SteveAllenPhoto

Realty Income (NYSE:O) is one of the most popular REITs among individual investors and it is pretty simple to understand why:

- It pays a monthly dividend of nearly 5%.

- It has grown its dividend for over 20 years in a row.

- It has one of the best track records in the whole REIT sector (VNQ).

- It has an investment-grade-rated balance sheet.

- It owns net lease properties with strong tenants that are household names:

Realty Income

But is it actually a good buy today?

Before I get into this article, let me clarify that we own a position in Realty Income as part of our Retirement Portfolio at High Yield Landlord.

I believe that it is a good REIT if your goal is to generate safe monthly income and that is why we hold it in our Retirement Portfolio. We got to buy it at a >5% dividend yield and so it provides a good yield and acceptable total returns once you include a 3-4% growth rate to it.

However, if your goal is to maximize total returns, then in that case, I think that it is one of the least attractive options in the net lease REIT sector, and this is why we own much larger positions in some of its peers.

In what follows, I will give you 3 reasons why Realty Income is likely to underperform most of its net lease peers in the long run. Towards the end, we also present an alternative to Realty Income that’s likely to generate far greater total returns over time.

Reason #1: Low Internal Growth Prospects

Internal growth in the net lease sector is mainly the function of two things:

- The rent hikes in your leases.

- The cash flow that you retain to buy more properties.

And on both fronts, Realty Income is inferior to most of its peers.

The rent hikes in its leases average only 0.9%. Its rent hikes are so low because Realty Income focuses on net lease properties that are leased to higher-quality tenants like Walmart (WMT), Starbucks (SBUX), and McDonald’s (MCD). These are great tenants to have, but they also hold a lot more bargaining power when signing leases since every landlord would love to have them as a tenant, and as a result, they are able to negotiate smaller annual rent hikes.

Realty Income

Moreover, Realty Income retains relatively little cash flow to reinvest in growth. Its payout ratio is around 75%, leaving just 25% to buy more properties. That’s not bad. The dividend is certainly safe here. But some of its peers retain more income to reinvest in growth and so naturally, they will have faster internal growth prospects.

Reason #2: Low External Growth Prospects

Realty Income has historically compensated for its low internal growth rate by growing externally.

External growth is when you raise additional capital through an equity issuance to buy additional properties. It leads to FFO per share growth if your cost of equity is lower than the expected returns of the new acquisitions.

For much of its history, the market has priced Realty Income at a large premium to its net asset value, and so it was able to achieve rapid external growth.

But this is also now getting a lot harder because of two reasons.

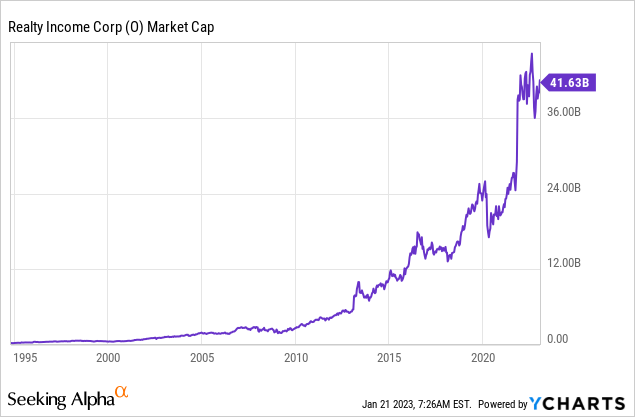

Firstly, the company is getting very big in size. Its market cap is now over $40 billion and so it has to buy a huge amount of new properties to keep the ball rolling.

The large size makes things a lot harder because net lease properties are relatively low ticket investments and there are only so many for sale at any given time. The impact of every new investment is now a lot smaller on the FFO per share because it is so large.

Moreover, the spreads are also now a lot smaller. Cap rates have compressed a lot over the years for high-quality net lease properties. Lately, they have spiked up a bit, but not enough to make up for the higher cost of debt and equity.

Therefore, external growth is likely to be a lot lower going forward.

Some of its peers are much better positioned because they are smaller in size and so new acquisitions really move the needle for them. Moreover, many of them focus on niches of the net lease market that enjoy better spreads.

Reason #3: No Valuation Discount

Despite facing below-average internal and external growth prospects, Realty Income isn’t priced at a discount relative to its peers. On the contrary, it trades at a small premium in many cases:

| FFO Multiple | Dividend Yield | Est. Growth Rate | |

| Realty Income | 16.5x | 4.5% | 3-4% |

| Essential Properties Realty (EPRT) | 14.6x | 4.6% | 5-7% |

| VICI Properties (VICI) | 14.4x | 4.7% | 5-7% |

So you are not getting rewarded with a lower valuation / higher yield that would compensate for the slower growth prospects.

Therefore, Realty Income is very likely to underperform its peers going forward.

Very simple math here would tell you that Realty Income is likely to deliver around ~8% annual total returns going forward, whereas its peers are likely to deliver closer to 10-12% annual total returns.

How can they achieve so much higher returns?

Let’s take a look at Essential Properties Realty Trust (EPRT) so that you get an example.

A Better Alternative for Total Returns

EPRT is a smaller net lease REIT that focuses on properties that are leased to middle-market non-rated tenants. Its tenants are less sought after and this gives EPRT more bargaining power as it structures its leases.

What it lacks in the credit quality of its tenants, it more than makes up by structuring safer and more rewarding leases:

- Longer lease terms

- Master lease protection

- Access to unit-level economics

- High rent coverage of 3-4x

- Higher initial cap rate (it makes up for occasional leakage)

- Greater annual rent hikes (it makes up for occasional leakage)

And this allows EPRT to grow a lot faster.

Its annual rent hikes are about 50% higher than Realty Income at 1.5%.

It also has a lower dividend payout ratio of 65%, allowing it to invest more of its cash flow in growing the portfolio.

It is also much smaller in size with a 10x smaller market cap and its spreads on new investments are greater, so the acquisitions really move the needle, resulting in faster external growth.

So here is a recap:

| Realty Income | Essential Properties | |

| Rent escalations | 0.9% | 1.5% |

| Payout ratio | 75% | 65% |

| Market cap (size) | $40 billion | $3.4 billion |

| Investment spreads | Low | High |

And so this results in the following:

| Realty Income | Essential Properties | |

| Internal Growth | Slower | Faster |

| External Growth | Slower | Faster |

| Valuation | Higher | Lower |

| Dividend Yield | Lower | Higher |

| Expected Total Return | Lower | Higher |

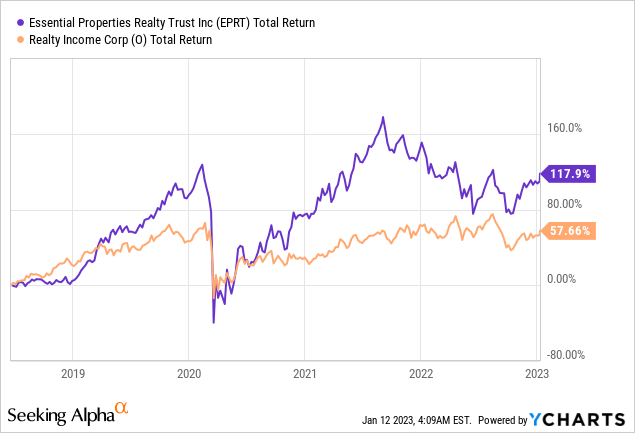

This is also backed by history.

Since going public, EPRT’s total returns have been about 2x greater than those of Realty Income, and that’s despite going through two black swan events: the pandemic and the period of high inflation / rising rates.

Typically, you would expect the large blue-chip (Realty Income) to outperform under those circumstances, but EPRT’s business model is so much more lucrative that it still pulled it ahead:

Bottom Line

This article is a good reminder that a REIT can be a good investment for one investor, but a poor one for another.

It depends entirely on your objectives.

Realty Income is a great choice for a retiree who needs safe monthly income.

However, it is a poor choice for an investor who is still in his/her accumulation phase and is trying to maximize total returns. In that case, EPRT would be a far better investment.

Because of this, we have two portfolios at High Yield Landlord.

Our Core Portfolio aims to maximize total returns and it holds EPRT.

Our Retirement Portfolio aims to maximize safe monthly income and so it holds Realty Income.

Be the first to comment