Abu Hanifah/iStock via Getty Images

Co-produced with Treading Softly

I was looking at the value of various plots of land the other day, and one large plot jumped out at me. It was significantly cheaper than the surrounding for-sale plots. It wasn’t wasteland or swamp. Not a toxic landfill or poisoned. No one had been murdered there – or if they had, they hadn’t been discovered.

The issue at hand? The property had no direct access. To gain access, you were required to cross over another landowner’s property to reach this one. Its value was heavily impacted simply by the extreme difficulty of accessing it.

At times inaccessibility can drastically impact the value of something, for better or worse.

Most people who hit “millionaire” status do so in their retirement accounts. Why is this? There are two factors at play in most cases:

1. It’s one of the few places people automatically save money – having it withheld from their paycheck means they don’t “miss it.”

2. It’s difficult to touch the money locked away in there.

It isn’t easy to save $1 million, but it’s something that is achievable for those who are diligent about taking advantage of employer matching programs and are willing to sock away more than the minimum.

If one of these diligent savers that reached $1 million decided to apply the 4% withdrawal rate prescribed in the “Safemax” methodology, they’d have about $40,000 in annual income. That’s great, but it seems like quite a bit of sacrifice for decades to receive a relatively small amount of income.

When it comes to income investing, you can do a whole lot more with a whole lot less. Within our High Dividend Opportunities Model Portfolio, we aim for an overall portfolio yield in excess of 9%. This means you could generate $40,000 with $445,000 – over 50% less than a millionaire using the 4% withdrawal process.

Sounds much easier to achieve, doesn’t it?

Even if you have $1 million in your retirement savings, that’s a massive difference in annual income by using our Income Method.

Let’s look at two excellent income picks to include – among a minimum of 42 income investments to make a holistic income portfolio.

Let’s dive in.

Pick #1: EPR – Yield 8.6%

One of the coolest things about investing is having ownership over companies that you use. As I’m out living my life and spending money on this or that, it’s like the ultimate rewards program because so much of it filters back into my dividends! My wife is absolutely sick of the words, “Hey, I own this place!”

There are a lot of reasons to own EPR Properties (EPR). One of the most important is that their properties are a lot of fun to visit.

If you’ve read about EPR at all, you are familiar with their movie theaters. EPR is the largest movie theater landlord in the U.S. What is the reason why EPR is so cheap right now? Cineworld (OTCPK:CNNWQ), the parent company of Regal Cinemas, has filed for bankruptcy and is in the process of restructuring.

During the COVID pandemic, movie theaters were hit exceptionally hard. Both from the obvious fact that people weren’t going to movies, but also are hurting from Hollywood suspending content production. The content pipeline has not fully recovered yet, with only 46 movie releases from January to August 2022, compared to 75 during the same period in 2019. So while audiences have shown up for a few blockbusters like Top Gun: Maverick, there just wasn’t as much content in 2022 as there was pre-COVID. The schedule for 2023 is expected to be more normal, but buckling under a mountain of debt taken on just to survive, that wasn’t quick enough for Cineworld.

What does this mean for EPR? Not as much as many seem to think. Cineworld has continued to pay rent through the bankruptcy process, and any locations where it continues operating will keep paying rent. Whatever the company does with its debt obligations or equity holders is of no concern to EPR. EPR is a landlord and will collect rent from whoever owns Regal. Cineworld does have the right to reject certain leases. So far, it has only identified three EPR-owned properties (EPR owns 173 theaters) on which it wants to reject the lease (Source: PDF download). The bankruptcy is expected to be concluded in the first half of next year, providing a potential catalyst for EPR shares to recover as the financial impact of the Cineworld bankruptcy is likely to be minimal.

Theaters account for 41% of EPR’s annualized EBITDAre. So while they get the most attention, EPR has many properties in other sectors.

- Eat & Play: EPR is a major landlord for the popular “Top Golf” and owns several “family entertainment centers” that include arcade games, go-karts, and bowling.

- Attractions: Indoor/outdoor waterparks, amusement parks, and indoor skydiving centers.

- Ski Resorts: EPR owns several ski resorts managed by Vail Resorts (MTN).

- Other Experiential Properties: EPR owns three museums, a hot springs resort, a casino, and specialized destination lodging.

EPR is a REIT that caters to experiences. Something that was terrible in a world where everyone was staying home. Yet, despite going through a period where its tenants were completely shut down, EPR managed to exit the pandemic without taking on additional debt. EPR didn’t have to issue equity and dilute shareholders. In fact, it was buying back shares in the early days of the pandemic. EPR’s management navigated the difficult times and is now focusing on growth.

EPR pays a monthly dividend and is trading at bargain prices since Cineworld filed for bankruptcy. We are buying the dip, confident that the impact of the bankruptcy will be far less than the market fears.

Pick #2: AGNC – Yield 13.4%

Homes are expensive, and most people who buy homes need to take out a mortgage to afford it. Even those who could afford to pay cash often take out mortgages. Why? For most people, a mortgage is the lowest interest rate debt they can take out. They can use their home as collateral and take out large amounts financed over 15 or 30 years.

Homeownership has long been synonymous with “The American Dream.” A person’s home is their castle. The government has been involved with ensuring that “average” Americans can obtain mortgages, this has led to a unique mortgage system in the U.S. and some unique investment opportunities.

The biggest problem with mortgages from a lender’s perspective is time. When a lender makes a loan, they must provide the cash up front and get paid back slowly over time. 15-30 years is a very long time to tie up capital. If a lender makes too many of those loans, they quickly don’t have any cash to provide to the next person looking for a loan. So lenders look to sell mortgages as fast as they write them, they sell to investors.

The biggest problem with mortgages from an investor’s perspective is the risk, 30 years is a long time. You might have a great job now, but what are the odds of you running into financial difficulty over the next 30 years? Well, for the “average” American, an investor would demand a very high return to account for that risk.

Fannie Mae and Freddie Mac are “Government Sponsored Enterprises” or GSEs. They were created to solve both of these problems. You see, Fannie and Freddie buy unlimited mortgages from mortgage originators as long as the mortgage meets certain predetermined underwriting guidelines. The originator underwrites the mortgages, provides the funds to the borrower, and then promptly sells them to Fannie or Freddie.

The agencies then put a guarantee on it and bundle mortgages into “mortgage-backed securities” or MBS, which they sell to investors. This guarantee promises investors that it will buy the mortgage back at par value if the borrower doesn’t pay the mortgage. By removing the credit risk, investors are much more willing to buy and to buy at lower yields.

The result is agency MBS trades with a very strong correlation to U.S. Treasuries. With no credit risk, investors don’t have to worry about mortgage defaulting. They only have to worry about interest rate risk – the risk that they are tying up capital at prices that might be less attractive in the future.

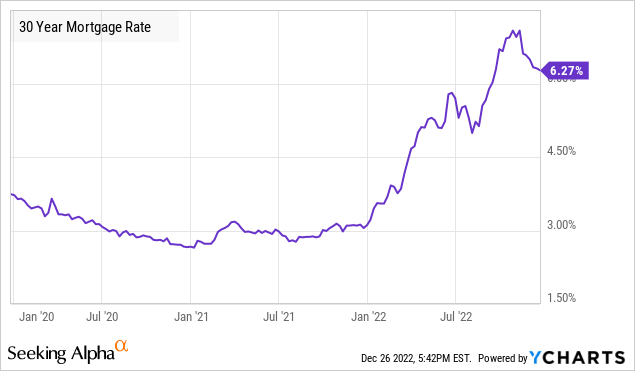

AGNC Investment Corp (AGNC) invests in these MBS and in 2022, has felt the brunt of interest rate risk. Mortgage rates skyrocketed in 2022. For years, mortgages have had 3%-4% yields, but in 2022, this skyrocketed to over 7%.

In the past couple of months, mortgage rates have fallen. Yet is still twice as high as they have been in recent years. As a result, the value of all the 3%-4% mortgages that AGNC has bought over the years is much lower. AGNC’s “book value” collapsed to multi-decade lows, and the share price followed.

The great irony is that AGNC’s future outlook is brighter than ever. Falling MBS prices impact book value, but the mortgages are still guaranteed at par! AGNC’s cash flow has improved, and on new investments, AGNC is getting substantially higher returns than have been available over the past decade.

Think about it: AGNC is in the business of owning mortgages. If mortgages are paying twice as much as last year, is that a good thing or a bad thing for mortgage investors?

The instability of mortgage prices in 2022 has made it difficult for AGNC to back up the truck and buy. Since it uses short-term borrowings, it must hedge against interest rate risk.

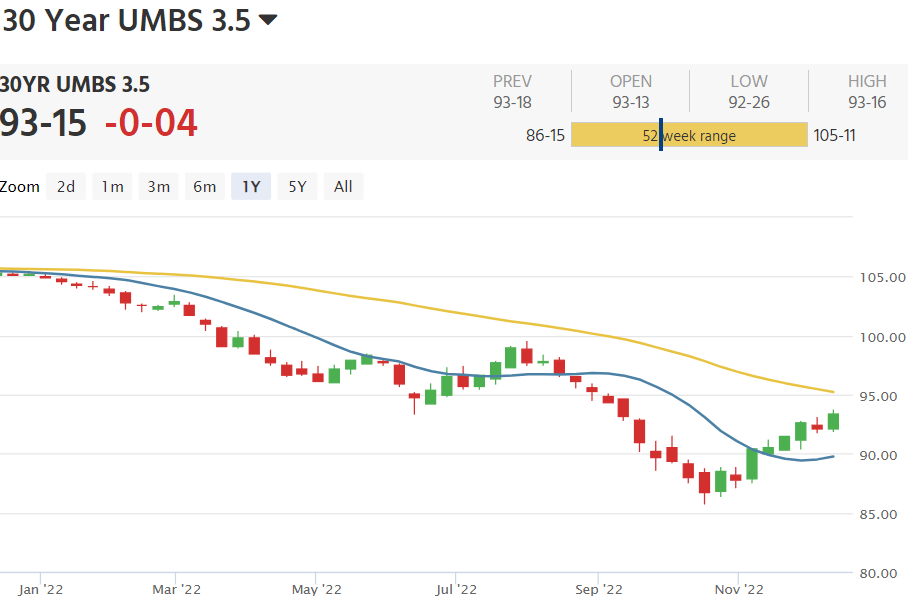

After the Fed meeting in December, AGNC has to feel really good about getting more aggressive with buying mortgages. While the equity markets have responded by selling off, the mortgage markets have remained stable. Continuing their recovery from the October bottom. Source

Mortgage News Daily

That mortgages have maintained their ground in the face of what theoretically should have been a headwind is a good sign that the bottom was in October and waving the green flag for AGNC to leverage up and buy more mortgages at attractive yields.

AGNC owns $60 billion in mortgages. It will likely own north of $100 billion in mortgages when it leverages up. Maybe, it might own yours and/or your neighbors! The outlook for future earnings is bright, and you can collect a double-digit yield with this monthly dividend.

Dreamstime

Conclusion

With EPR and AGNC, we can enjoy large monthly dividend income from two companies with exposure to the American economy’s roots. The last bill most are likely to skip paying is their mortgage, and even if they do – AGNC has the principal guaranteed back to them. EPR will benefit from the “lipstick” effect – even in hard economic ties, consumers will spend money on small ticket extras to reward themselves. A trip to a movie theater is fun and also much less expensive than a 4-day cruise.

What does this mean for you? Your income will keep pouring in month after month.

Retirement should be a time to explore opportunities, dabble in new hobbies, and build relationships with loved ones and new friends. Your finances shouldn’t be holding you back but propelling your forward by enabling you to experiment and explore.

If your portfolio feels like an anchor stopping you from reaching your potential, perhaps it’s time to reconfigure your portfolio into something that can.

That’s the beauty of income investing – it’s never too late to get an income portfolio up and running.

Be the first to comment