Brandon Bell/Getty Images News

Introduction

Reckitt Benckiser (OTCPK:RBGPF) (OTCPK:RBGLY) performed pretty well during the COVID pandemic as its Lysol and Dettol disinfectant brands were highly sought after. But Reckitt is more than just those two products and about 70% of its revenue comes from brands that are unrelated to COVID-19 and should continue to see their revenue increase.

Reckitt investor Relations

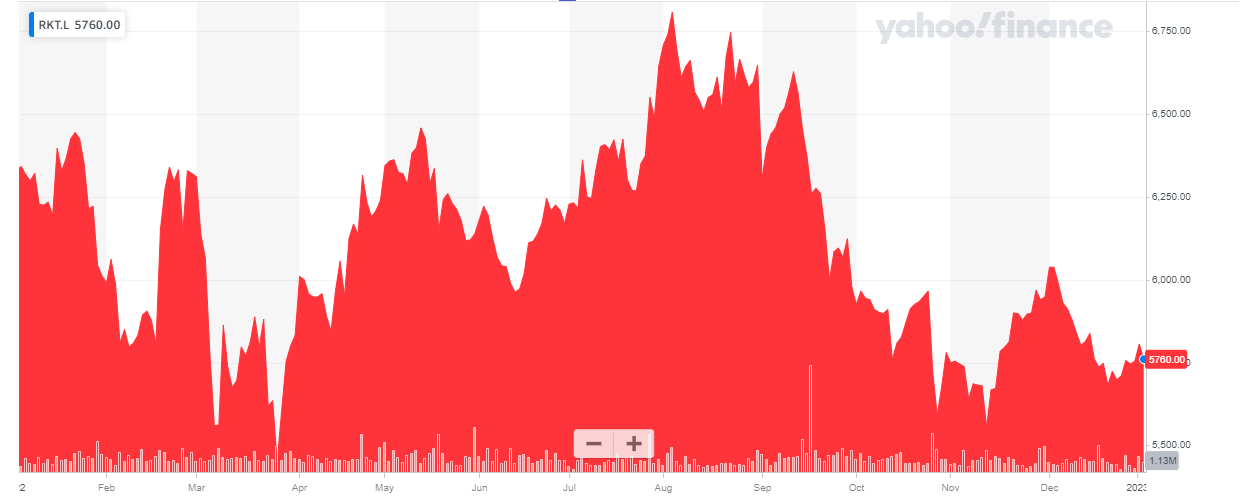

Reckitt’s primary listing is in London where the company is trading with RKT as its ticker symbol. Considering the average daily volume in London is approximately 1.35 million shares per day (for a monetary value of in excess of 75M GBP which translates into in excess of $90M), I would strongly recommend using the company’s most liquid listing to trade in its shares. I will use the GBP as base currency throughout this article.

Yahoo Finance

Unfortunately the Reckitt website contains quite a few download-only links which makes it difficult to hyperlink to all exact sources, but you can find all relevant information and documentation here.

2022 should have been a year with strong cash flows

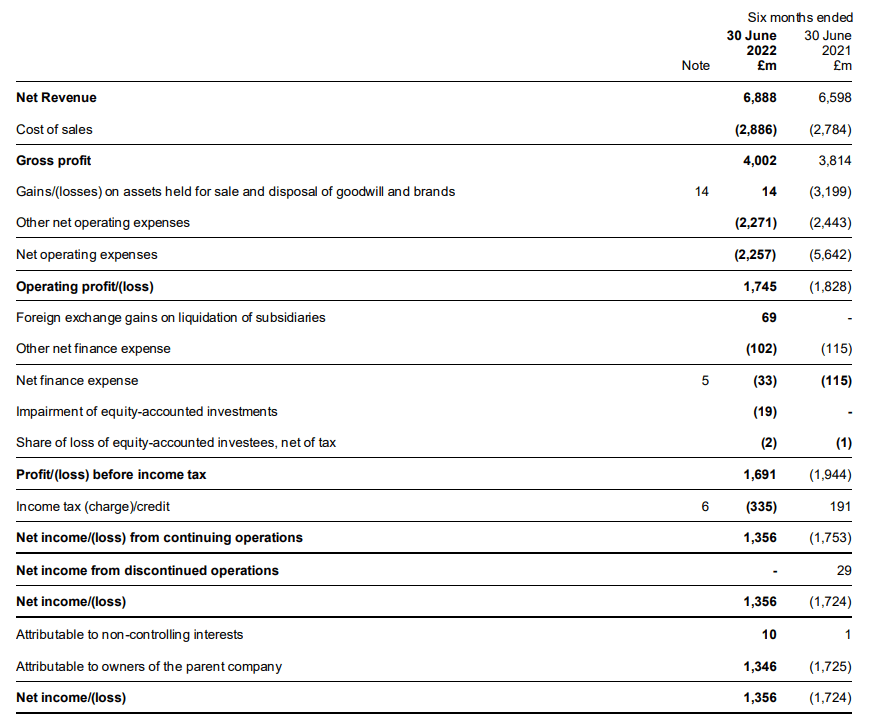

Reckitt only publishes detailed income and cash flow statements every six months so the most recent detailed financial statements to have a look are discussing Reckitt’s H1 results.

During the first semester, Reckitt generated just under 6.9B GBP in revenue, resulting in a 5% higher gross profit, which came in at 4B GBP. The total operating expenses (adjusted for the losses on the assets held for sale) came in lower and this boosted the operating profit to almost 1.75B GBP.

Reckitt investor Relations

The pre-tax income during the first half of the year was 1.69B GBP which resulted in a net income of 1.36B GBP. Of that bottom line result, about 10M GBP was attributable to non-controlling interests which means the net income attributable to the Reckitt shareholders was 1.346B GBP, representing an EPS of just over 188 pence per share. The adjusted EPS was just over 178M GBP after cancelling out some exceptional items.

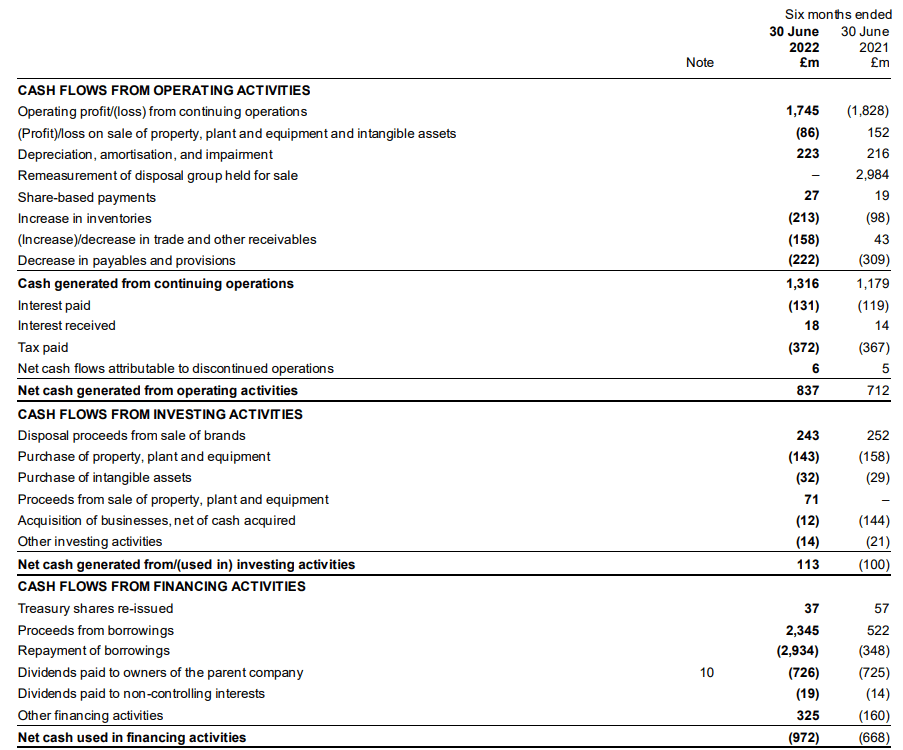

I also focus on cash flows, so Reckitt’s H1 cash flow statement was also important to have a look at. The starting point is the company’s 1.75B GBP operating income. We see the total reported operating cash flow was 837M GBP but this includes about 37M GBP in additional taxes paid over what was due based on the H1 results, and it also includes a 593M GBP investment in the working capital position. On an adjusted basis, the operating cash flow before changes in the working capital position was approximately 1.47B GBP.

Reckitt investor Relations

The total capex was 175M GBP, resulting in a net free cash flow of 1.3B GBP. Divided over the 715M shares that are currently outstanding, the net free cash flow per share was approximately 182 pence per share.

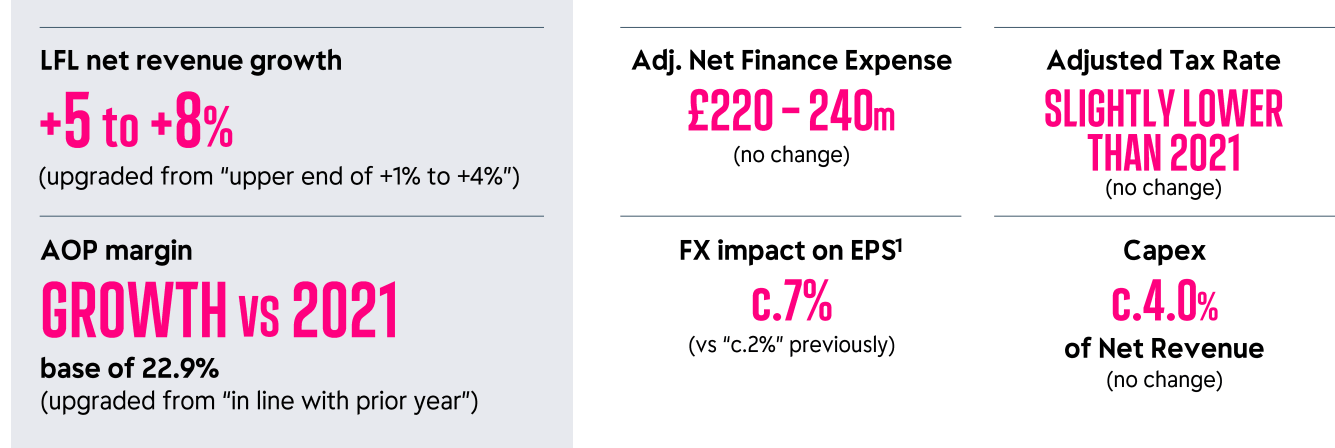

The Q3 trading update was also encouraging. Although there were no special surprises, Reckitt did narrow down the LFL revenue growth target from 5-8% to 6-8%. Additionally, on the Q3 conference call, Reckitt confirmed it has been pushing through price hikes and this should enable Reckitt to start this year on a strong note although the Reckitt management did not want to give a specific guidance for 2023 just yet.

Extrapolating the H1 results to figure out the FY 2022 performance

Reckitt usually spends more on capex in the second half of the year, and 2022 won’t be an exception. Reckitt guided for a full-year capex of approximately 4% of the net revenue which would imply a full-year capex of 500-550M GBP for this year. The net free cash flow result should be around 2.4B GBP for a FCFPS of 335 pence per share. This means Reckitt is currently trading at a free cash flow yield of just under 6%. That’s not exceptionally high but these types of investments (strong household names with excellent brand name reputation and recognition) rarely get cheap.

Reckitt investor Relations

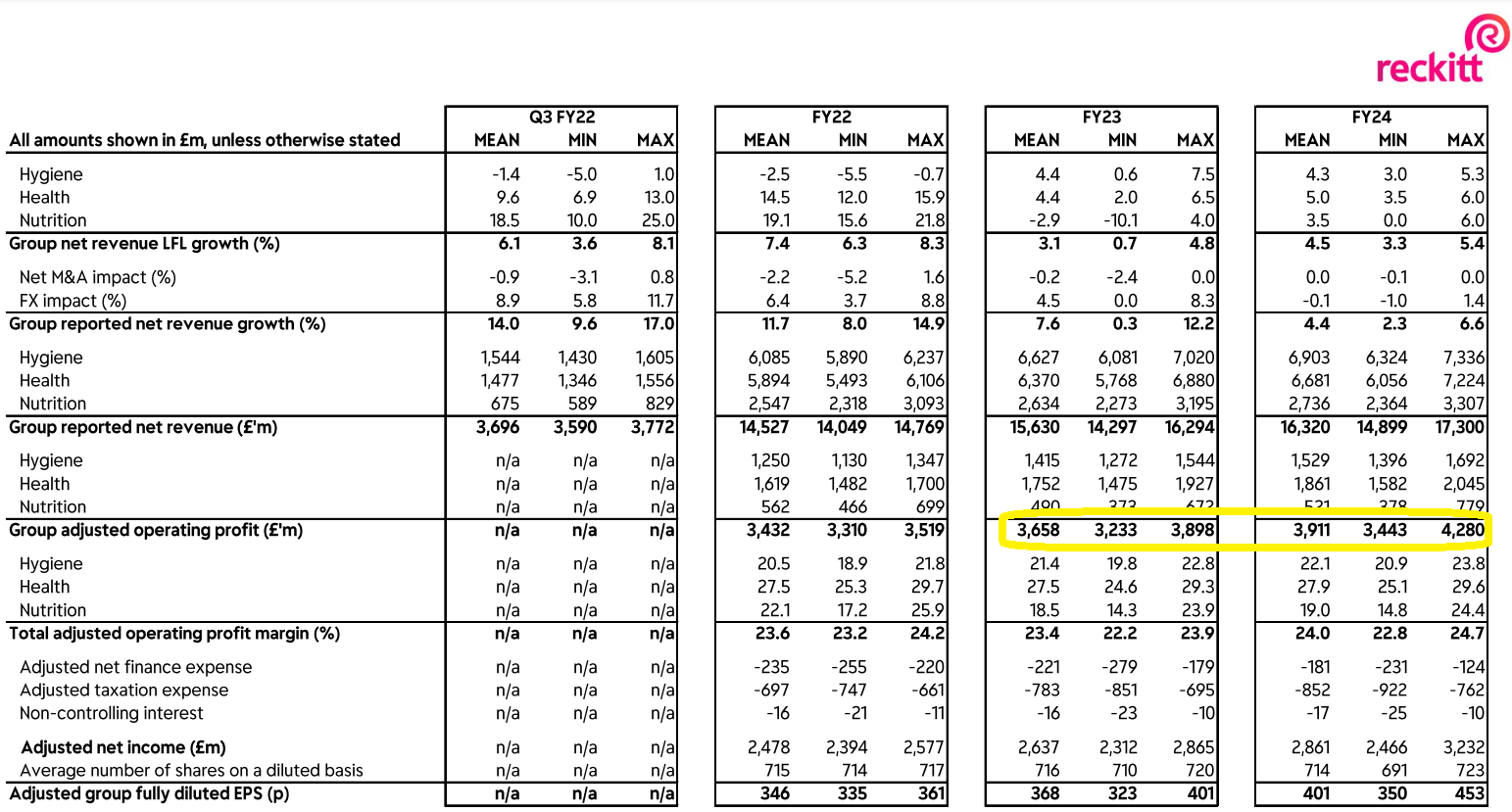

As the series of price hikes executed in 2022 will only start to contribute for an entire financial year in 2023, I expect next year’s EBITDA to come in closer to 4B GBP and the EBITDA result should further increase to 4.1-4.15B GBP in 2024, translating into a free cash flow per share of in excess of 350 pence. And I’m actually erring on the side of being cautious here. According to Reckitt, the analysts it polled expect a 3.66B operating profit and 3.9B GBP operating profit for FY 2023 and 2024, respectively.

Reckitt investor Relations

We know the annual depreciation expenses are 450-500M GBP and this means the operating profit consensus implies an EBITDA of 4.1B GBP and 4.4B GBP for the next two years. This shows my 4.15B GBP EBITDA expectation for 2024 is pretty conservative as it is just about 5% above the lowest operating profit guidance.

Investment thesis

This means Reckitt Benckiser is currently available at a relatively attractive valuation. Sure, a 6% FCF yield or an EV/EBITDA of approximately 12 is not extremely exciting, but when you buy Reckitt, you kinda know you are buying quality. I’m not expecting any sudden moves in the share price, but this could be an interesting stock to add some more ‘conservative’ plays in my portfolio.

I currently have no position in Reckitt, and in situations like this I’d write out of the money put options. Unfortunately the UK-based option contracts are based on 1,000 underlying shares which means that even if I would write a P5200 (pence) for March, I’d be on the hook for 52,000 GBP in stock. And I’m not ready to immediately establish a position of that size.

In any case, I added Reckitt Benckiser to my shortlist as I like the company’s products and its valuation is reasonable.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment