

Be the first to comment