nemke

Introduction

Shares of Qurate Retail (NASDAQ:QRTEA) (NASDAQ:QRTEB) have risen 29% YTD. Despite the fact that the company’s stock is, in my personal opinion, a fallen angel, quite a lot of people still see a speculative opportunity in the stocks of the companies. I decided to make a forecast of future cash flows in order to determine the fundamental fair price of the stock, which could be targeted by long-term investors who prefer to use fundamental analysis.

Projections

The company previously released Q3 2022 results, which were lower than investors had expected. The company continues to face pressure on revenue growth and margins due to continued inflation, a supply chain crisis and declining real disposable income. In addition, the removal of COVID restrictions helps to reduce the amount of time people spend watching TV, which is negatively perceived by investors when predicting the company’s future financial results.

To predict future cash flows, I use the following assumptions:

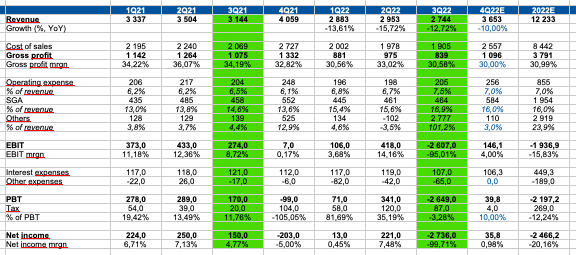

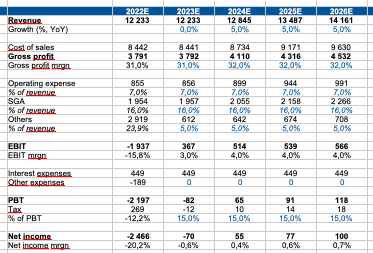

Revenue growth rate: I optimistically believe that the company will show not negative, but 0% revenue growth in 2023, then I conservatively forecast growth at the level of 5% until 2023.

Gross margin: I believe that due to ongoing macro and geopolitical uncertainty, companies will continue to face pressure on the gross margin. Thus, I predict a gross margin of 30% for Q4 2023, 31% for 2023 and an improvement to 32% by 2026.

Operating expenses: I forecast a stable level of operating expenses at 7%. A slowdown in revenue growth, in my personal opinion, will not allow the company to become significantly more efficient through the use of economies of scale.

Thus, I would like to point out that the results could potentially improve in the coming quarters, however, at the moment I do not see positive catalysts that could drive the share price higher in the near term.

Quarterly projections

Personal calculations

Yearly projections

Personal calculations

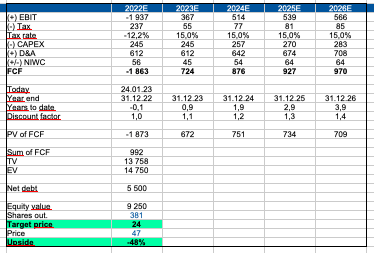

Valuation

I prefer to use the DCF method to value this company because:

1. The company has a long public history, on the basis of which I can make assumptions about the impact on financial activity of such factors as inflation growth, demand decline, etc.

2. The company operates in a stable and mature market where the use of the DCF method for valuation is most preferable

3. Management and independent agencies regularly provide forecasts of future financial and operating results, as well as the dynamics of consumer spending in the sector, which help predict the dynamics of demand for the company’s goods and services

To calculate the fair price of a stock, I use the following inputs in my model:

WACC: 8.3%

Terminal growth rate: 3%

Personal calculations

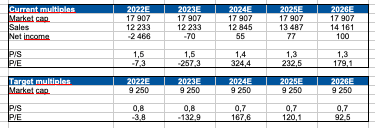

Multiples

Based on my own sales and net income forecasts, I calculated the current and target P/E and P/S multiples for the company. You can see the results of my calculations in the table below.

Personal calculations

Risks

Macro: continued growth in inflation, a decline in real disposable income and a decline in consumer confidence have a negative impact on the growth of costs in the sector and, accordingly, on the dynamics of the company’s revenue.

Margin: continued growth in inflation could have a negative impact on the company’s operating costs, which could lead to lower operating margins and a lower share price.

Competition: the growth of competition in the sector may have a negative impact on the dynamics of the company’s revenue, the level of operating profitability of the business and market share. Also, I would like to highlight the growth of competition from e-commerce players who continue to increase their own market share.

Drivers

Macro: the recovery of real incomes and the growth of consumer confidence of the population can have a positive impact on consumer spending and the dynamics of the company’s revenue.

Margin: decreasing inflation and increasing economies of scale can support the operating margin of the business by reducing the share of operating expenses.

Conclusion

Despite the fact that I like the company and the business segment where it operates, in my personal opinion, now is not the best time to go long. First, I expect inflation to continue rising and real incomes to decline, which will have a negative impact on the company’s revenue dynamics. Secondly, the lifting of COVID restrictions and the reduction in the amount of time people spend watching TV will continue to have an impact on sales. In addition, increased competition from efficient e-commerce players will also continue to affect business cash flows in the future.

Be the first to comment