Olemedia/E+ via Getty Images

Rapid7, Inc. (NASDAQ:RPD) is a buy with strong revenue growth, high APR growth per customer and a unified cloud platform that gives it a strong competitive advantage. Businesses are undergoing a security transformation and RPD offers a full suite of services that not all of its competitors can deliver to the same standard, which gives it an edge to capture market share.

Company Overview

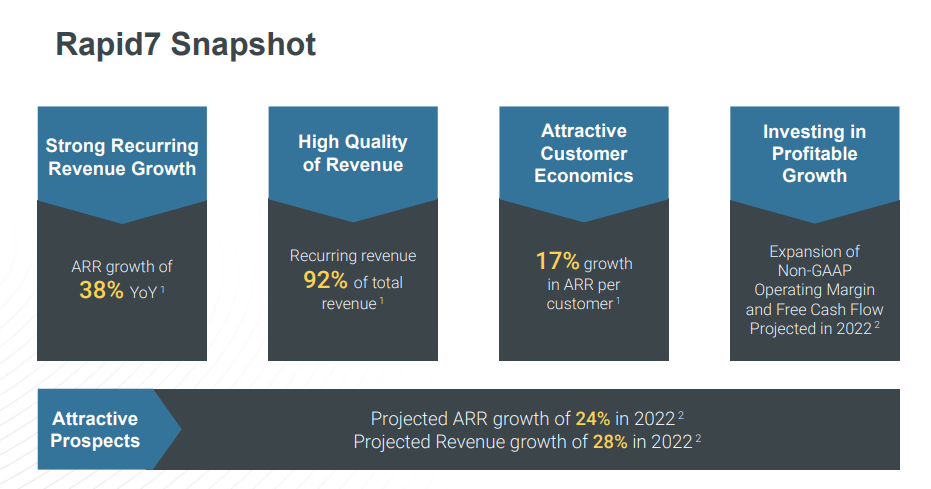

According to the investor deck released in Q4 2021, RPD is in a strong financial position in terms of revenue. The firm has an average APR growth of 38% YoY, and a quality revenue stream. In fact, 92% of its revenue is recurring from its existing book of customers, and that it’s able to increase its account penetration with 17% increase in growth in APR per lead.

Overall, RPD expects an APR growth of 24% this year and a revenue growth of 28%. 2022 is also the year that it expects to become profitable as it released a guidance of FCF to fall between $40m to $45m by the end of December.

RPD Investor Slide

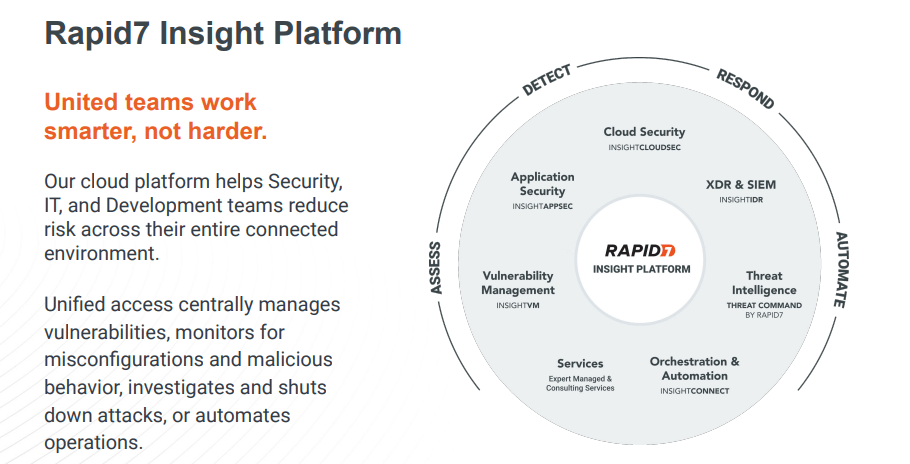

In my opinion, what makes RPD stand out from its competitors is the quality of its unified Insight cloud platform. With one application IT and security experts are able to reduce their risk of being breached across the entire organization. The tool helps with cloud as well as application security and also helps improve the organization’s threat intelligence.

Automation is also a large part of the platform as it continually monitors for misconfigurations and can be set to immediately respond to attacks and other tasks. Since the Insight platform is comprehensive, I feel that it means RPD’s customers are less tempted to pick and choose from the company’s many competitors as everything is provided in one platform.

RPD Investor Slide

Industry Analysis

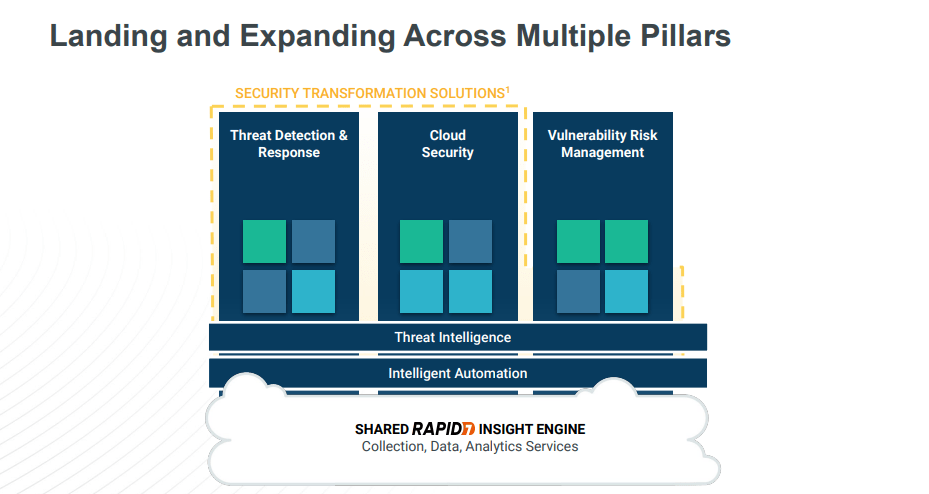

Breaking down the cybersecurity segment further, RPD has identified two pillars of which it considers to be of utmost importance: namely threat detection & response and cloud security. To me the importance of these segments makes sense as cloud computing is set to grow at a CAGR of 15% from this year to 2032 as an important market trend. Threat detection and response is also of vital importance as Norton estimates that there are 2200 cyber-attacks per day, which works out to be around one per 39 seconds. The need to immediately respond to existing as well as 0-day threats remains a priority for any business that is concerned with cybersecurity.

RPD Investor Slide

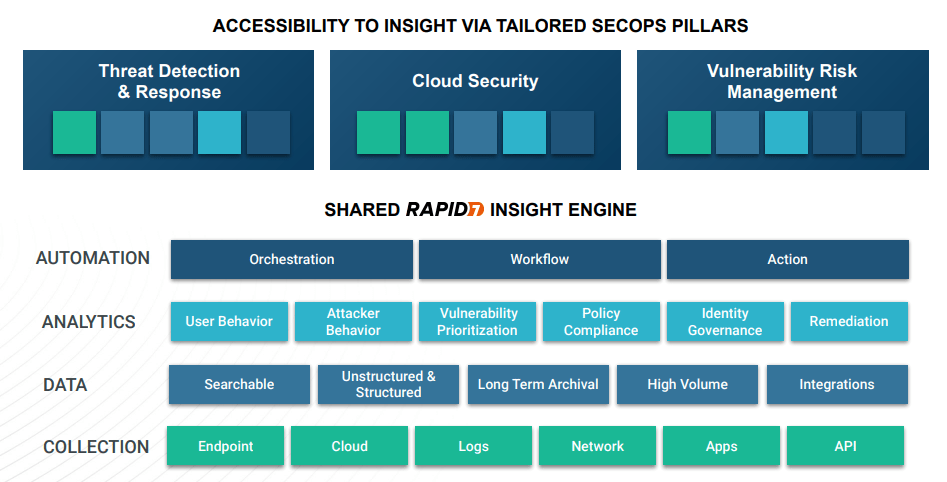

The terms of how the company’s Rapid insight engine is able to respond to the above threats are detailed below. The company integrates automation, analytics, and data to help prevent and mitigate attacks for its clients.

RPD Investor Slide

There is also a great addressable market for RPD’s revenues to grow further as more companies embrace security transformations. As cyber-attacks grow in their frequency I believe this will only be more important in the future. The company expects $500k ARR opportunity for an average customer on its books and that there is roughly $8bn worth of market share that it considers as an under-penetrated opportunity.

RPD Investor Slide

Financials

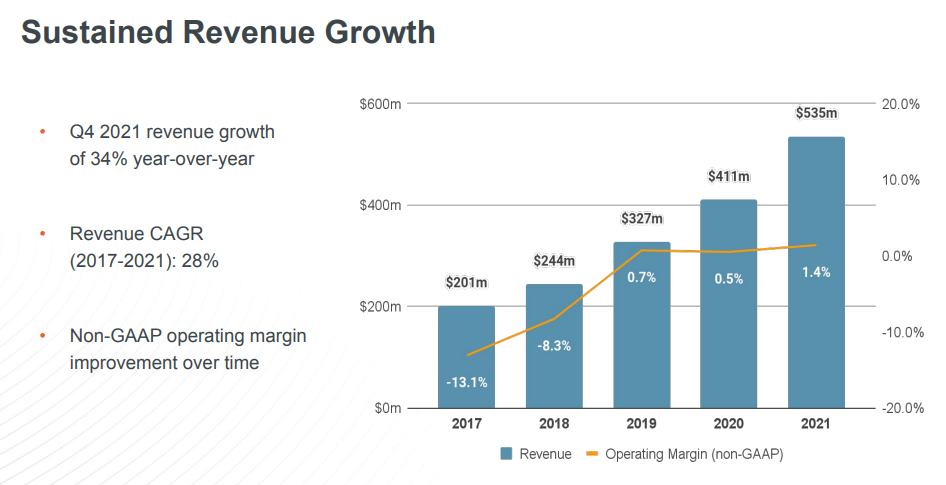

RPD managed a 34% YoY growth with a CAGR of 28% from 2017 to 2021. One downside is that non-GAAP operating margin has remained stagnant from 2019 to 2021.

RPD Investor Slide

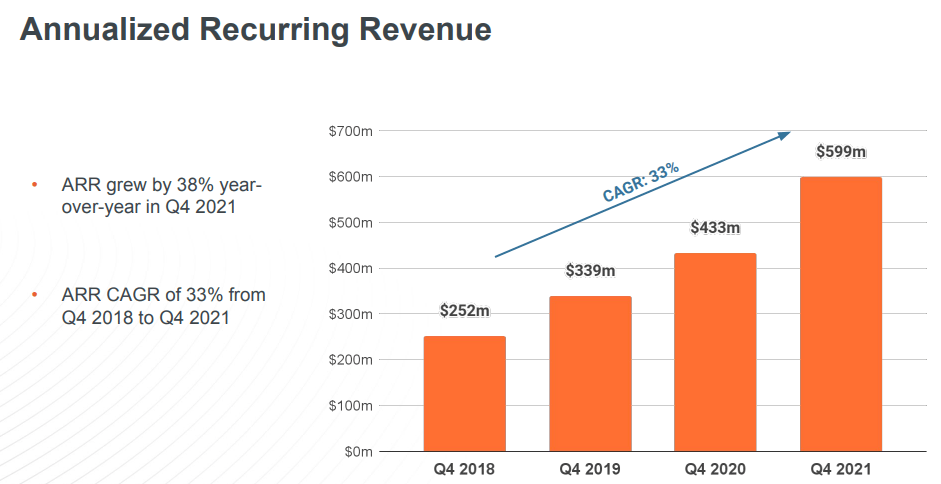

A big plus for the company is the strength and growth of its annualized recurring revenue, which grew at a CAGR of 33% from Q4 2018 to Q4 2021. To me this shows that its customers are able to extract the full value from the company’s products and that its churn is likely to be low.

RPD Investor Slide

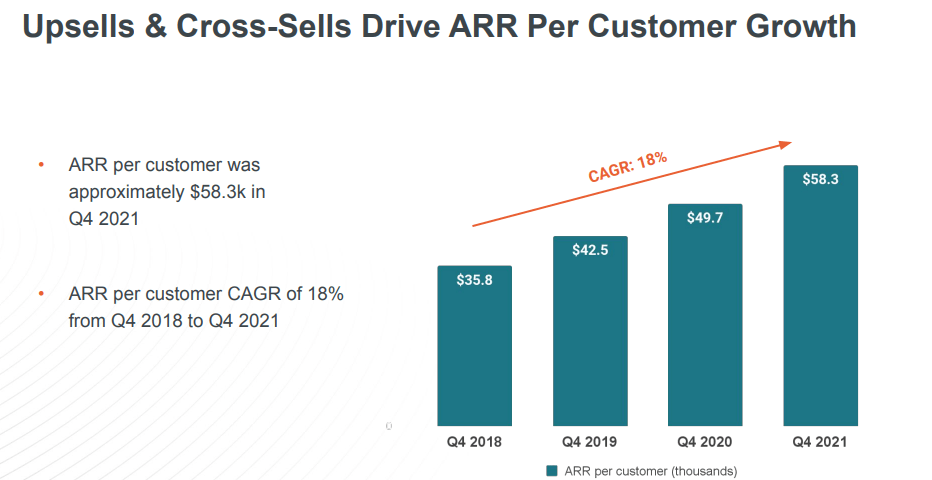

The company also stated that the majority of its revenue comes from up-sells and cross-sells across its product line. To me, a heavier investment into the company by its clients means that they are more closely integrated and therefore more loyal and less likely to change to a competitor.

RPD Investor Slide

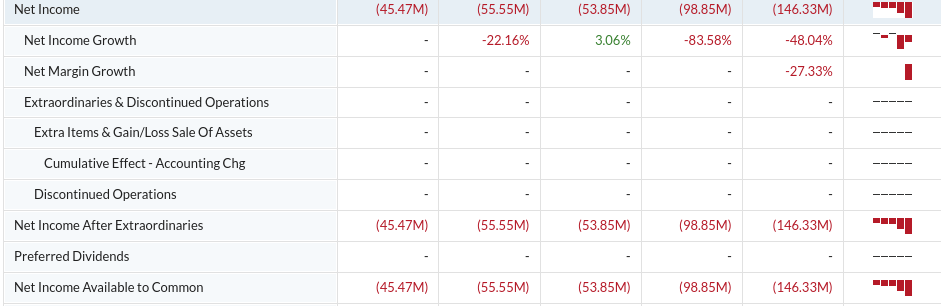

One downside of the company is that like many companies in the security industry, it has a negative net income. The company’s losses have swelled from 55.5M per year in 2018 to 146.33M in 2021.

MarketWatch

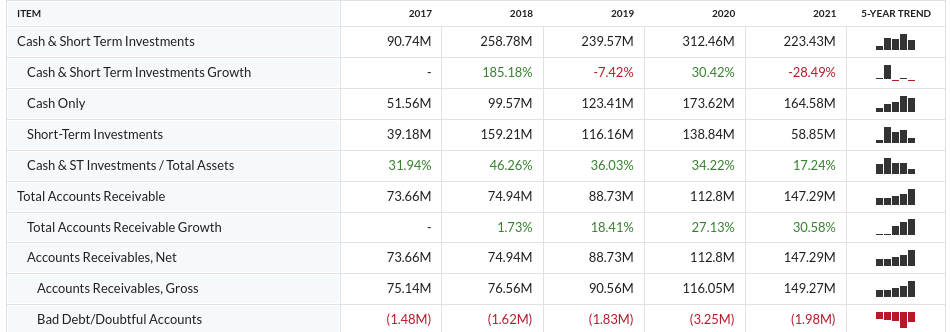

Due to the company never actually turning a profit, its cash and short-term investment accounts have remained low. RPD has a cash ratio of 0.48, meaning that it has less cash and short-term investments than its current liabilities. The company has a current ratio of 1.29, which also indicates weakness in its balance sheet, but not at dangerous levels.

MarketWatch

The company has also added to its long-term debt, with a huge swell being added to its balance sheet in 2021.

MarketWatch

Competitive Analysis

One area where I’m most bullish on for this stock is its Insight platform and how it’s able to be seen as the leader in cybersecurity for global businesses.

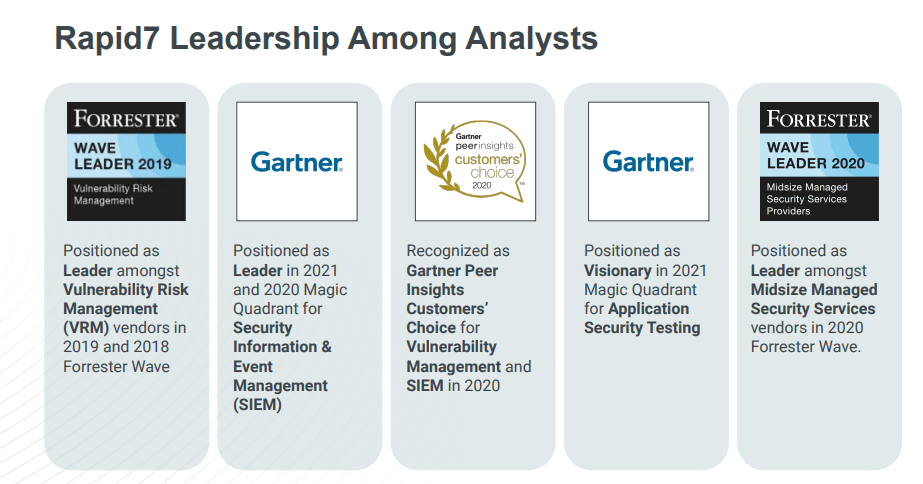

The company has been dubbed as a leader by several industry analysts. It was awarded the Leader title by Forrester for vulnerability and risk management as well as being a Visionary by Gartner for application and security testing, among other accolades.

RPD Investor Slide

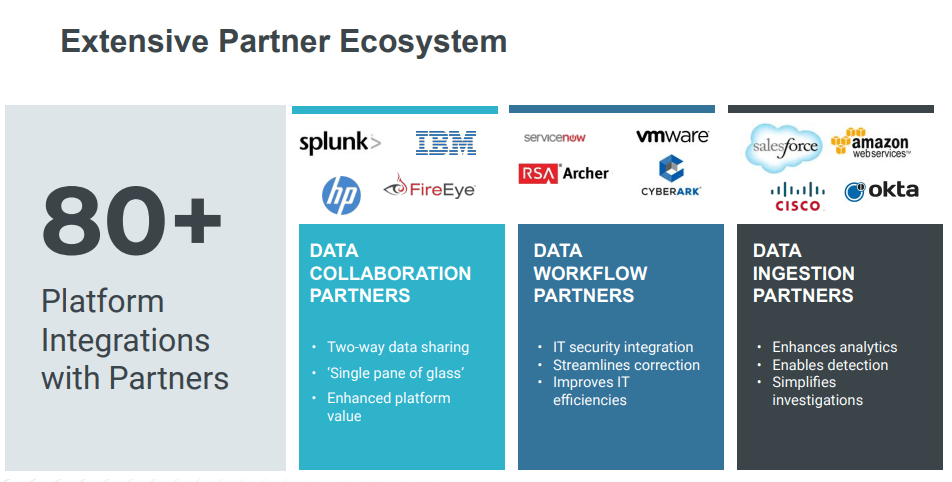

The extensive size of the company’s partner ecosystem also gives it an edge over its many competitors.

RPD Investor Slide

Valuation

For this comps model, I’ve chosen Tenable Holdings Inc. (TENB), CyberArk Software (CYBR), Qualys (QLYS), Varonis Systems (VRNS), and Mandiant Inc. (MNDT).

Firstly, RPD has the best ratings across these selection of companies, with Quant, SA Authors and Wall St analysts agreeing that it is a buy. This is the only company in the last with all 3 data sources in consensus to buy the stock.

Seeking Alpha

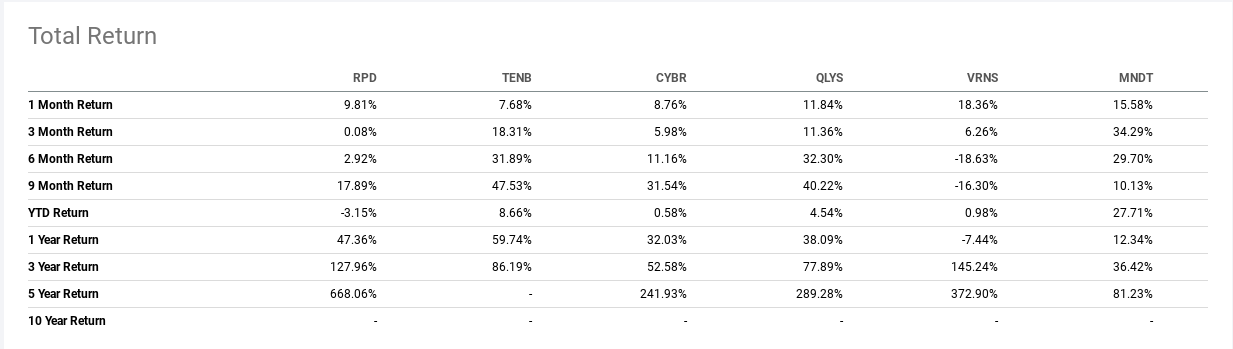

For total returns RPD also has performed strongly. It had the second highest 3-year return, and the highest 5-year return by almost double its trailing second place competitor. Its one-year returns are close to TENB at 47.36% and 59.74% respectively.

Seeking Alpha

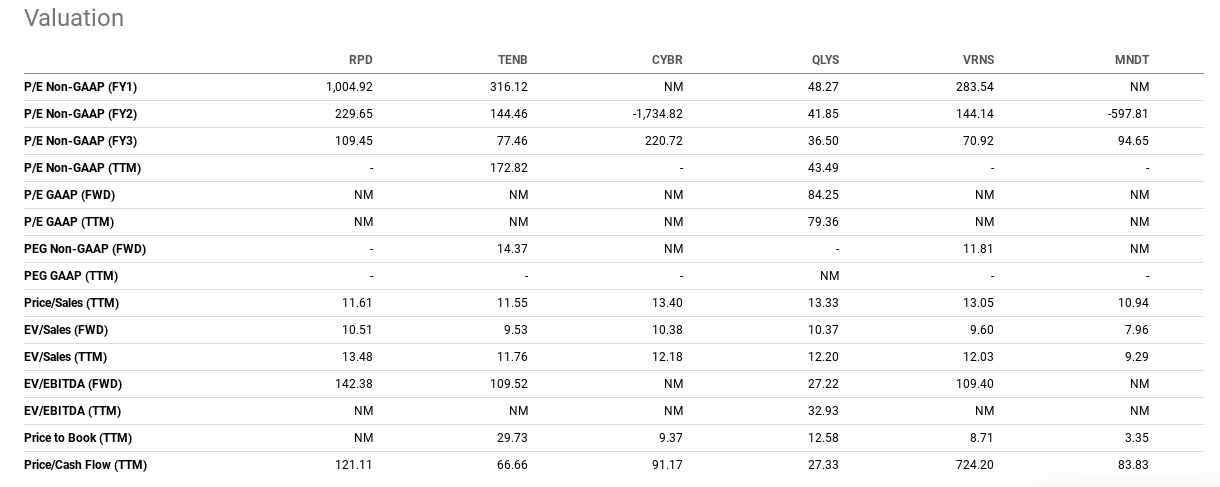

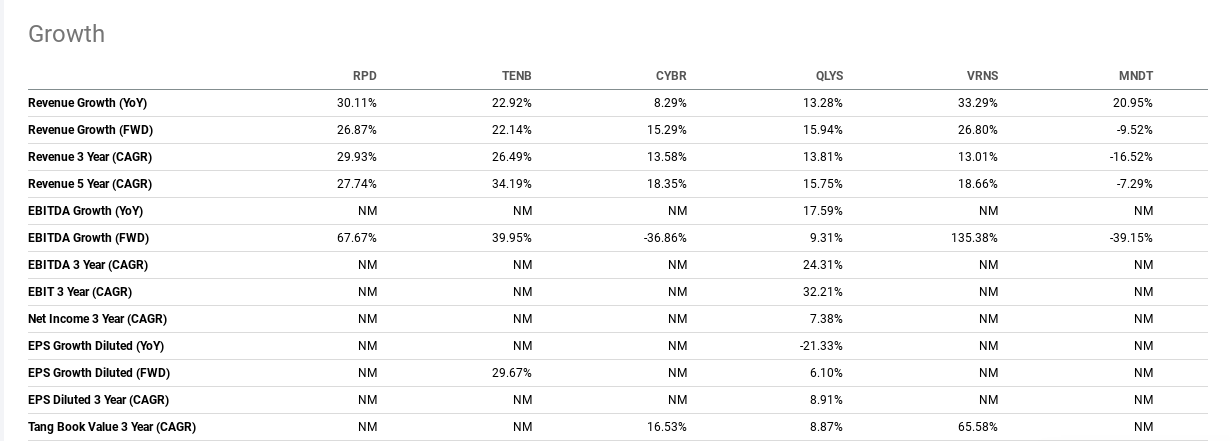

When compared to its competitors RPD has a similar ratio for its Price/Sales ttm at 11.61, while its fwd EV/EBITDA considerably higher. When looking at its Price/Cashflow ttm it’s also considerably higher than its peers, although not as much as VRNS which is the obvious outlier.

Seeking Alpha

RPD has the highest forward revenue growth out of its peers at 26.87% and a forward EBITDA growth of 67.67%, which is impressive as it’s the second highest in the group and many of these companies are expected to be in negative territory.

Seeking Alpha

Risks

Like many cybersecurity companies, RPD is yet to record a profit and has widening losses. According to guidance posted in 2021 this year the company expects to generate free cash flow but I still expect this to be highly speculative. If the company does not prove its ability to generate positive cash flow soon it will have limited runway to do so in the future due its cash and current ratios being below average.

Another risk that the company presents is the high amount of competition in the marketplace with a relatively low amount of differentiation. The company does have a growing book of loyal customers that it’s able to successfully upsell, but changes in the security transformation supercycle may lead to changes that the company is not easily able to incorporate into its integrated software, and could cause a number of customers to churn.

Conclusion

RPD has a great competitive advantage with its integrated software suite, surging revenues and has been considered by many industry analysts a leader in the field of cybersecurity. The company has good prospects moving forward as cybersecurity becomes a focus of its addressable market. For these reasons I am rating RPD a buy.

Be the first to comment