DaniloAndjus/iStock via Getty Images

This article was coproduced by Wolf Report.

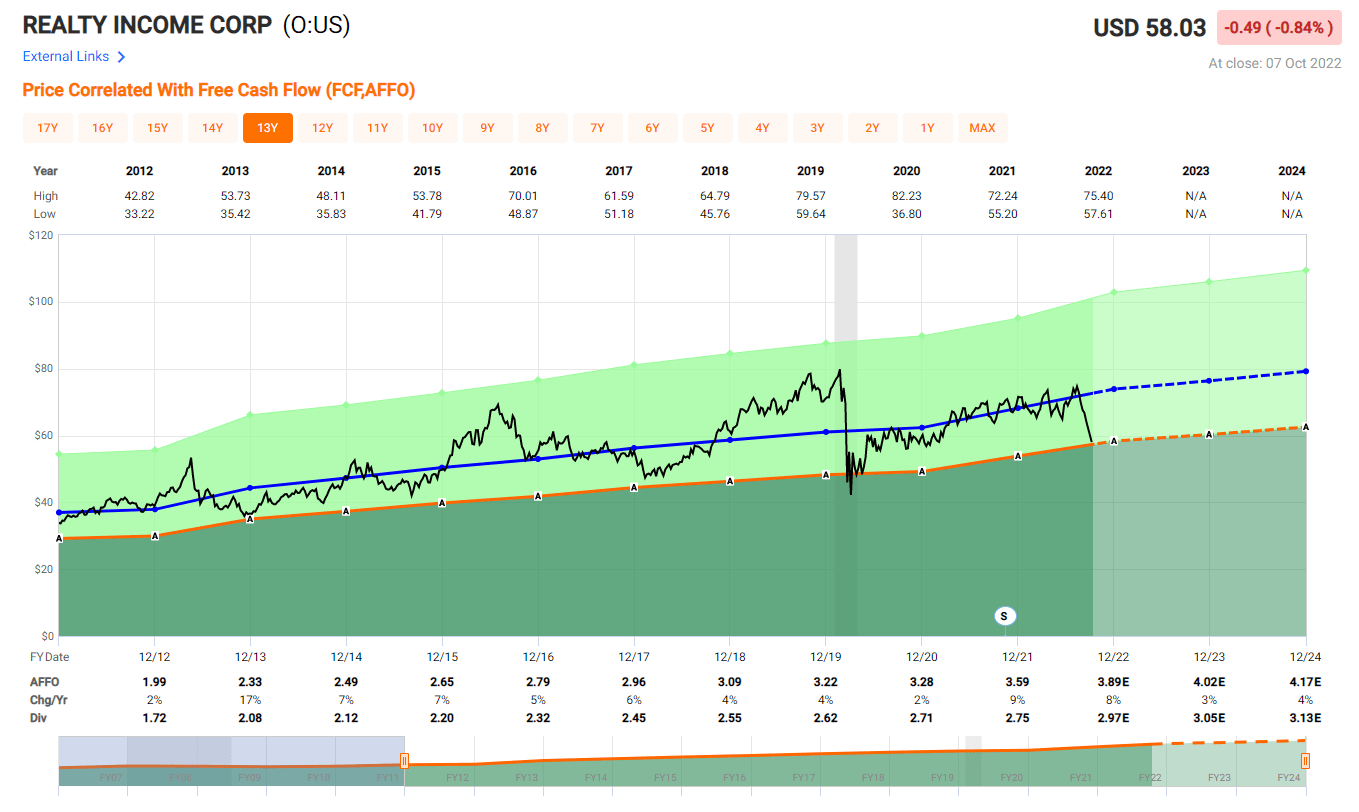

Realty Income (NYSE:O) is currently what I would consider “cheap” here:

FAST Graphs

The company is at one of the best values in years.

There are, of course, reasons for this valuation pressure.

The current environment comes with a mix of interest rate fears, inflation fears, and sector/geographic fears.

Still, we can’t lose track of what makes such a company great – and this article is a reiteration of that.

Let’s get going and see what we have here.

Revisiting Realty Income

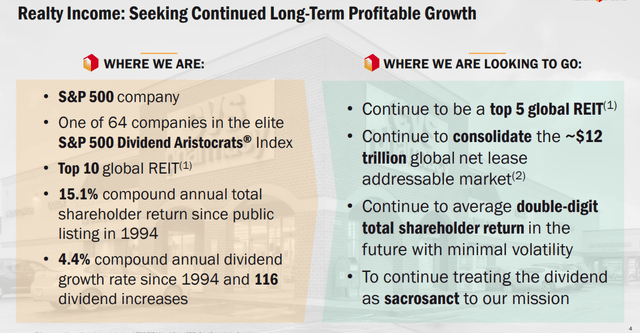

Few companies are as well-known in the REIT space as ticker symbol “O.”

The monthly dividend company is a staple for many income-producing portfolios.

Some consider the business a “Buy” even at very high multiples.

At $60B worth of enterprise value and a market cap of $40B, this is one of the largest businesses in the space. It’s heavily US-weighted, with only slight exposure to Europe, though that is growing as well.

O Investor Relations

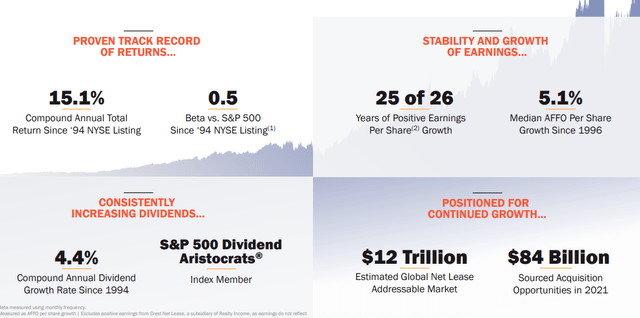

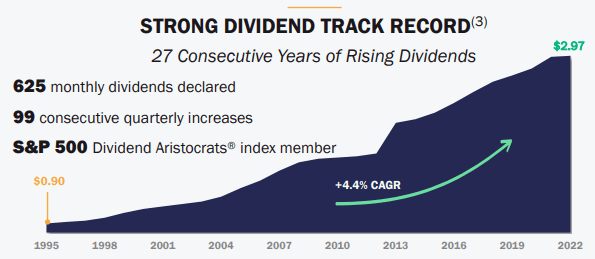

625 consecutive monthly dividends, 99 consecutive quarterly increases, and being a member of the Dividend Aristocrats makes this company’s dividend “safe” indeed.

O is the fourth-largest REIT on the planet with more than 11,000 free-standing properties, 1,125 clients and in 72 industries.

94% of its total rent is resilient to downturns and has very little correlation to e-commerce pressures.

The company has 27 years of dividend growth under its belt, but also 53 years of operating history.

O Investor Relations

It’s one of the very few REITS at an A-rating from S&P and an A3 from Moody’s.

In fact, only seven REITs have this.

The balance sheet is fortress-like for this sort of business with net debt of 5.2x to annualized Pro-forma adj. EBITDAre (a highly adjusted number, but relevant when you dig down into the filings), along with a 5.5x fixed charge coverage ratio.

Its debt is over 7.5 years to maturity, and 93% of it is fixed, with 94% unsecured.

Finding more conservative REITs is hard, and it reflects the company’s credit rating.

Interest rate raises will hurt refinancing spreads/income, but it would take years of consecutive increases for this to become a real issue for Realty Income.

These facts alone should appeal to you.

With history and fundamentals essentially “fine,” we can look at things like historical development.

The company has a strong history of growing AFFO as well as FFO, and this is of course in addition to its impressive share price development.

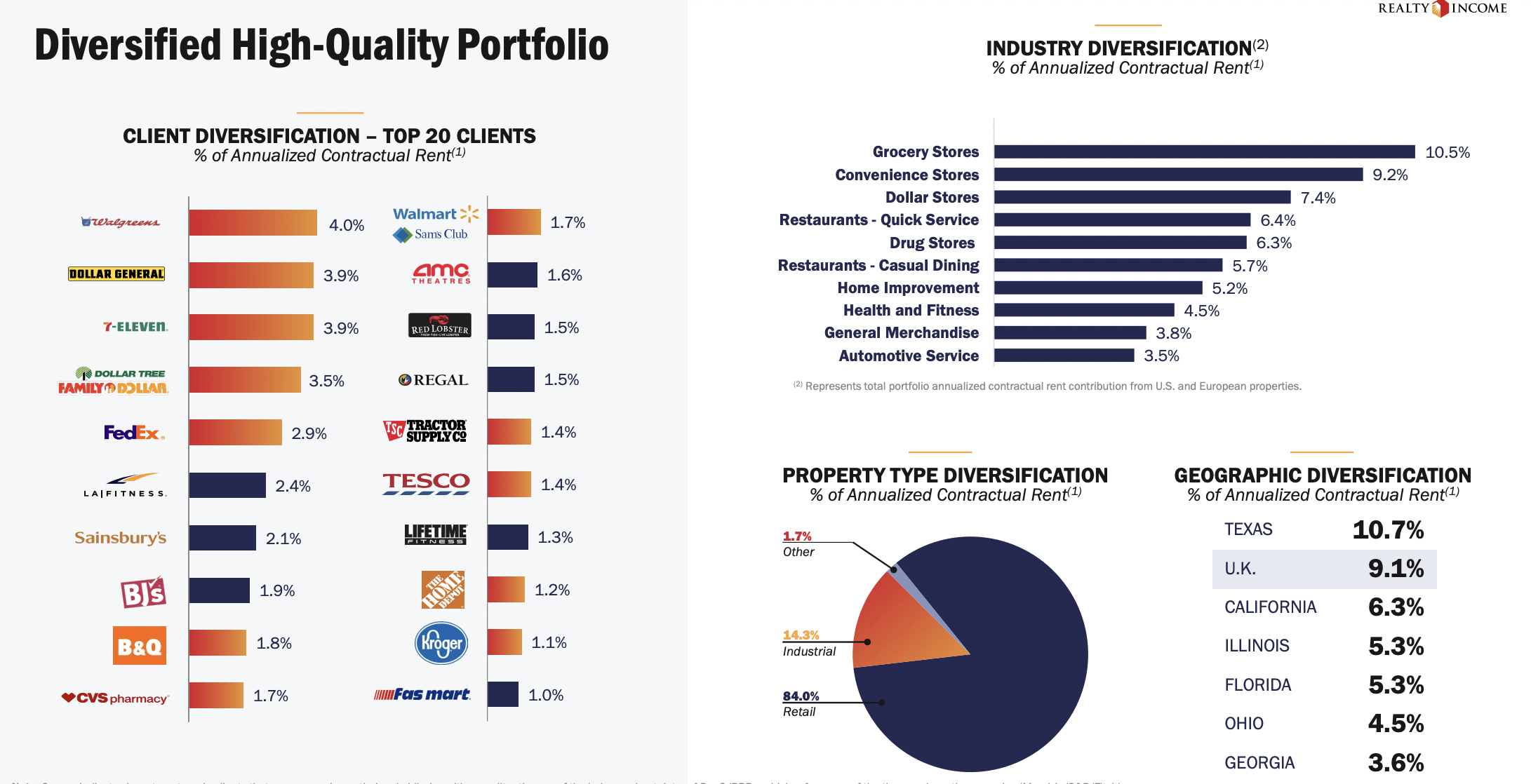

When we look at tenant quality, we find similar conservative qualities.

O Investor Relations

While I consider it technically possible for the company’s major tenants to see competition or less need for space from E-commerce growth, I would point out that such increases now come at the expense of labor cost increases, fuel increases, and inflation overall.

I question the overall appeal of diversifying too much into e-commerce compared to physical locations. And most of these top ABR tenants have businesses that do not really fit well into the e-commerce model. This adds further protection.

O remains a play on high-quality assets with high-quality tenants. 2Q22 cemented this view further.

The company’s strategy and goals continue, and we can emphasize just how sacrosanct the dividend is to the company.

The mere notion that there would be a freeze or a cut here would entail some very serious headwinds – that we currently do not see.

O Investor Relations

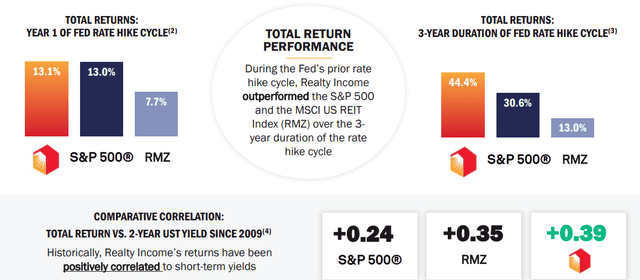

O has proven, mathematically, the superior nature of its approach.

Its TSR is superior per unit of volatility.

The merger with VEREIT has created a premier net lease REIT, and the divesting of Orion (ONL) has freed the company from some of the riskier assets from this portfolio…

And also, the dividend is much safer, because the company lowered its payout ratio (using AFFO) and its reliance on TILC (tenant improvement and leasing costs) related to its previous office exposure.

O outperforms both the one-year and three-year basis during a Fed rate hike cycle. Maybe not in terms of share price during the initial months, but in terms of TSR – which we last had in 2015.

O Investor Relations

Oh, you can argue that this cycle will be different – and that might be true.

But I believe the general direction will still be the same.

Even if there’s pressure, there’s no evidence, either in current trends, historical trends, or forecasts, that the company will see any sort of fundamental or significant impact causing it to change its thesis or expectations.

There is, simply put, too much stability in this company.

Mathematically, the company is on par with names like Johnson & Johnson (JNJ), and Southern (SO).

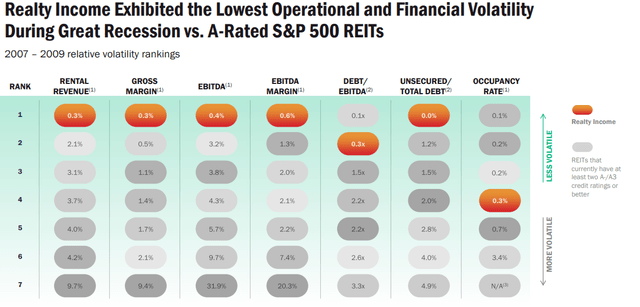

We also can look at the company’s performance during the great recession and see how volatile O was here if things really turn bad.

O Investor Relations

A REIT can of course point to all of these historical facts.

But recent results confirm these trends.

I don’t really care about share price drops, unless they’re actually based on realistic issues or risks.

So what is the “bearish” view on Realty Income?

Well, that part is pretty simple.

See now this is why “going nowhere” needs context.

Since 8/3/2016 (which was an all-time high at the time), O’s total return through 9/30/22 is 13.5% vs. the RMZ at 12.0%.

Investors should view performance on a relative basis.

What impacts real estate (positive or negative) may not necessary mirror the broader market.

This shows that relative to its industry benchmark, Realty Income has been just fine (despite using a starting point that was as high as it could’ve been).

Even most bears don’t consider O to be “bad” – they just consider some of its peers to have better yields and potentially better upsides and earnings/FFO growth than O does.

I cannot fault this because I consider this to be a valid stance.

Many of the company’s peers, including REITs like Spirit Realty (SRC), trade at more attractive multiples and higher yields.

But where O scores is safety, reliability, and predictability.

Compared even to other conservative REITs, O has the historical scores and safeties to back their valuation up, even if they trade at a high multiple even in this environment.

To me, safety, provided I get a decent yield for it, is more important than a few bps higher in yield.

I’m open to investing in REITs like SRC (I do own shares). But O is simply larger – and we all know – scale has its advantages.

O isn’t the greatest investment in terms of comparative valuation – this much is true.

But it’s a solid investment in terms of safety and returns.

Here’s where it stands following the recent decline in share price.

Realty Income’s Valuation

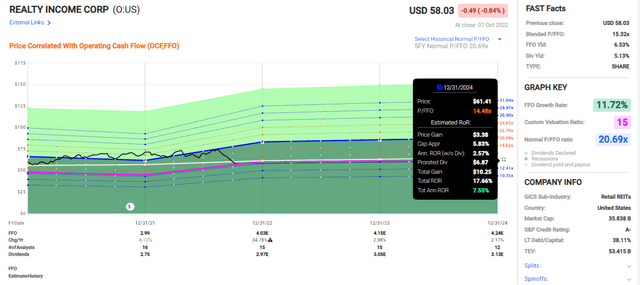

What’s interesting with O here is that it trades exactly opposed to its 2022E expected FFO growth.

2022E, bringing in new portfolio assets and merger synergies, is expected to drive FFO by nearly 35% in a single year, followed then by around 2-3% FFO growth rates.

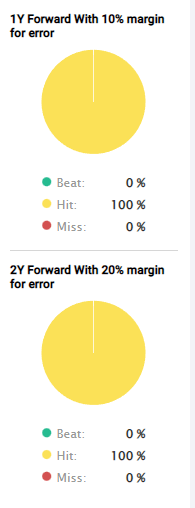

Just how accurate are these forecasts?

100%.

FAST Graphs

The analysts following the company haven’t missed the mark with an MoE for over 10 years at this point.

This means we have fairly good safety, all things considered.

Some investors say that O has “gone nowhere” now for several years.

This might be true – but it’s also because O now trades at a valuation, from which it has always recovered for the past 10+ years.

My money is on the company doing the same thing again, despite the overall macro and situation we’re going into here.

There’s very little to suggest that the company would go in a different direction.

The company trades at around 15.5x P/FFO here, which is low for the company, and high for the peer sector.

But even if it traded down to 14.5x P/FFO, you’d still make returns that can be considered in the range of S&P500 returns until 2024E.

FAST Graphs

All the while making that 5%+ return paid out on a monthly basis.

To me, if you have at least a one-year timeframe, this is the equivalent of great savings account given that there’s a “rent check” in your mail every ~30 days.

I know several of my colleagues who have an interesting investment approach.

They only buy O.

Monthly incomes, in and out.

They don’t really care about the principal/share price movements and valuations, trusting in the company’s quality, and simply collecting and in both cases, living off, the incoming checks, and reinvesting anything they don’t need.

Where?

Into O, of course.

I don’t condone or recommend this approach. It lacks diversification. But is an approach, and I can honestly say that since they both started this back in COVID-19, their returns are actually better than many “serious analysts”.

It goes to show you – quality beats most things.

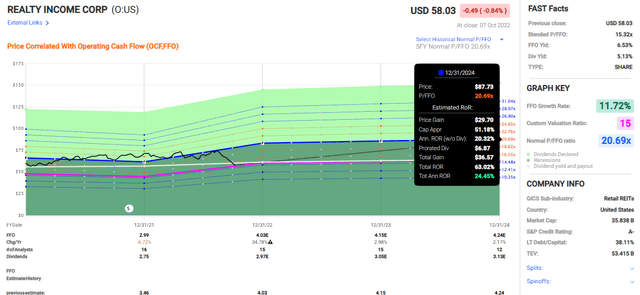

FAST Graphs

My conservative target for O is a least $70/share, and even this is a very conservative target, according to my views.

Analyst targets are far higher, and these, unlike most REITs and investments, are incredibly stable over time.

18 analysts follow O, and 12 of them consider the REIT a “Buy” or equivalent with a range of $68 low and $84 high, coming to a $76.33 average, implying an upside of at least 31%, at a valuation where the price/NAV is essentially 1x.

Wrapping up

The current price/valuation for O is a “gift” from above, as I see it.

Those investors not yet fully exposed to O in accordance with their risk weighting should consider whether an investment in O might not be beneficial to them.

I (Brad Thomas) have been a shareholder for over a dozen years and I’m continuing to increase my exposure during the share price weakness.

O is one of the biggest “no-nonsense” buys in the market. Whenever it’s cheap, I at least consider buying more.

Now, can you see why I titled this article…

Wide Moat + Wide Margin Of Safety = Sleep Like A Baby

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Be the first to comment