Just_Super/E+ via Getty Images

AT&T (T), Verizon (VZ), T-Mobile (TMUS), Comcast (CMCSA), etc. are rolling out 5G and this has been several years in the making that is now finally ramping up. Three companies are positioned to capitalize on this multi-year secular growth trend: MasTec (MTZ), Dycom (DY) and QualTek (NASDAQ:QTEK).

All three are undervalued based on their growth potential and one is priced for bankruptcy. MasTec trades at 9.9x EV/EBITDA and Dycom trades at 11.7x EV/EBITDA and QualTek trades at 5x EV/EBITDA. It is my view that in the order of increasing risk/reward MasTec is worth $90+, Dycom is worth $115+ and QualTek is worth $10+ if you believe that they are all are currently ramping up their telco business and ride this 5G build.

The broadband construction industry has predominantly been outsourced to third-parties like MasTec, Dycom and QualTek and bringing that capacity in-house doesn’t change the economics of the build and so I expect that these three businesses are set to boom.

Investment Thesis

50 million homes will be connected with fiber broadband in the next 5-10 years. If quarterly conference call statements are to be believed, organic revenue growth should be realized from upcoming and now happening catalysts for 5G, fiber and rural infrastructure deployments. There has been a long-awaited surge in spending for fiber, wireless and 5G deployments that I suspect is now getting rolling. The market seems to be over-discounting the reality that the spending is now upon us. The risk would be that there is a deep recession that somehow negatively impacts consumer spending for internet connectedness and mobility that would result in a slower roll out of 5G. All three of these companies, MasTec, Dycom, and QualTek have record company backlogs, but if underlying business trends change meaningfully spending could be cut back or pushed back or there could be resource bottlenecks that could delay. Those risks aside, business should be booming for the foreseeable future and these three companies are undervalued today and I think they could more than double in the next couple years if they’re able to execute against their plans.

MasTec

MasTec Stock Price Chart (finviz)

MasTec is Telco/Power/O&GPipe/Renewable. MasTec also has a record company backlog. MasTec’s backlog is at $10.6B and is the first time they’ve ever exceeded $10B. MasTec trades at 23x earnings. MasTec projects 2022 EBITDA of $750M. This puts MasTec at EV/EBITDA of 9.9x. MasTec looks at 2022 as a transition year. I believe MasTec is worth $90+. Company insiders own over 20% of the float and MasTec’s largest customer is AT&T (T) which is ramping up activity in wireless/5G as planned. MasTec’s largest communications customers also include Verizon, T-Mobile and Dish — all of which are increasing their activity. MasTec sees this as part of ramping up a long cycle.

Non-Telco

MasTec has other lines of business aside from Telco. MasTec dialed back 2022 guidance because of Oil and Gas slowdowns and because a project is being pushed back a couple quarters and so this should swing back next year. MasTec views Biden’s solar executive order as beneficially as soon as next year. The supply chain is being impacted by inflation but progress is being made. There is a lot of potential in the future growth of wind energy based on new transmission routes being put into place to capture wind energy.

Dycom

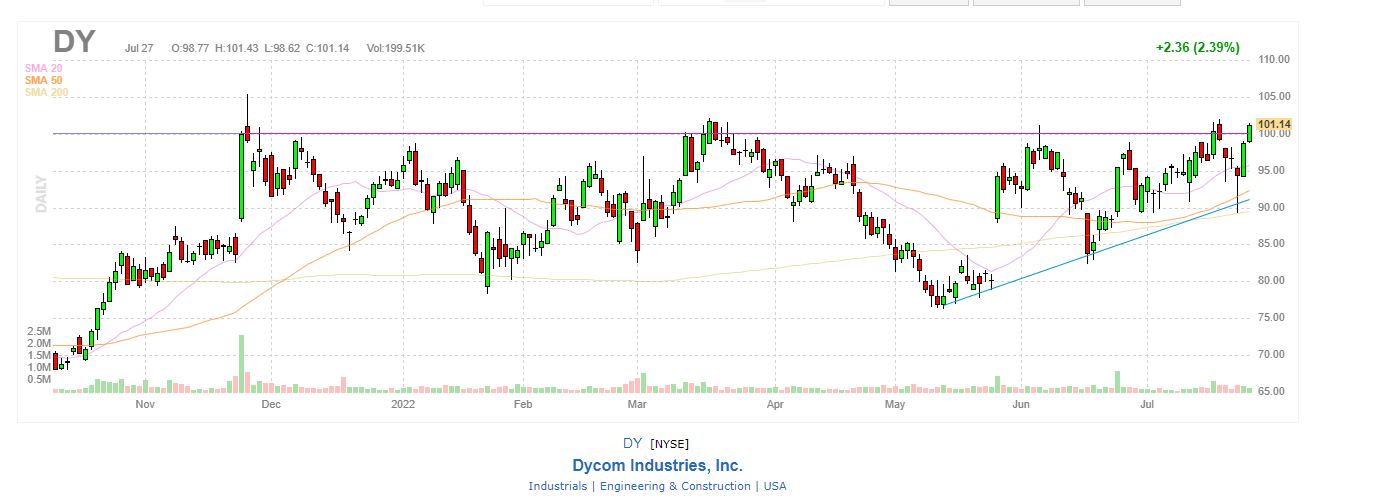

Dycom stock price chart (finviz)

Dycom is a pureplay telecom contractor. It’s top 5 customers account for 2/3 of their total revenue. Dycom is forecasting $244M of EBITDA for 2022 and has a backlog of $5.5B, of which $2.9B is expected to be completed in the next 12 months. This puts Dycom’s EV/EBITDA at around 11.7x. I think Dycom is worth $115+ and currently trades at $100. Dycom generated 21% organic revenue growth last quarter and industry tailwinds are starting to take root. AT&T is finally expanding their networks:

Dycom (DY), an installer of fiber-optic wiring, is expected to get a boost as AT&T (T) and other phone companies finally expand their fiber-optic broadband networks. In addition, new government subsidies will expand broadband networks in rural areas.

The company is repurchasing stock and is expecting to increase their margins moving forward despite inflation and a tight labor market.

Margin Expansion

Dycom expects that its margins will expand to north of 10% as the 5G rollout takes shape and the cycle gets underway. Dycom has a significant opportunity in rural utility moving forward as they undertake broadband initiatives. Dycom has been targeting longer-duration contracts where they can ensure that their labor costs are economical.

QualTek

QualTek Stock Price Chart (finviz)

The stock seems to have bottomed now. Q2 Earnings are to be announced Monday, August 8, 2022 after COB. Since the company went public in February, it has been SPAC smashed as the market has switched to risk off. Hurricane season is in full swing and QualTek’s recovery logistics line of business profits from rebuilding after hurricanes. The $2.2B 24 month backlog is worth $200M in EBITDA across the next two years by my rough napkin math. The market capitalization is $31M and there is $485M in debt and the company’s last quarter of EBITDA was a measly $4M on $148M of revenue, but business is seasonal and Q2 and Q3 are their bigger quarters. DEBT/EBITDA is at about 5x, which is maximum capacity. I expect as the company works down its debt load the market capitalization will appreciate exponentially as right now it trades like a call option on the future of a business that is priced to fail which doesn’t make sense given their record backlog. If the next two quarters exceed analyst expectations, you’re potentially looking at a $10+ stock.

Second Half Of 2022 Weighted

AT&T is their largest customer and their build plan is second half weighted:

Yeah. We do anticipate that and just want to add a nuance obviously AT&T is our largest customer, the visibility into their build plan is really second half weighted. So we may be a little bit above that.

Margins should improve possibly beyond 20% in the second half of this year. The company should be hitting its stride right now in late July / early August.

Yeah. So we’re anticipating about 10% EBITDA margin in Telecom business and as we mentioned in prepared remarks, Christian, we anticipate those margins expanding back half of Q2 into Q3 where you’re going to see a normalized run rate.

Numbers were understandably weak in Q1 but they should show strength possibly in Q2. Q3 sounds like it will be ever stronger. This likely applies to all equally to QualTek and Dycom and partially to MasTec. Business is seasonal and strongest in summer.

QualTek – Most Explosive Risk/Reward Of The Three

I don’t see any real significant financial problems with QualTek, but the valuation of the equity is so low that it appears the market is pricing bankruptcy as inevitable in the next quarter or two. My friends who have looked at this company seem to think that it is struggling financially and that it is on life support. Maybe there is something there that I am missing, but the company just went public via a SPAC at $10 which has subsequently collapsed to as low as $1. I can’t tell the difference between an investor problem and a business problem until after a few quarters of earnings are reported — we will know if business is booming or if the debt is crushing.

At a market cap of $31M, you’re getting an alleged $2.2B book of business with throughput margins of 20% that basically does a little better than breaking even in their off-season that is entering a multi-year secular growth cycle. The key ingredient to this deal from my vantage point is they extended their ABL to 2025. That seems to indicate that there aren’t the significant credit problems that the market is pricing in.

Risks To QualTek Investment Thesis

When looking at an equity security that has lost something like 90% of its valuation in the past year, it is worth noting the risks associated with the security. I recommend reviewing the 22 pages of risk factors on the company’s most recent 10-Q on pages 14-36. The biggest risk in my view is that the business underperforms in the near future and this leads to the capital structure getting swallowed by the debt where the equity is wiped out and creditors take over and make themselves whole in a Chapter 11 restructuring of sorts. The company says it has a $2.2B 24-month backlog, but if there is an epidemic like COVID-19, things could get pushed back and delayed and this could negatively impact business long enough to force a restructuring. With regards to concentration risk, the business relies heavily on a few customers for its revenue and it could lose business from these customers if these customers choose to inhouse their 5G build out or go with a different vendor. If QualTek loses AT&T, it would probably have to file bankruptcy, for example. With regards to geographic diversification, I don’t think that there is real risk there as QualTek is pretty spread out across America:

QualTek Geographic presence (10-Q SEC Filing 2022 Q1)

Another risk is that major customers could pull back on their capex spending if the economy goes into a recession instead of increasing it along with projections and expectations:

2020-2022E Capex Spend by Major Customer (2022 Q1 QualTek 10-Q)

So there are a lot of risks with investing in QualTek, but I guess my overall view is that the prevailing price seems to suggest that the business is destitute and hopeless, but when I look at what’s actually happening, things look good to great and that difference between market expectations and reality is something I think investors might want to aim to capitalize on should they agree.

5G Rollout Spending Exceeded Guidance In Q2

AT&T has pulled forward some of its 5G spend which has caused its stock to come down after it announced Q2 results because they overspent via capex guidance. The same applies to Verizon. This bodes well for anyone looking for a stronger Q2 top line from Dycom, QualTek or MasTec. That over spending has to have gone somewhere and if you listen to the Q1 QualTek’s conference call, for example, the CEO makes it pretty clear that significant work is underway May 18, about halfway through Q2:

And then more specifically, in wireless and 5G build-outs there is a long cycle, and I know a lot of folks were in great anticipation of when it was going to start and how it was going to start? I think, we’re pretty well past that. Now, we’re building 5G sites every day, a lot of our attention is focused around that. Our customers build plans and the work that we’re pulling in now is all related to this build that we’re now pretty clearly in.

It seems like the long awaited 5G rollout cycle has begun and is well underway.

Summary and Conclusion

Dycom, MasTec and QualTek are all three positioned to capture a huge secular growth cycle of rolling out fiber and 5G internet and are cheap relative to that potential. QualTek is priced for bankruptcy and thus has the most risk/reward if this cycle takes off sooner than later given its debt load and equity pricing. The safest pureplay bet is Dycom which should more than double in the next couple years based on my growth expectations. MasTec is a bit more diversified if you’re looking to spread out your risk.

QualTek appears to be the one to watch, because if the rollout is in full steam, and they can survive their debt load, then the upside could be mind bending back to where the SPAC originally IPO’d and then some. From what I can tell, it is seriously mispriced, but all three are undervalued presently and even if they were fairly valued ought to outperform the market in the next three to five years as they presumably get up to speed and revenues explode and margins expand.

Be the first to comment