Gizem Gecim/iStock via Getty Images

Today I offer an update on RenaissanceRe (NYSE:RNR), which I first recommended in May of 2021. RNR is a reinsurer focused on the property sector with specialization in natural catastrophe modelling. The company is perfectly positioned to take advantage of current dynamics in the property insurance market, which was recently rocked by Hurricane Ian. I continue to recommend RNR as a high-confidence stock, especially for younger investors with a longer time horizon.

State of the Property Insurance Market

Returns for property insurers and reinsurers have been depressed over the past few years. Lots of cheap capital entered the space seeking returns in a low-yield macro environment, and a series of heavy catastrophe years caused significant losses. 2022’s Hurricane Ian may have been the last straw for many. Ian is estimated to represent the largest loss event for the insurance industry ever, with early estimates coming in at a minimum of $75 billion in total loss.

Unsophisticated capital is now draining out of the reinsurance market. With risk-free rates rising (and providing more attractive alternatives) and losses mounting, available reinsurance capital contracted in the back half of 2022. This dynamic set up a widely-reported “hard market” entering January 2023 renewals, where power has shifted to the remaining players in the reinsurance markets:

Berenberg’s analyst team have been highlighting a steady shifting of the power-balance in reinsurance over recent months, but now they believe the shift towards reinsurance and retro capital providers is becoming “significant”, with more still to come.

“In our view, it is becoming increasingly apparent that the balance of power is shifting towards property reinsurance (and retro) sellers, as opposed to buyers,” the analysts explained.

Typically, in the current hardening, to hard, reinsurance market environment, new start-ups and new insurance-linked securities (ILS) capital would be pouring into the sector.

But as we approach the end of 2022, this isn’t the case.

– Steve Evans, writing for Artemis.bm. “Power shifts to property reinsurance & retro sellers”

Industry reporters suggest that primary insurers had significant difficulties finding reinsurance coverage at the January 2023 renewals, with “no signs that all cedents will be able to secure the capacity they want by, or even soon after, January 1st.” This resulted in reinsurers gaining significant pricing power. Howden (a brokerage group) reported 37% price increases on average for global property/catastrophe reinsurance and 50% average increases in the US.

In short, it is an incredibly good time to be a well-capitalized reinsurer.

RenaissanceRe’s Position

About 18 months ago, I first wrote on RenaissanceRe. My thesis in that article was twofold: first, that climate change was a secular growth driver for property insurance, which would increase demand for capital in the sector. And second, that climate change would make accurately pricing risk harder in this sector (as old models for natural catastrophes became out of date), meaning that the edge for sophisticated players in the sector would get wider. This creates a “winner-takes-most” dynamic where the most capable underwriters would use their edge in risk modelling to capture the most attractive returns in the sector. RNR is the acknowledged market leader in natural catastrophe reinsurance, with extremely strong in-house cat modelling capabilities that put them far ahead of the vendor models many other insurers rely on, and a long track record of successfully driving book value growth. I argued that RNR was the perfect company to take advantage of these long-term trends.

I believe that the current hard market in the property sector is evidence of this long-term thesis playing out. Unsophisticated capital is leaving the sector as it failed to secure good returns, all while demand for reinsurance continues to increase, leaving RNR perfectly positioned to generate strong returns going forward.

Going into the most recent earning call, RNR was trading in the $130-150 range as investors awaited news on Hurricane Ian. With book value temporarily depressed by rising interest rates, the fear was that significant exposure would force RNR to lock in otherwise temporary losses on its bond portfolio and leave the company undercapitalized going into the Jan 1 renewals. The November earnings call decisively addressed these concerns.

This year, a Cat 4 hurricane hit Florida and 10-year U.S. treasuries were down 18% year-to-date, which is the worst performance in a century. Our investors rightly want to understand if we have the capital to take advantage of profitable opportunities in 2023. The answer is yes. Our group and rated balance sheets are strong and give us a wide range of flexibility to access attractive risks.

There are three things I would like to highlight. First, as Kevin pointed out, through a combination of holdings company capital and committed partner capital, our rated balance sheets will bring the same level of capital to our customers next year as they did prior to and this year. Second, our reserves are strong and reflect our current view of the impact of inflation. And finally, we are in a very strong liquidity position across all our balance sheets. In this very attractive market, we believe that deploying capital into underwriting is the best way to maximize long-term value creation for our shareholders and are not planning repurchases in the fourth quarter.

– Bob Qutub, RNR CFO, 2022 Q3 Earnings Call

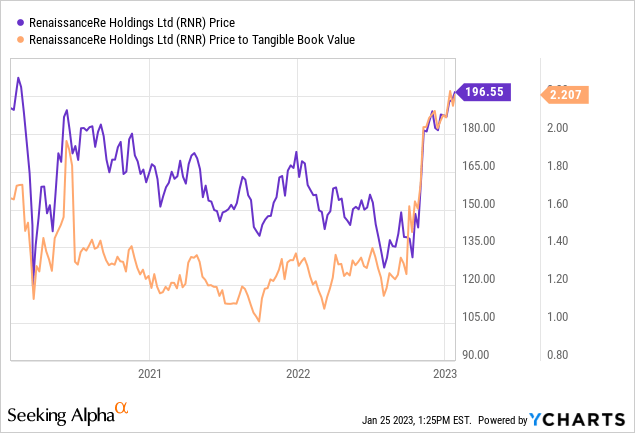

The price rapidly shot up after the earnings call and has been trading in the $180-195 range as investors now anticipate that the company will be able to take advantage of the ongoing hard market.

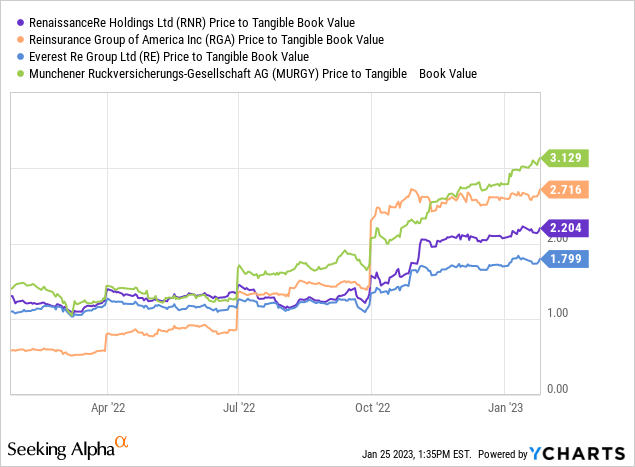

Investors may fear that the stock, currently trading at historically high price-to-tangible-book-value (P/TBV) ratios (above 2x), is pricing in too much success. However, the book value ratio is not out of line with current trends in the broader sector.

P/TBV ratios are currently inflated across the sector, primarily due to temporary mark-to-market losses on bond portfolios because of the rapidly shifting interest rate environment. These ratios will come down to more historically normal levels over the next few quarters as portfolios turn over, mark-to-market losses are reversed, and interest income increases. RNR does not appear to be uniquely expensive at the moment.

Conclusion

Investors will learn more about the company’s performance at the Jan 2023 renewals in next week’s Q4 earnings call. While the short-term opportunity in RNR is probably limited after the recent price action, I believe that RNR continues to be an excellent long-term opportunity to take advantage of the secular trends driven by climate change, and continue to recommend the company as a core holding. I continue to believe the company is particularly attractive for younger investors with a longer-term time horizon, as the positive exposure to rising interest rates provides diversification for younger investors who tend to have their portfolios tilted towards growth.

Be the first to comment