JuSun

General Overview

Passive investing has perhaps radicalized money management. With its increasing popularity, ETFs have managed to carve out a niche in every nook and cranny of the capital allocation world, stealing market share from active funds and money gurus. Rock bottom management fees and auto-pilot returns adorned exchange traded funds, appealing to the masses who simply had no time to manage capital.

Fund managers were shunned (remember Neil Woodford?) – high fees, questionable returns, and absent alpha all hammered home the underlying message – marquee money managers cannot beat the machines. Arguments abound that while passive investing aptly suited plain vanilla packages, they struggled in supplying the market with anything exotic – that remained the realm of active managers driving lambos.

That is until the advent of more complex ETFs. More recently, we have seen leveraged and ultra-leveraged wrappers, exchange traded notes, and even derivative laden funds hit the markets in an all-out assault for investors’ dollars. ETFs following US lawmakers stock picks have since gone live, allowing investors to get in on some of the action. Efficient market theory, eat your heart out.

It explains perhaps the marketing of Nasdaq 100 Covered Call & Growth ETF (NASDAQ:QYLG). Why bother writing calls when you can simply buy the ETF? Who really wants to memorize John C. Hull‘s masterpiece “Futures, Options & Other Derivatives” for a license to trade WMDs when you can simply pay, go away, and come back another day?

We at ZMK remain a little skeptical. Nothing worth having comes easy, so how can an autopilot call writing ETF lead our capital to the promised land? Previous coverage provides some oversight here – now let’s revisit its underpinnings to see if anything has since changed. Neutral.

Revisiting the ETF

According to Global X documentation, QYLG is a fund providing high income potential, some upside, and monthly distributions. It takes the labor of out of trawling through options charts, understanding Delta, monitoring Theta, and hunting for Vega. It’s the all-bells-and-whistles autopilot ETF that takes securities in the NASDAQ 100 and then writes calls against them.

The fund seeks to track returns of the CBOE Nasdaq 100 Buy Write V2 index by measuring theoretical returns of a hypothetical covered call strategy applied to the underlying index.

To achieve this, it writes at-the-money call options for roughly half its holdings – for example, 5 calls written (500 shares) for 1000 shares held in the fund. Selling call options allows the fund to collect premium which explains the income generating characteristics showcased in the term sheet.

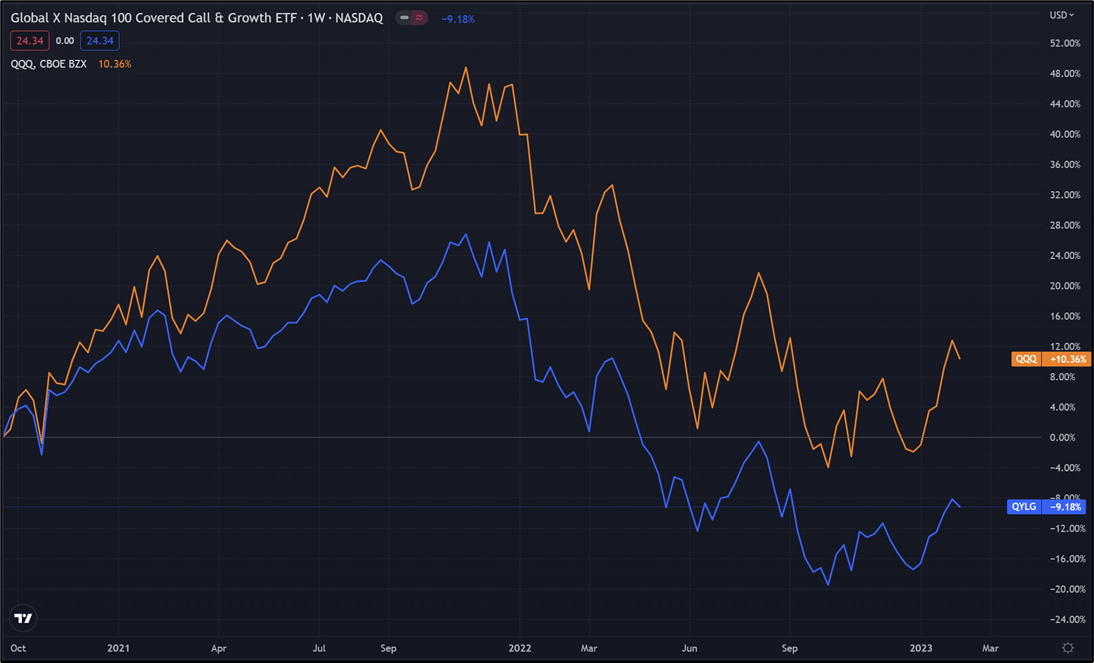

Trading View

While covered calls are naturally income generating, they have dragged on QYLG’s long-term returns when matched against QQQ, mainly because of big tech’s multi-year upside.

Covered Calls

For the unfamiliar, call writing – aka selling call options is probably the first thing you learn when you go to options school. Its covered – as opposed to naked – as you hold the underlying that can be called away from you should it go above the strike.

These strategies are mildly bearish to neutral – by selling the call, you are effectively wagering on the underlying not going above the strike price, the option expiring and you keeping the premium.

Options have several relevant characteristics described by the Greeks. And while here is not the purpose of providing a detailed thesis in derivative mythology, it is important to understand the mechanics behind the options when pulling the trigger.

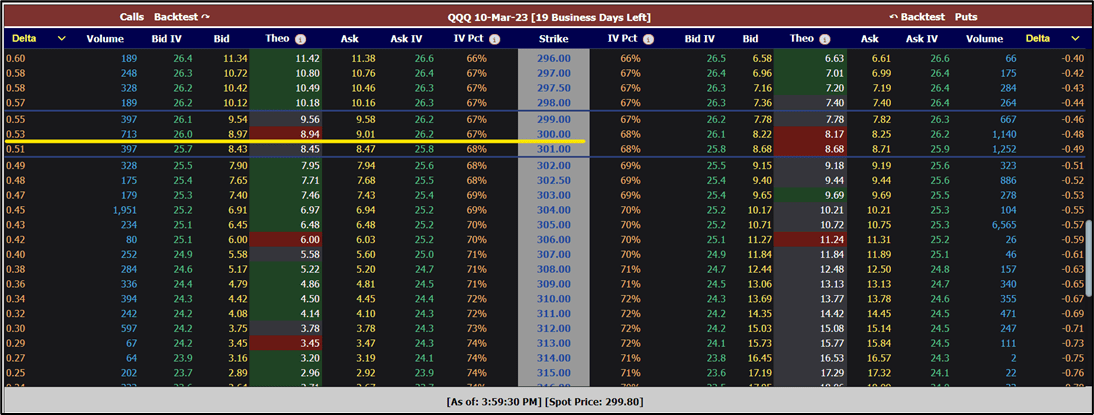

For QYLG – it sells at-the-money calls. For simplicity’s sake, we will use QQQ as a Nasdaq 100 proxy in our example. Note the fund manager is replicating this by trading options against the 100 underlying holdings, and not necessarily QQQ but this will help understanding.

Market Chameleon

The fund manager would sell 1 month out at-the-money calls highlighted in yellow.

The option chart above provides insights into what the fund manager would be doing by selling at the money call options. Note the fund term sheet stipulates the ETF sells only calls against half total underlying holdings.

So simply said, if the fund were holding 1,000 shares of QQQ (~$300K value) it would sell 5 contracts (500 Deltas) at the $300 strike. By doing this, the fund would receive a premium – in this case of roughly $9.

Market Chameleon

This theoretical example shows the 10 March 23 $300 strike being sold for $8.97. Note the implied volatility of the option.

In total, that premium would be worth $4,500 ($9 x 500) so now the fund would be holding $300K in the underlying and an additional $4,500 in premium.

If at expiry in 1 month (10 March) the underlying QQQ was below $300 per share, the fund would keep the $4,500 in premium. Oppositely, if at expiry the underlying QQQ was above $300, the fund would be obliged to sell 500 shares at $300 (~$150K cash inflow)

The call writing strategy would be beneficial if the underlying stayed at the same level during that month or moved slightly lower. As the underlying QQQ moved down in value, the short call would gain in value, offsetting some of the losses on the underlying. However, as the underlying QQQ moved up in value, the short call option would lose value, dragging on overall returns.

This explains why QQQ has outperformed QYLG over the long run – because the tech focused bull-market has seen the Nasdaq move up more often than not, the short options on QYLG have meaningfully dragged on returns. No bueno.

Market Chameleon

Historical data for the short $300 call shows that 58% of the time, the option was in the money.

Looking at statistical replication describes furthermore why the Qs generally outperform. If we looked at historical data, there are 26 similar 19 day observations over the past 4 years. During this period 58% of those observations finished in the money – in this case, we would be forced to sell the underlying.

The same data set showed there was a 70% chance of the underlying touching the strike. The average calculated value of the option from the data set was $15.52 – implying over the long run it would simply be better not selling the option because our position would have a $9 – $15.52 = -$6.52 expectancy.

Market Chameleon

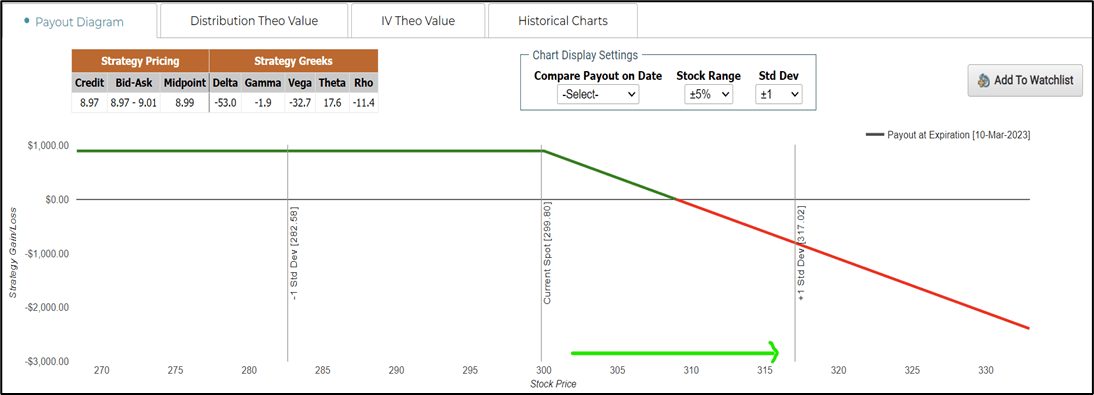

The pay-out diagram demonstrates the phenomena perfectly. As the underlying increases in price (green arrow) the short call option progressively starts to lose value, dragging on overall returns.

Risks

There are risks associated with using derivatives to manage risk. However, surprisingly Mirae Asset Management does not use OTC derivatives to sell calls, preferring to use a clearing house which helps de-risking. The fund does not use leverage, and the absence of direct counterparty means any structural counterparty risk is absent too.

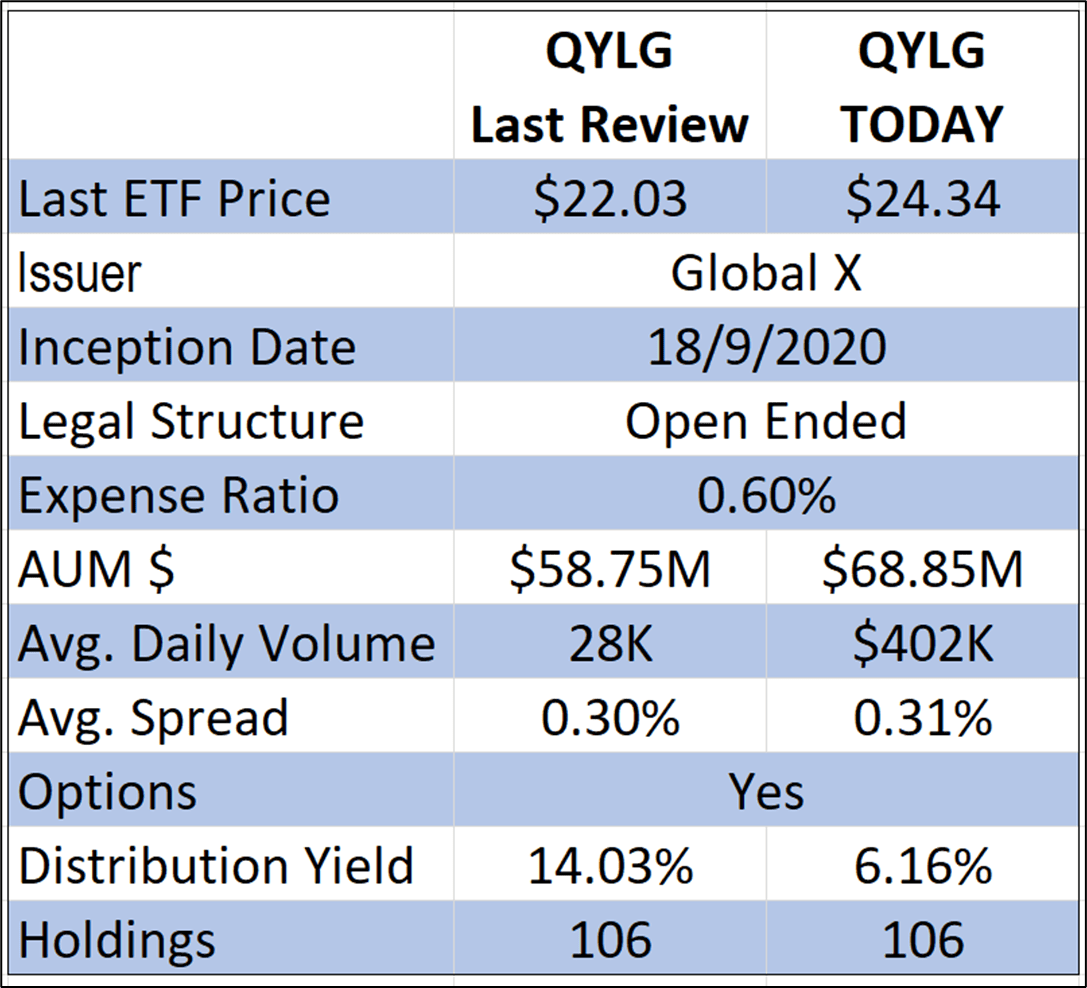

The main risks linked to the fund relate perhaps to the tech stocks underpinning the overall package and perhaps the lack of liquidity the fund has managed to build. With only $68M in assets under management, this could be a package ultimately shelved if it fails to attract investor cash in the long run.

Spreadsheet developed by ZMK

While volume has expanded, assets under management have not massively progressed.

Key Takeaways

QYLG provides investors auto-pilot options while branching out into the more exotic side of the ETF landscape. Useful in flat to mildly bearish environments, it allows investors to benefit from the income generating characteristics of call option selling.

But for those who are a little more engaged in managing capital like most of the Seeking Alpha readership, a do-it-yourself solution – saving you 60 basis points in fees – may be just as practical.

Be the first to comment